Europe Prostate Cancer Diagnostics Market Size & Forecast 2025–2033

Advancing Early Detection Through Innovation, Awareness, and Precision Diagnostics

Europe Prostate Cancer Diagnostics Market Outlook

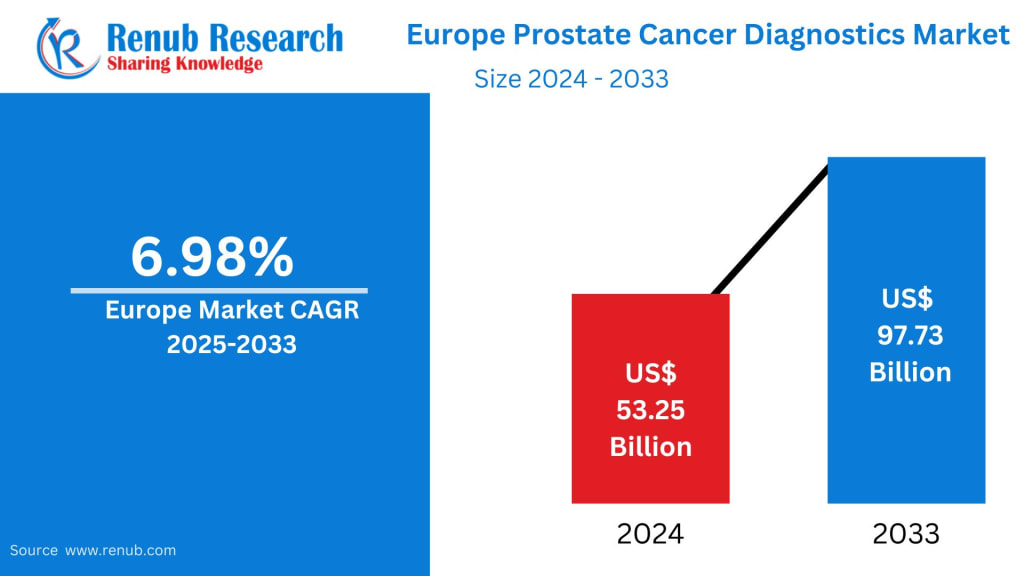

The Europe Prostate Cancer Diagnostics Market is on a strong upward trajectory, driven by demographic shifts, rising cancer awareness, and continuous innovation in diagnostic technologies. According to Renub Research, the market is expected to grow from US$ 53.25 billion in 2024 to US$ 97.73 billion by 2033, registering a CAGR of 6.98% during 2025–2033.

This growth reflects Europe’s increasing focus on early cancer detection, preventive healthcare, and precision medicine. Prostate cancer remains one of the most commonly diagnosed cancers among men across the region, particularly in populations aged 50 years and above. Governments, healthcare providers, and diagnostic companies are therefore intensifying investments in screening programs, advanced imaging, and molecular diagnostics to improve survival outcomes and reduce long-term treatment costs.

Europe Prostate Cancer Diagnostics Market Overview

Prostate cancer diagnostics refers to the clinical tests and medical procedures used to identify prostate cancer at various stages. These include PSA (Prostate-Specific Antigen) blood tests, Digital Rectal Examination (DRE), multiparametric MRI, ultrasound-guided biopsy, and advanced genomic and molecular testing.

In Europe, early detection plays a crucial role in improving prognosis and expanding treatment options. Countries such as Germany, the United Kingdom, France, and Italy have well-established diagnostic infrastructures, supported by public reimbursement systems and strong hospital networks. The increasing adoption of MRI-targeted biopsy and genomic profiling has significantly improved diagnostic accuracy, helping clinicians distinguish aggressive cancers from indolent ones and avoid unnecessary procedures.

Key Drivers of the Europe Prostate Cancer Diagnostics Market

Rising Prevalence in an Aging Population

Europe has one of the world’s oldest populations, and prostate cancer incidence rises sharply with age. As life expectancy continues to increase, the number of men at risk is expanding rapidly. This demographic trend is placing sustained demand on routine PSA screening, follow-up imaging, and confirmatory diagnostics.

Public health campaigns and routine check-up programs across Europe are further encouraging men to seek early testing. According to EU-level data, a significant share of men are projected to receive a cancer diagnosis before the age of 75, reinforcing the need for accessible and reliable diagnostic services.

Technological Advancements in Diagnostic Methods

Technological innovation is transforming prostate cancer diagnostics across Europe. The integration of multiparametric MRI, next-generation sequencing (NGS), liquid biopsy, and AI-assisted imaging has enhanced diagnostic precision while minimizing invasiveness.

MRI-targeted biopsy, in particular, has become a game-changer by improving the detection of clinically significant prostate cancers and reducing overdiagnosis. Genomic tests are also gaining traction, enabling risk stratification and personalized treatment planning. These innovations are increasingly being incorporated into standard clinical protocols, especially in Western Europe.

Strong Government Support and Screening Initiatives

European governments and healthcare organizations continue to prioritize cancer prevention and early detection. Investments in national screening frameworks, physician training, and reimbursement policies have created a favorable environment for market growth.

Collaborative initiatives at the EU level are also supporting harmonized screening strategies and evidence-based diagnostics. These efforts aim to improve efficiency, reduce disparities, and enhance patient outcomes across member states, further accelerating the adoption of advanced prostate cancer diagnostics.

