United States GLP-1 Analogues Market Projected to Soar Amid Robust Innovation and Expanding Therapeutic Applications

Rising Demand for Obesity and Diabetes Treatments, Emerging Oral Formulations, and Expanding Indications Drive Market Momentum

The global GLP-1 (glucagon-like peptide-1) analogues market is on an extraordinary growth trajectory, reflecting one of the fastest-expanding sectors within the biopharmaceutical industry. Valued at US$37.4 billion in 2023, the market grew to US$47.4 billion in 2024 and is projected to advance at a compound annual growth rate (CAGR) of 33.2% from 2024 to 2032, ultimately reaching US$471.1 billion by the end of the forecast period.

The surge in demand for GLP-1 analogues is primarily driven by the global rise in obesity and type 2 diabetes, two of the most significant public health challenges of the modern era. The adoption of these drugs has expanded beyond their original diabetic applications, now encompassing obesity, metabolic disorders, and even investigational uses in neurological diseases such as Alzheimer’s.

Expanding Clinical Pipeline and Innovation Drive Growth

GLP-1 analogues are a class of incretin mimetics designed to help regulate blood glucose levels, enhance insulin secretion, and promote satiety—making them critical in managing both diabetes and obesity. The pipeline for this drug class is stronger than ever, with leading pharmaceutical companies accelerating innovation through advanced formulations and new combination products.

Several high-profile developments underscore this momentum:

Oral semaglutide (25 mg and 50 mg) is expected to revolutionize the administration route for type 2 diabetes patients.

CagriSema, a combination of Cagrilintide and Semaglutide, is in late-stage trials targeting both obesity and diabetes.

Survodutide is emerging as a promising candidate for Nonalcoholic Steatohepatitis (NASH) and obesity.

Semaglutide continues to demonstrate strong efficacy in trials addressing NASH and related metabolic syndromes.

These product advancements are expected to fuel growth as new therapies enter the market over the next several years, broadening access and strengthening therapeutic diversity.

Dominance of Key Players and Emerging Entry Barriers

Despite rapid innovation, the competitive landscape of the GLP-1 analogues market remains highly concentrated. Novo Nordisk A/S and Eli Lilly and Company currently account for over 90% of marketed products, effectively establishing a duopoly in the space.

This market dominance results from several factors:

Strong brand recognition and clinical credibility of their flagship products, including Ozempic, Mounjaro, and Wegovy.

Established global supply and distribution networks capable of meeting surging demand.

Extensive patent protection and intellectual property portfolios that limit generic competition.

While this concentrated market structure has ensured consistent quality and supply reliability, it poses challenges for smaller or emerging biopharmaceutical entrants. High R&D costs, strict regulatory standards, and manufacturing complexities further compound entry barriers. However, ongoing collaborations and licensing agreements between biotech innovators and major pharmaceutical corporations are expected to foster gradual diversification over time.

Opportunities in New Therapeutic Indications

A pivotal growth catalyst for the GLP-1 analogues market is the expansion of therapeutic applications beyond diabetes and obesity. Research has shown that GLP-1 analogues possess anti-inflammatory and neuroprotective properties, opening new frontiers for treating conditions such as Alzheimer’s disease, NASH, Obstructive Sleep Apnea (OSA), and cardiovascular diseases.

These expanded applications are particularly relevant as global healthcare systems shift toward managing chronic metabolic and neurodegenerative diseases holistically. The weight-reducing and metabolic-regulating benefits of GLP-1 analogues make them suitable candidates for multi-targeted therapeutic strategies.

Furthermore, the growing global awareness of obesity as a chronic medical condition—not merely a lifestyle issue—is enhancing reimbursement support and patient access. As such, pharmaceutical companies are investing in large-scale trials to validate these new indications and gain regulatory approval in additional therapeutic areas.

Regional Insights: North America Leads the Charge

North America continues to represent the largest and most dynamic market for GLP-1 analogues, driven by robust healthcare infrastructure, high obesity prevalence, and increasing physician and patient awareness of advanced anti-obesity therapeutics. The region’s strong R&D ecosystem and significant capital investment in biopharmaceutical innovation further enhance its leadership position.

Research investments and new clinical collaborations in North America have accelerated drug development timelines. Major academic institutions and pharmaceutical companies are conducting extensive trials on novel GLP-1 formulations, including once-weekly oral and combination therapies. Moreover, rising patient preference for less invasive oral alternatives is expected to shape the market’s next growth phase.

Challenges: Addressing Non-Adherence and Accessibility

Despite the tremendous growth outlook, patient adherence remains a persistent challenge for long-term market sustainability. Clinical data indicate a significant decline in adherence rates after 12 months of treatment, particularly for injectable formulations.

