Japan Convenience Food Market Size and Forecast 2025–2033

How Konbini Culture, Technology, and Demographic Shifts Are Powering Japan’s Convenience Food Boom

Japan’s Convenience Food Market is entering a transformative phase, driven by lifestyle changes, cutting-edge food technologies, and one of the world’s most advanced retail networks. According to Renub Research, the Japan Convenience Food Market will reach US$ 38.7 billion by 2033, rising from US$ 24.99 billion in 2024 at a CAGR of 4.98% during 2025–2033. The powerful influence of urbanization, an aging population, and Japan’s legendary “konbini” ecosystem is reshaping how everyday consumers eat.

As cooking time shrinks and demand for nutritious, delicious, and ready-to-eat options rises, Japan’s convenience food landscape is evolving faster than ever. Ready meals, bento boxes, instant noodles, frozen foods, and portable snacks are now indispensable in the lives of workers, students, and seniors across the country.

Japan Convenience Food Market Overview

Convenience food refers to packaged, ready-to-eat, or ready-to-prepare products designed for minimal cooking effort. In Japan, this includes an extensive segment—instant noodles, frozen meals, ready-to-eat bentos, canned products, soups, and snack foods.

Japan’s convenience food culture is unlike anywhere else in the world. Products are synonymous with high-quality ingredients, freshness, hygiene, and innovative packaging solutions. The country’s demographic structure—characterized by a large working population, increasing single-person households, and a growing elderly population—creates immense market demand for portion-sized, nutritious, and convenient meal options.

Japan’s highly competitive convenience stores—7-Eleven, FamilyMart, and Lawson—act as innovation hubs. These stores offer freshly prepared sushi, rice bowls, sandwiches, salads, curries, Western meals, and desserts, all restocked multiple times a day. Moreover, Japan’s food manufacturing ecosystem prioritizes safety, flavor, and technology. Advanced processing, freezing, and vacuum packaging systems ensure that consumers receive products that taste remarkably fresh.

As a result, convenience food has become deeply ingrained in modern Japanese consumption habits, evolving from an occasional purchase to an everyday lifestyle necessity.

Growth Drivers in the Japan Convenience Food Market

1. Urban Lifestyles Leave Less Time for Cooking

Japan’s fast-paced urban life is redefining eating behaviors. Metropolitan centers like Tokyo, Osaka, and Yokohama have some of the longest working hours in the world. With limited time for meal preparation and rising single-person households, an increasing share of consumers rely on ready-to-eat or ready-to-heat foods.

Konbini stores play a crucial role by offering:

24/7 access

Affordable meal options

High-quality seasonal selections

Easy-to-carry packaging

Convenience food has morphed into a primary meal replacement, not simply an alternative to cooking. For urban consumers, grabbing a bento, onigiri, or noodle bowl is often quicker, cheaper, and more satisfying than preparing food at home.

2. Japan’s Rapidly Aging Population Is Shaping Demand

Japan has one of the world’s oldest populations. As of September 2024, government data shows 36.25 million people aged 65 or above, accounting for nearly one-third of the population.

Elderly consumers increasingly prefer:

Small portion meals

Easy-to-digest foods

Nutrient-rich ready meals

Frozen foods with long shelf life

Food companies are innovating to cater to senior needs with products lower in sodium, higher in fiber, and easier to chew or reheat. This demographic shift is expected to remain a consistent market accelerator through 2033, as manufacturers target older consumers with specialized convenience food offerings.

3. Advancements in Processing & Packaging Technology

Japan is a global leader in food technology, and innovation is a major growth catalyst.

Recent developments include:

Vacuum and MAP (Modified Atmosphere Packaging)

Microwave-safe packaging

Intelligent labeling systems

Automation and AI-enhanced production lines

High-precision freezing technology

In November 2024, Neste, Mitsui Chemicals, and Prime Polymer collaborated to supply sustainable, bio-based food packaging to Japan Co-op, replacing fossil-based materials. Such initiatives align with Japan’s environmental goals while improving safety, shelf life, and freshness.

These technical advancements significantly enhance consumer trust—critical in a market that values freshness above all else.

Challenges in the Japan Convenience Food Market

1. Health Concerns About Processed Foods

Younger Japanese consumers are increasingly health-conscious, avoiding:

High sodium

Preservatives

Artificial additives

If convenience food manufacturers fail to adapt to clean-labeled, nutritious options, they risk losing consumers to fresh alternatives, diet-specific brands, or premium health foods.

2. Labor Shortages Impacting Production and Retail

Japan’s shrinking workforce presents long-term challenges.

Labor shortages affect:

Food processing plants

Logistics and supply chain operations

Konbini store staffing

While automation helps, it cannot fully resolve issues in maintaining Japan’s high-frequency product restocking and freshness standards. The labor gap remains a bottleneck to market scalability.

Segmentation Insights

Japan Ready-to-Eat (RTE) Convenience Food Segment

The RTE segment is the backbone of Japan’s convenience food industry.

Popular products include:

Donburi rice bowls

Sushi bento packs

Sandwiches

Curry rice

Noodle cups

These offerings dominate because they combine freshness, flavor, affordability, and convenience—critical for busy workers and students. Seasonal variations (like limited-edition flavors) also help maintain high demand year-round.

Japan Frozen Food Segment

Frozen foods are witnessing significant growth, especially among:

Dual-income households

Seniors

Suburban families

Products such as frozen dumplings, pasta, vegetables, and fried rice require minimal effort to prepare. Advanced freezing technology preserves taste and texture effectively, making frozen meals increasingly competitive with fresh items.