Challenges Facing the Europe Prostate Cancer Diagnostics Market

Variation in Screening Policies and Public Acceptance

Despite medical advancements, prostate cancer screening recommendations vary widely across Europe. Some healthcare systems actively promote routine PSA testing, while others remain cautious due to concerns over overdiagnosis and overtreatment.

Cultural attitudes toward preventive healthcare and differences in healthcare policy influence screening participation rates. These inconsistencies can limit early detection in certain regions and slow overall market expansion.

High Cost of Advanced Diagnostic Technologies

Sophisticated diagnostic tools such as MRI-guided biopsy systems, genomic assays, and molecular tests involve significant costs. Limited reimbursement and budget constraints can restrict adoption, particularly in public hospitals and less-developed regions.

Healthcare providers often require robust cost-effectiveness data before fully integrating these technologies, making affordability a continuing challenge despite their clinical benefits.

Europe Prostate Cancer Diagnostics Market Segmentation Insights

By Test Type

Initial screening methods such as PSA testing and DRE form the foundation of early diagnosis and remain widely used due to affordability and accessibility. Confirmatory tests, including MRI, biopsy, and genomic profiling, are experiencing faster growth as clinicians seek higher diagnostic accuracy and personalized insights.

By End User

Hospitals dominate the market due to their comprehensive diagnostic capabilities, multidisciplinary teams, and access to advanced imaging and pathology services.

Diagnostic centers are emerging as important contributors, offering faster turnaround times and specialized prostate cancer testing.

Research institutes also play a key role in clinical trials and diagnostic innovation.

Country-Level Market Analysis

Germany Prostate Cancer Diagnostics Market

Germany represents one of the largest and most advanced markets in Europe. With strong insurance coverage, routine health check-ups, and rapid adoption of multiparametric MRI and precision diagnostics, Germany leads in both innovation and market size. The country’s focus on clinical research further supports widespread use of molecular and genomic testing.

United Kingdom Prostate Cancer Diagnostics Market

The UK market is expanding steadily, supported by NHS-led initiatives, high awareness, and strong academic research. While PSA testing is not part of a universal screening program, it is readily accessible through general practitioners, particularly for high-risk groups. The UK is also at the forefront of AI-driven imaging and genomic research.

Russia Prostate Cancer Diagnostics Market

Russia’s market is developing gradually, with improved diagnostic facilities in major urban centers such as Moscow and St. Petersburg. Government-led cancer programs are increasing awareness and PSA testing rates, although access disparities remain in rural areas. Continued healthcare reforms are expected to improve diagnostic reach over time.

Market Segmentation

By Type

Benign Prostatic Hyperplasia (BPH)

Prostatic Adenocarcinoma

Small Cell Carcinoma

Others

By Test Type

Preliminary Tests

Confirmatory Tests

By End User

Hospitals

Diagnostic Centers

Research Institutes

Others

By Country

France

Germany

Italy

Spain

United Kingdom

Belgium

Netherlands

Russia

Poland

Greece

Norway

Romania

Portugal

Rest of Europe

Key Players Analysis

The European prostate cancer diagnostics market is moderately consolidated, with global and regional players competing through innovation, partnerships, and product expansion. Key companies covered with five viewpoints (overview, key person, recent developments, SWOT, and revenue analysis) include:

F. Hoffmann-La Roche AG

Bayer AG

Thermo Fisher Scientific Inc.

Abbott Laboratories Inc.

Siemens Healthineers AG

Becton Dickinson and Company

Agilent Technologies Inc.

Hologic Inc.

QIAGEN N.V.

OPKO Health Inc.

These players are investing heavily in molecular diagnostics, imaging platforms, and AI-driven solutions to strengthen their competitive position across Europe.

Final Thoughts

The Europe Prostate Cancer Diagnostics Market is entering a phase of sustained expansion, underpinned by demographic aging, rising disease awareness, and rapid technological advancement. While challenges such as cost barriers and screening inconsistencies persist, strong government backing and innovation-driven competition continue to shape a positive outlook.

As precision medicine and early detection gain prominence, prostate cancer diagnostics will remain a critical pillar of Europe’s oncology landscape. Market participants that combine clinical accuracy, affordability, and technological innovation are well positioned to capture growth opportunities through 2033 and beyond.

About the Creator

Diya Dey

Market Analyst

Day 4 of Quitting

If this is how sobriety feels, maybe it’s better to go through life a little buzzed… this, along with other hits like, I want to kill myself, I wish I was dead, and I’m going to throw myself off a bridge have been the only thoughts on rotation these past few days. I promise myself that if, in a month, I still feel like this (‘this’ meaning despondent, full of rage, and simultaneously numb) I can go back to smoking. Until mid-February though? Nicotine is off the table.

By sleepy drafts4 days ago in Longevity

Chilly Robins in the Garden? Put This Out Today and They’ll Start Coming Back Every Single Morning

As winter tightens its grip and frost coats the edges of your garden, you might notice that the familiar chirps of robins have become far less frequent. These charming, bright-breasted birds, often symbols of the festive season, are not disappearing; they are simply seeking food and warmth elsewhere. Yet, with a few thoughtful steps, you can turn your garden into a welcoming haven that keeps these delightful visitors returning day after day.

By Fiazahmedbrohi 3 days ago in Longevity

Comments

There are no comments for this story

Be the first to respond and start the conversation.