Australia Colonoscopy Devices Market Size and Forecast 2025–2033

How Colorectal Cancer Screening, Aging Demographics, and High-Tech Endoscopy are Transforming Australia’s Diagnostic Landscape

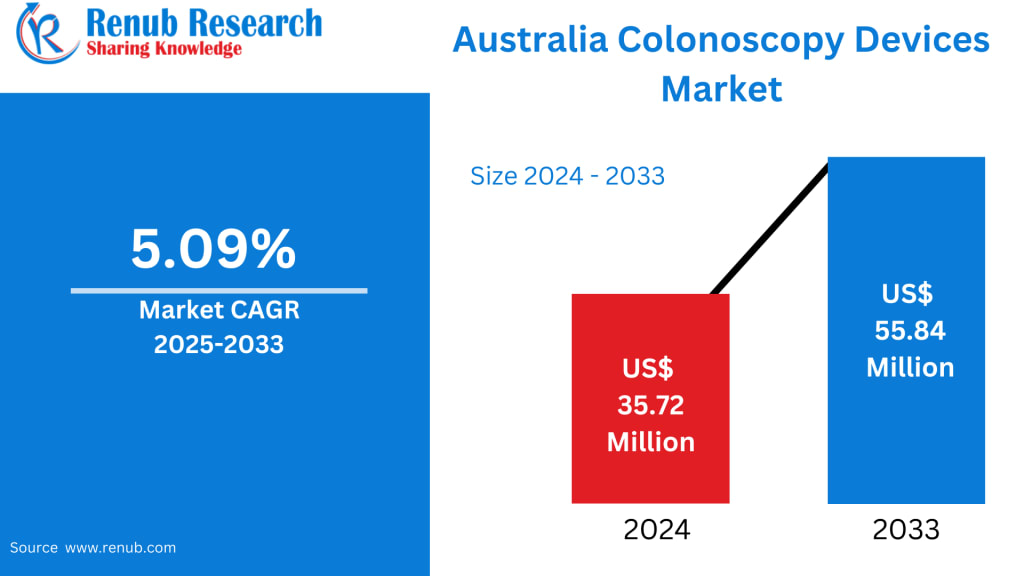

Australia’s colonoscopy devices market is undergoing a period of steady transformation, driven by rising awareness about gastrointestinal health, rapid technological advancements, and an aging population susceptible to colorectal disorders. According to Renub Research, the Australia Colonoscopy Devices Market is anticipated to grow to US$ 55.84 million by 2033 from US$ 35.72 million in 2024, registering a CAGR of 5.09% between 2025 and 2033.

This growth reflects a nationwide shift toward early detection, precision diagnostics, and enhanced patient care—supported strongly by government-led screening programs and continuous innovation in the MedTech domain. As colorectal cancer remains one of the most prevalent cancers in the country, colonoscopy devices have become indispensable tools for detecting and preventing life-threatening conditions.

Australia Colonoscopy Devices Market Overview

Colonoscopy devices are highly sophisticated instruments designed to examine the inner lining of the colon and rectum, allowing clinicians to detect polyps, ulcers, hemorrhages, inflammation, and early-stage colorectal cancers. A typical colonoscope includes a flexible tube with a high-resolution camera, illumination system, irrigation channels, and often integrated biopsy or therapeutic tools.

Australia’s adoption of colonoscopy devices is among the highest globally due to the country’s elevated incidence of colorectal cancer and its strong preventive healthcare culture. The government-backed National Bowel Cancer Screening Program (NBCSP) has significantly increased screening rates, encouraging early diagnosis and intervention. This has directly translated into increased demand for colonoscopy equipment in hospitals, specialist clinics, day centers, and ambulatory surgical facilities.

Furthermore, the surge in elderly populations—accompanied by greater health literacy and accessibility to advanced medical care—has further cemented colonoscopy devices as a cornerstone of Australia’s gastroenterology and oncology infrastructure.

Key Market Drivers

1. Rising Cases of Colorectal Cancer

Colorectal cancer remains a major public health concern in Australia. The country consistently ranks among the highest in global colorectal cancer incidence, making screening essential rather than optional.

