GCC Dark Chocolate Market Size and Forecast 2025–2033

Health, Premiumization, and Changing Consumer Tastes Drive a New Era for Dark Chocolate in the GCC

Introduction

The Gulf Cooperation Council (GCC) dark chocolate market is undergoing a notable transformation as health awareness, premium consumption trends, and evolving retail ecosystems reshape consumer behavior across the region. Once viewed primarily as an indulgent confectionery product, dark chocolate is increasingly recognized as a functional and lifestyle-oriented food choice, aligning with modern preferences for lower sugar intake, antioxidant-rich diets, and ethically sourced products.

According to Renub Research, the GCC Dark Chocolate Market is expected to reach US$ 3.01 billion by 2033, up from US$ 1.52 billion in 2024, growing at a compound annual growth rate (CAGR) of 7.90% from 2025 to 2033. This growth is driven by rising disposable incomes, expanding retail channels, increased demand for premium and artisanal chocolates, and growing awareness of dark chocolate’s health benefits, including its reduced sugar content and high antioxidant properties.

As consumers across Saudi Arabia, the UAE, Qatar, Kuwait, Oman, and Bahrain increasingly favor quality over quantity, dark chocolate has emerged as a symbol of both indulgence and wellness, positioning it as one of the most dynamic segments within the GCC confectionery market.

GCC Dark Chocolate Market Overview

Dark chocolate is characterized by its high cocoa content and minimal addition of sugar and milk solids. Typically containing 70% to 90% cocoa solids or more, dark chocolate derives its deep color, intense flavor, and slightly bitter taste from cocoa liquor made from fermented, roasted, and ground cocoa beans. Cocoa solids and cocoa butter, the primary components of dark chocolate, contribute to its rich mouthfeel and nutritional value.

In addition to its distinctive taste profile, dark chocolate contains essential minerals such as iron, magnesium, copper, and zinc, as well as flavonoids and polyphenols known for their antioxidant properties. These compounds have been linked to a range of potential health benefits, including improved cardiovascular health, enhanced cognitive function, and reduced inflammation.

In the GCC, these nutritional advantages have resonated strongly with health-conscious consumers who are increasingly mindful of sugar intake and ingredient transparency. As a result, dark chocolate is no longer confined to the confectionery aisle alone; it is now gaining traction across functional foods, cosmetics, and even pharmaceutical applications.

Key Growth Drivers of the GCC Dark Chocolate Market

Rising Health Awareness

Health awareness is one of the most influential drivers of dark chocolate consumption across the GCC. Rising incidences of lifestyle-related conditions such as obesity, diabetes, and cardiovascular diseases have prompted consumers to seek healthier alternatives to traditional sugary snacks.

Dark chocolate’s lower sugar content and antioxidant-rich composition make it a preferred choice among fitness enthusiasts, working professionals, and aging populations. Marketing narratives emphasizing heart health, stress reduction, and cognitive benefits have further strengthened its appeal.

Increasing Disposable Incomes

Sustained economic development and diversification initiatives across GCC economies have significantly boosted disposable incomes. With greater purchasing power, consumers are increasingly willing to spend on premium and imported food products, including high-quality dark chocolates.

Affluent consumers often explore artisanal, single-origin, organic, and ethically sourced chocolates, reflecting a shift from mass-market offerings to more refined indulgences. This trend has enabled brands to introduce higher-priced products while expanding their customer base, thereby accelerating overall market growth.

Premiumization and Gifting Culture

Dark chocolate plays a prominent role in the GCC’s strong gifting culture, especially during religious and social occasions such as Ramadan, Eid, weddings, and corporate events. Premium packaging, luxury branding, and customized assortments have elevated dark chocolate into a preferred gifting option.

The demand for elegant presentation and high cocoa content chocolates has encouraged manufacturers to innovate in packaging design and flavor combinations, strengthening the premium segment of the market.

Product Innovation and Clean-Label Trends

Continuous product innovation is reshaping the GCC dark chocolate landscape. Manufacturers are introducing products tailored to evolving dietary needs, including vegan, sugar-free, lactose-free, organic, and allergen-free chocolates.

A notable example is Barry Callebaut’s launch of “NXT” in Saudi Arabia, the region’s first 100% plant-based, allergen-free dark and milk chocolate. Such innovations align with global sustainability and wellness trends, allowing brands to target niche but rapidly growing consumer segments.

Expansion of E-Commerce and Digital Retail

The rapid growth of e-commerce has transformed how consumers discover and purchase dark chocolate in the GCC. Online platforms provide access to a broader range of premium and international brands that may not be readily available in physical stores.

The COVID-19 pandemic further accelerated online shopping adoption, prompting chocolate brands to strengthen their digital presence through influencer marketing, targeted advertisements, and direct-to-consumer strategies. This digital shift has significantly enhanced product visibility, convenience, and consumer engagement.

Challenges Facing the GCC Dark Chocolate Market

Supply Chain Volatility

Dark chocolate production depends heavily on cocoa sourcing, which is vulnerable to climate change, geopolitical instability, and fluctuating global prices. Any disruption in cocoa supply can impact production costs, pricing strategies, and profit margins for manufacturers operating in the GCC.