The pandemic accelerated this trend, and post-pandemic behavior shows the shift is permanent.

Convenience Stores (“Konbini”) Segment

Konbini stores are the heart of Japan’s convenience food ecosystem.

Key strengths:

24/7 operations

Freshly cooked meals

Rapid restocking cycles

Seasonal product rotation

High accessibility

With additional services—ATMs, courier services, Wi-Fi, and bill payment—konbini stores double as micro-community centers. Their influence makes them Japan’s most powerful distribution channel for convenience foods.

Online Retail Segment

Digital retail platforms like Rakuten, Amazon Japan, and store apps are reshaping food purchasing patterns. While not as dominant as konbini stores, online channels are growing rapidly due to:

Home delivery

Meal kit subscriptions

Convenience for elderly and homebound consumers

Customization and bundle offerings

Online retail is expected to gain a larger market share through 2033.

Regional Market Insights

Tokyo: The Epicenter of Convenience Food

Tokyo’s dense population, long working hours, and limited kitchen space make it the top-performing region.

Tokyo has the highest concentration of convenience stores per capita, offering unparalleled food diversity—from traditional Japanese meals to Western, Korean, and fusion options.

Aichi Prefecture

Driven by industrial activity and a large student population, Aichi has high demand for bento meals and convenient snacks. Suburban areas, in particular, rely heavily on frozen and ready-made dinners.

Shizuoka Prefecture

Shizuoka’s tourism, commuter population, and aging demographics boost convenience food demand. Investments in cold chain logistics are making frozen foods more accessible across the region.

Saitama Prefecture

A major suburban commuter hub for Tokyo, Saitama sees strong demand for:

Quick breakfasts

Packed lunches

Frozen dinners

As urbanization increases, convenience store chains continue to expand aggressively across the prefecture.

Market Segmentation

By Product

Ready-to-eat

Frozen food

By Distribution Channel

Supermarkets & Hypermarkets

Convenience Stores

Online Retail

Others

Top 10 City Markets

Tokyo

Kansai

Aichi

Kanagawa

Saitama

Hyogo

Chiba

Hokkaido

Fukuoka

Shizuoka

Key Company Profiles (5 Viewpoints Each: Overview, Key Person, Recent Developments, SWOT, Revenue)

General Mills Inc.

Conagra Brands

Nestlé S.A.

Hormel Foods

Unilever PLC

The Kraft Heinz Company

Nomad Foods Ltd

B&G Foods, Inc.

Final Thoughts

Japan’s convenience food market is undergoing a dynamic evolution shaped by demographic transitions, lifestyle changes, and advances in food technology. As the country moves toward a future dominated by single-person households, aging consumers, and fast-paced urban life, the demand for nutritious, flavorful, and time-saving meal solutions will continue to rise.

The fusion of konbini innovation, high-quality food manufacturing, and sustainable packaging initiatives positions Japan as a global benchmark for the convenience food sector. With a projected value of US$ 38.7 billion by 2033, the market is set for robust growth, offering immense opportunities for domestic and global players alike.

About the Creator

jaiklin Fanandish

Jaiklin Fanandish, a passionate storyteller with 10 years of experience, crafts engaging narratives that blend creativity, emotion, and imagination to inspire and connect with readers worldwide.

Keep reading

More stories from jaiklin Fanandish and writers in Feast and other communities.

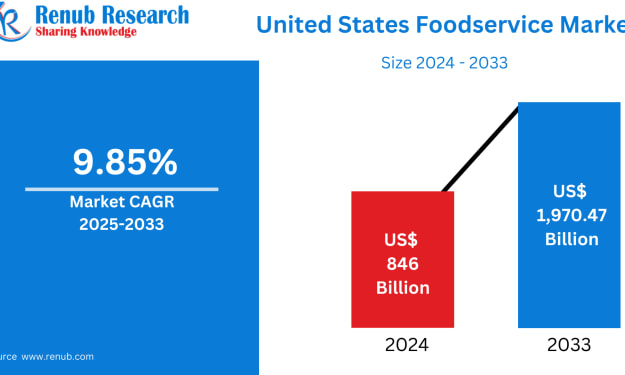

United States Foodservice Market Size & Forecast 2025–2033

The United States Foodservice Market is entering a transformative era, shaped by powerful shifts in consumer behavior, technology adoption, and evolving retail landscapes. According to Renub Research, the U.S. foodservice market is expected to grow from US$ 846 billion in 2024 to US$ 1,970.47 billion by 2033, reflecting an impressive CAGR of 9.85% between 2025 and 2033.

By jaiklin Fanandishabout a month ago in Feast

My Tous les Jours Trip

As someone who lives in a rural area, I don't get the chance to visit fancy restaurants or bakeries that often. So, when a friend told me about a French-Asian bakery that's less than an hour away, I knew I had to check it out and grab some pictures for social media. Tous les Jours ended up providing an immersive experience that went above and beyond my expectations--although I did leave with a few reservations.

By Kaitlin Shanks17 days ago in Feast

Organic Baby Food Market Companies Analysis (2025–2033)

Introduction: A New Standard for Infant Nutrition The global Organic Baby Food Market is undergoing a transformative shift as modern parents increasingly demand clean, transparent, and sustainable nutrition for their children. Organic baby food—made without synthetic fertilizers, artificial preservatives, genetically modified organisms (GMOs), or chemical pesticides—has moved from a niche category to a mainstream necessity. Rising awareness of food safety, health outcomes, and environmental sustainability is reshaping consumer behavior worldwide.

By Aaina Oberoiabout 10 hours ago in Feast

Comments

There are no comments for this story

Be the first to respond and start the conversation.