Key Statistics

Colorectal cancer was the fourth most frequently diagnosed cancer in Australia in 2020.

In 2020, 14,534 new cases were diagnosed (7,833 men and 6,701 women).

By 2024, estimated new cases increased to 15,542 (8,205 men and 7,337 women).

The risk of developing colorectal cancer by age 85 is 1 in 21 (4.8%):

1 in 19 (5.1%) for men

1 in 23 (4.4%) for women

The NBCSP invites residents aged 50–74 to complete screening tests every two years, significantly increasing colonoscopy referrals for positive results. Diagnostic facilities in both public and private sectors have responded by upgrading their equipment to high-definition and AI-driven models, enhancing accuracy and procedural efficiency.

As screening becomes more widespread, the need for advanced colonoscopy systems—featuring improved maneuverability, superior imaging clarity, and therapeutic capabilities—continues to grow.

2. Aging Population and Growing Awareness of Gastrointestinal Health

Australia’s demographic shift toward a significantly older population is one of the most influential factors contributing to market expansion.

Demographic Snapshot

By 2026, more than 22% of Australians will be over age 65, compared to:

16% in 2020

8.3% in 1970

Age is a known risk factor for polyps, diverticulitis, inflammatory bowel disease (IBD), and colorectal cancer. As a result, routine colonoscopy screenings among older adults have become standard practice.

Additionally, Australians today exhibit greater health consciousness. Increased doctor visits, better health insurance coverage, and public awareness campaigns have made gastrointestinal screening more mainstream. Healthcare facilities across metropolitan cities and regional hubs have rapidly upgraded colonoscopy suites to meet this growing demand.

3. Continuous Technological Advancements in Endoscopy

The colonoscopy devices market is riding a technological wave that is reshaping the future of diagnostics. Newer innovations include:

High-definition and 4K imaging systems

AI-assisted polyp detection

Single-use colonoscopes for improved hygiene

Robotic-assisted colonoscopy navigation

Enhanced sterilisation solutions

A leading example is Olympus Australia, one of the major endoscopy giants. In September 2024, the company launched “Sapphire,” its first flexible endoscope sterilisation plant in Melbourne. Sapphire is part of the “Olympus On-Demand” solution aimed at reducing risks, optimizing costs, and streamlining the delivery of endoscopy services nationwide.

Private hospitals and diagnostic labs are embracing these innovations not only to heighten diagnostic precision but also to attract patients seeking more comfortable and faster procedures.

Market Challenges

1. High Equipment and Maintenance Costs

Despite significant demand, high capital costs continue to create barriers—especially for smaller clinics and rural hospitals. Colonoscopes and visualization systems require:

Expensive acquisition

Regular maintenance and repair

Sterilization cycles

Disposable accessories

Training for specialized staff

Budget constraints within the public healthcare system can delay upgrades or limit access to state-of-the-art equipment.

2. Limited Access in Rural and Remote Areas

Australia’s vast geography makes healthcare accessibility uneven. Rural and remote communities often face:

Shortages of trained gastroenterologists

Delays in scheduling colonoscopy procedures

Limited endoscopic infrastructure

While telehealth, mobile endoscopy vans, and outreach programs have improved accessibility, disparities remain. Urban centers have cutting-edge units with AI technology, while remote towns lack even basic screening access—indicating a major market gap that can be addressed through innovation and partnerships.

Market Breakdown by Segments

Product Segmentation

Colonoscope (dominant segment)

Visualization System

Others

Application Segmentation

Colorectal Cancer (largest segment)

Ulcerative Colitis

Crohn’s Disease

Others

End User Segmentation

Hospitals

Clinics & Ambulatory Surgical Centers

Others

Regional Market Insights

Victoria

The state stands out as a high-demand region due to its strong medical infrastructure, prominent research hospitals, and advanced diagnostic centers. Melbourne houses several high-tech endoscopy suites, making Victoria a leader in adopting AI-integrated and HD imaging systems.

Western Australia

Perth’s growing healthcare investments and public awareness initiatives are fueling the market. Yet, the large rural expanse creates logistical challenges. Mobile endoscopy units and rural outreach programs are gaining traction to bridge this gap.