Intense Market Competition

The GCC dark chocolate market is highly competitive, with both multinational giants and regional players vying for market share. Established brands benefit from strong distribution networks, marketing budgets, and brand loyalty, making it challenging for new entrants to gain traction.

Smaller and emerging brands are compelled to invest heavily in innovation, branding, and niche positioning, which increases operational costs and intensifies competitive pressure.

Country-Level Insights

Saudi Arabia Dark Chocolate Market

Saudi Arabia represents the largest and fastest-growing dark chocolate market in the GCC. Rising health consciousness, a young population, and strong gifting traditions drive demand for premium and artisanal dark chocolate products.

The expansion of modern retail outlets and e-commerce platforms has significantly improved product accessibility. Seasonal demand peaks during Ramadan and Eid further strengthen market performance.

United Arab Emirates Dark Chocolate Market

The UAE’s dark chocolate market is shaped by high disposable incomes, a diverse expatriate population, and a strong preference for luxury food products. Consumers increasingly seek ethically sourced, premium dark chocolates with unique flavor profiles.

Dubai and Abu Dhabi serve as regional hubs for gourmet food retail, enabling brands to test innovative products and premium concepts. Continued focus on quality and innovation is expected to sustain long-term growth.

Oman Dark Chocolate Market

Oman’s dark chocolate market is growing steadily as health awareness rises and consumer preferences evolve. While smaller in scale compared to Saudi Arabia and the UAE, demand for premium and artisanal chocolates is gradually increasing.

Festive gifting and expanding online retail channels are supporting market expansion, positioning Oman as a promising long-term growth market.

Market Segmentation Overview

By Type

70% Cocoa Dark Chocolate

75% Cocoa Dark Chocolate

80% Cocoa Dark Chocolate

90% Cocoa Dark Chocolate

By Application

Confectionery

Functional Food & Beverage

Pharmaceuticals

Cosmetics

By Distribution Channel

Convenience Stores

Supermarkets and Hypermarkets

Non-Grocery Retailers

Others

By Country

Saudi Arabia

United Arab Emirates

Kuwait

Qatar

Oman

Bahrain

Competitive Landscape

The GCC dark chocolate market is dominated by a mix of global confectionery leaders and strong regional brands. Companies are evaluated across four key dimensions: company overview, key persons, recent developments, and financial insights.

Key Companies Operating in the Market

Nestlé S.A.

The Hershey Company

Mondelez International, Inc.

Ferrero Group

Meiji Holdings Co., Ltd.

Bateel International LLC

Al-Seedawi Sweets Factories Co.

AANI & DANI

These players focus on premiumization, product differentiation, sustainability, and regional flavor adaptation to strengthen their market positions.

Final Thoughts

The GCC dark chocolate market is entering a dynamic growth phase, fueled by health-conscious consumption, premiumization, and digital retail expansion. With market value projected to grow from US$ 1.52 billion in 2024 to US$ 3.01 billion by 2033, dark chocolate is no longer a niche indulgence but a mainstream lifestyle product in the region.

As consumer preferences continue to evolve toward quality, transparency, and wellness, companies that prioritize innovation, ethical sourcing, and targeted marketing are well-positioned to capitalize on emerging opportunities. Despite challenges such as supply chain volatility and intense competition, the long-term outlook for the GCC dark chocolate market remains robust and promising.

About the Creator

Janine Root

Janine Root is a skilled content writer with a passion for creating engaging, informative, and SEO-optimized content. She excels in crafting compelling narratives that resonate with audiences and drive results.

Keep reading

More stories from Janine Root and writers in Feast and other communities.

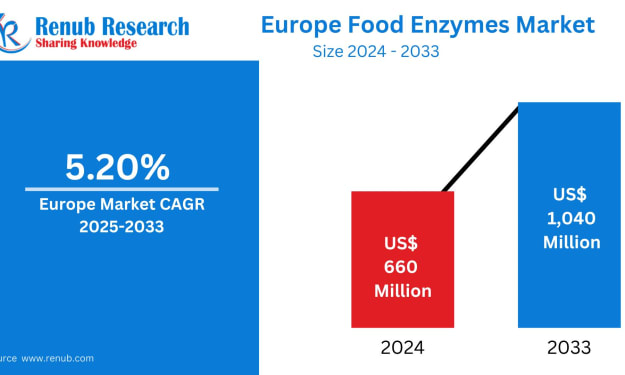

Europe Food Enzymes Market Size and Forecast 2025–2033

Introduction Europe’s food industry is undergoing a profound transformation as consumers increasingly prioritize health, transparency, and sustainability in their daily diets. At the heart of this evolution lies a rapidly expanding yet often overlooked segment: food enzymes. From improving texture and flavor to extending shelf life and enabling cleaner labels, food enzymes are quietly reshaping how food is produced, processed, and consumed across the continent.

By Janine Root 26 days ago in Feast

My Tous les Jours Trip

As someone who lives in a rural area, I don't get the chance to visit fancy restaurants or bakeries that often. So, when a friend told me about a French-Asian bakery that's less than an hour away, I knew I had to check it out and grab some pictures for social media. Tous les Jours ended up providing an immersive experience that went above and beyond my expectations--although I did leave with a few reservations.

By Kaitlin Shanks16 days ago in Feast

Comments

There are no comments for this story

Be the first to respond and start the conversation.