Faceing the 39% U.S. Tariff: A Coherent Strategy for Switzerland and its Watchmakers

39% U.S. Tariff: Swiss Watch Strategy 2025-2026

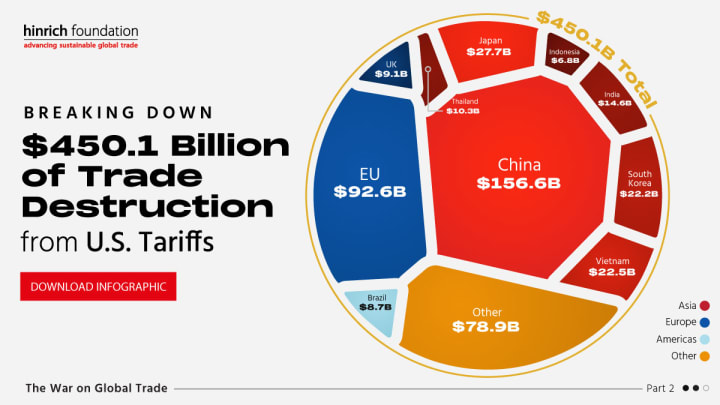

Background of the 39% Tariff

The United States has imposed an additional 39% ad valorem tariff on Swiss‑origin imports, including watches, effective August 7. The duty is determined by country of origin—not the shipping route or the last port of transit—so routing goods through third countries does not change liability. In practice, U.S. Customs will intensify checks on origin, valuation, and potential circumvention, raising the documentation bar for importers. Because luxury watches are high value, low weight, even small choices about when a shipment is formally entered, how it is stored, and which logistics programs are used can materially affect cash flow. The policy shock therefore interacts with multiple levers at once: trade rules, pricing power, supply‑chain design, currency moves, and brand stewardship.

What the 39% Tariff Means for Swiss Watches

Landed cost & pricing. The tariff creates a step‑change in landed costs. Most brands will blend partial pass‑through to MSRP with margin sharing across factories, distributors, and retailers. Expect stair‑step price adjustments concentrated first in low‑elasticity references (iconic steel sports, precious‑metal pieces, limited editions), while entry lines rely more on financing and value‑add bundles to defend conversion.

Demand & mix. High‑luxury halos remain relatively resilient; mid‑market and entry segments face greater price sensitivity and may shift buyers toward alternatives or certified pre‑owned (CPO). Portfolios will tilt toward fewer, stronger references, with materials and specification tweaks that raise perceived value without inflating the bill of materials.

Channels & control. Brands will tighten allocations and discount corridors for authorized dealers, lean more on direct‑to‑consumer boutiques and e‑commerce, and use CPO and after‑sales benefits to stabilize reference prices and curb grey‑market leakage.

Working capital & logistics. Duty‑deferral mechanisms (e.g., bonded storage, U.S. FTZ use), careful control of entry timing, and re‑sequencing of inbound POs help align cash‑out with sell‑through, as noted in Swiss Watch Exports Ticked Up in July Ahead of U.S. Tariffs. Given currency volatility, pragmatic FX hedging becomes more important to protect margins.

Compliance risk. The new regime raises the stakes on origin documentation, classification, and valuation. Any attempt to mask origin or route for evasion risks penalties that far exceed the tariff itself—making disciplined compliance a strategic, not just legal, priority.

In short, the 39% tariff is a cost shock that forces a system‑level response: thoughtful pricing, tighter channel management, sharper logistics and cash control, and unwavering compliance—executed in a way that preserves long‑term brand equity. For readers tracking real‑time pricing and availability in the German market, see koniguhren.de.

Switzerland’s Government Playbook (Expanded: renewed U.S. talks + non‑U.S. diversification)

Negotiate hard, broaden the agenda — a structured re‑engagement with the U.S.

Switzerland should return to the table with a two‑track approach that moves fast and signals seriousness, in line with Switzerland will pursue further talks with the U.S. over crippling tariffs:

Political track (principals‑level): Re‑open talks with a clear “landing zone”: (a) rate reduction ladder tied to measurable cooperation; (b) sector carve‑outs for repair/after‑sales parts and components; (c) time‑limited tariff‑rate quotas (TRQs) to avoid demand whiplash; (d) extended grace for bona‑fide in‑transit or returns/repairs flows.

Technical track (customs/industry working groups): Build a joint workplan on origin verification, anti‑circumvention, and data‑sharing, reducing friction at the border while addressing U.S. enforcement priorities.