South Australia

Anchored by Adelaide’s major hospitals and cancer screening centers, South Australia benefits from strong public health campaigns promoting early detection. Regional inequality persists, but targeted government efforts are improving access.

Other Key States

New South Wales – The most populous state; significant hospital investments

Queensland – Growing demand driven by rising colorectal awareness

Australian Capital Territory – Strong public-sector healthcare adoption

Tasmania & Northern Territory – Smaller markets but growing screening initiatives

Associated Market Trends

Australia Colonoscope Market

Demand is rising for HD and 4K colonoscopes with enhanced flexibility, durability, and AI compatibility. Disposable scopes are gaining popularity due to infection control standards.

Australia Colorectal Cancer Devices Market

Biopsy forceps, snares, imaging systems, and minimally invasive surgical tools are in high demand. Public and private awareness campaigns continue to drive early diagnosis efforts.

Australia Crohn’s Disease Market

Crohn’s patients require regular colonoscopic monitoring, increasing long-term demand for high-performance endoscopic devices that minimize discomfort and provide accurate disease tracking.

Competitive Landscape

The market features strong participation from global and local medical device leaders. Each company is evaluated across five viewpoints—Overview, Key Person, Recent Developments, SWOT Analysis, and Revenue Analysis.

Key Players

Boston Scientific Corporation

Fujifilm Holdings Corporation

Hoya Corporation

Medtronic plc

Olympus Corporation

Stryker Corporation

Steris Corp.

Merit Medical Systems Inc.

Getinge AB

These companies are investing heavily in R&D to develop next-generation diagnostic tools that reduce procedure time, enhance accuracy, and improve patient outcomes.

Final Thoughts

Australia’s Colonoscopy Devices Market is entering a dynamic growth phase shaped by preventive healthcare initiatives, a rising senior population, and groundbreaking technological innovation. As the market grows from US$ 35.72 million in 2024 to US$ 55.84 million by 2033, the focus is shifting toward improving accessibility, minimizing diagnostic disparities, and equipping healthcare facilities with the latest endoscopic solutions.

A nationwide commitment to early screening—combined with continuous advancements in AI, imaging, and robotic-assisted navigation—positions Australia to become a leader in gastrointestinal diagnostics. While challenges remain, particularly in rural accessibility and equipment costs, the market’s long-term trajectory remains strongly positive.

About the Creator

Keep reading

More stories from Aaina Oberoi and writers in Longevity and other communities.

United States Medical Gas Market Size and Forecast 2025–2033

The United States Medical Gas Market is projected to reach US$ 8.01 billion by 2033, rising from US$ 4.34 billion in 2024, according to Renub Research. This strong growth—at a CAGR of 7.05% from 2025 to 2033—highlights the increasing reliance on medical gases across hospitals, home healthcare, pharmaceuticals, diagnostics, and biotechnology innovation. From oxygen supplies that sustain critical care patients to ultra-high purity gases used in drug development, the importance of medical gases in modern healthcare is expanding rapidly.

By Aaina Oberoiabout a month ago in Longevity

Day 4 of Quitting

If this is how sobriety feels, maybe it’s better to go through life a little buzzed… this, along with other hits like, I want to kill myself, I wish I was dead, and I’m going to throw myself off a bridge have been the only thoughts on rotation these past few days. I promise myself that if, in a month, I still feel like this (‘this’ meaning despondent, full of rage, and simultaneously numb) I can go back to smoking. Until mid-February though? Nicotine is off the table.

By sleepy drafts7 days ago in Longevity

Chilly Robins in the Garden? Put This Out Today and They’ll Start Coming Back Every Single Morning

As winter tightens its grip and frost coats the edges of your garden, you might notice that the familiar chirps of robins have become far less frequent. These charming, bright-breasted birds, often symbols of the festive season, are not disappearing; they are simply seeking food and warmth elsewhere. Yet, with a few thoughtful steps, you can turn your garden into a welcoming haven that keeps these delightful visitors returning day after day.

By Fiazahmedbrohi 6 days ago in Longevity

Comments

There are no comments for this story

Be the first to respond and start the conversation.