For example, studies on Wegovy and Saxenda show that only 32% and 21% of patients, respectively, continue therapy after a year. Factors such as nausea, vomiting, injectable inconvenience, and affordability barriers contribute to early discontinuation.

Manufacturers are actively addressing these issues through patient support programs, improved delivery mechanisms (such as autoinjectors and pens), and the development of next-generation oral GLP-1 analogues with fewer side effects. These innovations are anticipated to enhance adherence and expand patient populations, especially in developing economies.

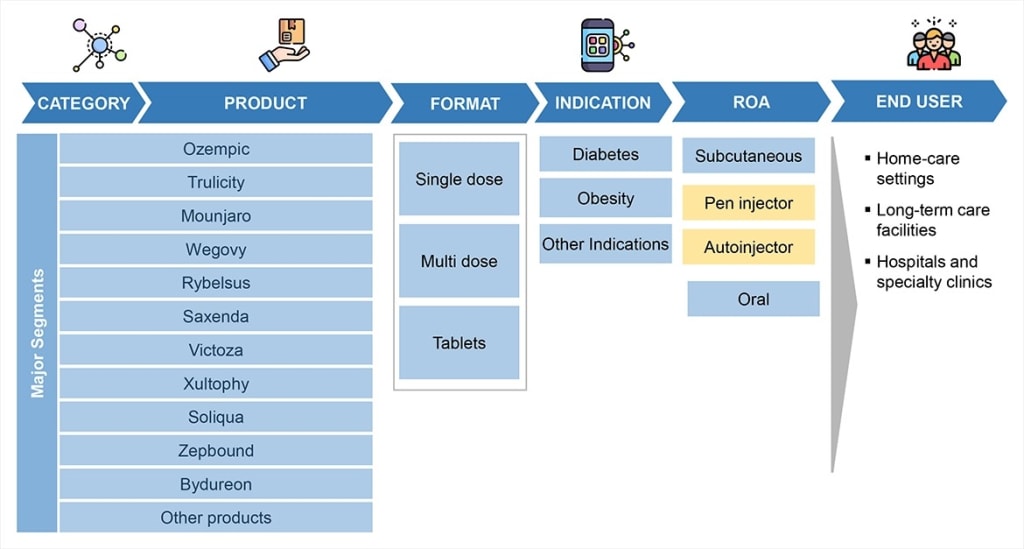

Market Segmentation Highlights

By Product:

Ozempic dominated the market in 2023, primarily due to its strong brand equity, proven clinical efficacy, and wide global availability. Other leading brands include Trulicity, Mounjaro, Rybelsus, Saxenda, and Victoza.

By Format:

The single-dose segment led the market in 2023, favored for its ease of administration and the availability of once-weekly formulations that improve patient compliance. Autoinjector-based delivery systems continue to be the preferred choice for both physicians and patients due to convenience and reduced error rates.

Future Outlook: Transforming the Landscape of Metabolic Health

As the global healthcare community intensifies its focus on chronic disease prevention and management, GLP-1 analogues are set to play an increasingly central role. The convergence of metabolic research, biotechnology innovation, and patient-centered care is reshaping the therapeutic landscape for obesity, diabetes, and related disorders.

With a forecasted valuation exceeding US$471 billion by 2032, the GLP-1 analogue market is poised to become a cornerstone of modern metabolic medicine. Continued investments in R&D, expansion into new indications, and patient-centric delivery innovations will determine the competitive advantages of leading industry participants.

The United States GLP-1 analogues market, in particular, will remain a bellwether for global trends—reflecting not only scientific advancement but also the shifting public perception of obesity and metabolic disease management. As pharmaceutical companies continue to explore the full therapeutic potential of GLP-1 analogues, the industry stands at the threshold of a transformative era in global healthcare innovation.

About the Creator

Keep reading

More stories from Juan Martinez and writers in Journal and other communities.

United States AI in Healthcare Market Poised for Transformative Growth, Driven by Early Detection Needs and Technological Advancements

The United States Artificial Intelligence (AI) in Healthcare Market is undergoing a profound transformation, reflecting both the maturity of advanced AI tools and the evolving priorities of healthcare delivery systems. Globally, the AI in healthcare market, valued at US$14.92 billion in 2024, surged to US$21.66 billion in 2025, and is projected to achieve a remarkable CAGR of 38.6% from 2025 to 2030, ultimately reaching US$110.61 billion by the end of the forecast period.

By Juan Martinez3 months ago in Journal

How AI Is Reshaping the Future of Software Development

Artificial intelligence is no longer an experiment running in parallel to engineering. It has moved directly into the production pipeline. For modern software development companies, AI is changing how code is written, tested, secured, and evolved. This shift is not cosmetic. It is structural. Businesses that treat AI as a feature will fall behind those that redesign their development model around it.

By Gabriella Browne6 days ago in Journal

Comments

There are no comments for this story

Be the first to respond and start the conversation.