Broaden the bargaining set: Pair tariff talks with cooperation in energy security, critical‑tech, and defense‑adjacent procurement transparency to create multiple paths to de‑escalation.

Business coalition & evidence pack: Convene maisons, suppliers, and U.S. retailers to present a shared, data‑driven impact brief (jobs, investment, consumer prices) and codify a “no‑transshipment” compliance pledge to strengthen negotiating credibility.

Communication discipline: Issue a joint progress note after each round—short, factual, and forward‑looking—to steady markets and discourage speculative pricing behavior.

30/60/90‑day deliverables:

30 days: Launch both tracks; table a written proposal with the reduction ladder + carve‑outs.

60 days: Provisional agreement on after‑sales/repairs corridor and a TRQ outline.

90 days: Convert technical understandings into an implementation protocol with monitoring and snap‑back clauses.

Stabilize competitiveness at home — make exporters stronger while talks proceed

Regulatory pacing: Defer or streamline cost‑adding but non‑safety regulations; adopt a “one‑in, one‑out” rule for new administrative burdens on exporters.

Export finance (scaled up and faster): Expand working‑capital guarantees, credit insurance, and short‑term pre‑shipment finance so firms can hold inventory longer and time entries without cash‑flow strain. Create a fast‑track channel for watch SMEs with simple, template‑based underwriting.

Skills & productivity: Co‑fund precision‑manufacturing training, micro‑credentials in CNC/micromechanics, and automation upgrades (assembly, testing, QC). Offer super‑deductions/accelerated depreciation for tooling and digitalization that demonstrably lift unit productivity.

Market‑maker support for diversification: Stand up a “Diversify Now” package that co‑finances market entry (legal, labeling, after‑sales set‑up) in priority regions, with shared storefronts at key fairs and a concierge program for retailer onboarding.

Diversify and signal confidence — a non‑U.S. growth agenda with targets

Switzerland should match U.S. engagement with a decisive push into other demand centers, turning risk into optionality:

Priority markets & channels:

Asia hubs: Singapore, Hong Kong, Japan, South Korea, selected ASEAN markets.

Middle East: UAE and Saudi retail ecosystems, anchored by travel retail and high‑service boutiques.

Europe & UK: Deepen premium doors and omnichannel clienteling; protect price integrity with stronger after‑sales guarantees.

Americas beyond the U.S.: Mexico and Chile as footholds where distribution quality supports premium positioning.

Go‑to‑market toolkit: National pavilions and “Swiss Watches Weeks” in tier‑1 cities; co‑op campaigns with top retailers; shared after‑sales academies to train local technicians; digital export acceleration for authorized e‑commerce.

Logistics & service spine: Build regional service centers (parts, polishing, regulation) to cut turnaround times and elevate ownership value; use duty‑efficient hubs to reduce lead times without compromising provenance.

Signals and scorecards: Publish a diversification dashboard (export concentration, non‑U.S. share, service turnaround, new doors opened). Markets respond to clarity; give them milestones and keep them updated.

Outcome: By re‑engaging Washington with a broader offer while funding competitiveness and pursuing non‑U.S. growth, Switzerland reduces near‑term damage, restores medium‑term leverage, and hardens the industry’s long‑run resilience—without sacrificing the integrity of Swiss watchmaking.

Brand Response Timeline — Expanded With Concrete Playbooks (Rolex, Swatch Group, etc.)

Phase 1 — Now through early Q4: Stabilize inventory and cash

1) Triage every shipment

What to do: Audit each PO by load date / ETA / entry date; fast‑track lots that can enter under more favorable timelines; split consignments so the fastest‑moving SKUs clear first.

Rolex (and Tudor): Prioritize allocations for Datejust, Submariner, GMT‑Master II and Tudor Black Bay to the highest‑velocity ADs; delay low‑turn precious‑metal variants if they risk tying up duty before peak demand.

Swatch Group (Omega, Tissot, Longines): Sequence Speedmaster/Seamaster, Tissot PRX/Seastar, and Longines Spirit/HydroConquest to doors with proven sell‑through; push slower novelty colors to regions with stronger elasticity.

Richemont (Cartier, IWC, Panerai): Clear Tank/Santos and Portugieser/Pilot first; schedule Panerai special references around boutique events to compress days‑to‑cash.

LVMH (TAG Heuer, Hublot, Zenith): Land Carrera and Formula 1 first for volume; hold boutique‑only Hublot editions until coordinated client previews shorten the cash cycle.

2) Use duty‑deferral tools (bonded/FTZ)

What to do: Park inbound inventory in bonded warehouses or FTZs; release just‑in‑time for confirmed sales; use FTZ for re‑exports and returns processing to avoid unnecessary duty.

Rolex: Centralize U.S. buffer stock for core steel references in a single zone to minimize multi‑state tax friction; pull units to ADs only against pre‑qualified client lists.

Swatch Group: Stand up a shared FTZ hub covering Omega/Tissot/Longines; kit straps/bracelets in‑zone so final contents match demand, reducing useless duty on unused accessories.

Richemont & LVMH: Use group logistics to consolidate brands in one or two zones; for travel‑retail flows, route via FTZ to keep re‑export pathways clean.

3) Prioritize high‑turn references

What to do: Allocate the lowest‑cost lots to hero SKUs with short sell‑through; protect price integrity by pairing them with after‑sales value rather than markdowns.

Examples: Rolex Oyster Perpetual/Datejust; Omega Seamaster Diver 300M; Tissot PRX Powermatic; TAG Heuer Carrera 39/42; Longines Spirit 37/40; Cartier Tank Must.

4) Hedge sensibly (FX & input costs)

What to do: Extend simple forwards/options on USD receivables; ladder maturities around key delivery windows; avoid speculative hedges.

Group play: Central treasuries (Swatch, Richemont, LVMH) net brand exposures; independents lock rolling 3–6‑month layers aligned to U.S. sell‑out plans.

Phase 2 — Q4 into year‑end: Reset price and allocation without losing the room

1) Stair‑step pricing (start where elasticity is lowest)

Rolex: Nudge precious‑metal Day‑Date/Sky‑Dweller and boutique allocations first; keep steel icons tight and let scarcity carry part of the pass‑through.

Swatch Group: Moderate increases on Omega flagship lines; keep Tissot entry points sharp to defend the on‑ramp; use limited dials/editions to justify higher brackets without training for discount.

Richemont: Lift on Cartier precious‑metal Tanks/Santos skeletons and IWC complications; hold line on steel starters.

LVMH: Take price on Hublot limited ceramics/precious metals and selected Zenith El Primero; keep TAG Heuer core Carreras competitive.

2) Value over discount (protect reference prices)

Toolbox: Extended warranty terms, first service credit, strap/bracelet bundle, priority access to future drops.

Examples:

Rolex/Tudor: clienteling perks (priority allocation, service appointments) instead of markdowns.

Omega: bundle a complimentary strap + spring bars or first regulation voucher with Speedmaster purchases.

TAG Heuer/Tissot: offer seasonal strap packs and no‑fee installments to offset sticker shock.

Cartier: complimentary engraving/adjustment and express after‑sales to enhance perceived value.

3) Channel concentration (feed the winners)

What to do: Shift inventory to top‑quartile ADs and owned boutiques; narrow wholesale terms where sell‑through lags; tie replenishment to clean inventory KPIs.

Rolex: Tighten allocations to ADs with deep client books and minimal leakage; enforce stricter waitlist hygiene.

Swatch Group (Omega): Favor boutiques and high‑service doors; reserve novelty drops for doors that hit service and CRM targets.

Richemont/LVMH: Expand appointment‑led selling; link replenishment to CPO trade‑ins to keep clients inside the brand ecosystem.

Phase 3 — 2026 and beyond: Re‑architect for structural resilience

1) Portfolio tiering (protect halos, broaden ladders carefully)

Rolex: Keep the entire portfolio Swiss‑Made; rely on scarcity management and after‑sales excellence rather than provenance changes.

Swatch Group:

Omega: Double down on Swiss‑Made craftsmanship and Master Chronometer messaging; use limited technical editions to command price power.

Tissot/Longines: Maintain Swiss‑Made cores; where brand‑safe, incubate clearly labeled value lines (e.g., different sub‑labels) that use Swiss movements but lighter specifications to hold key price points—without blurring provenance.

Richemont/LVMH: Keep maisons’ halos pristine; if broader ladders are needed, launch them under distinct sub‑brands rather than diluting flagship identities.

2) U.S. footprint (service‑led resilience)

What to do: Expand regional service centers (inspection, regulation, polishing), parts depots, and strap/accessory programs in the U.S. to raise LTV without extra import duty.

Examples:

Rolex: more capacity for same‑week regulation/pressure tests in major metros.

Omega: Speedmaster and Seamaster fast‑track lanes with loaner watches for VIPs.

Cartier/IWC/TAG Heuer/Tissot: publish turnaround SLAs (e.g., 10–15 business days) and meet them.

3) Network design (duty‑smart, client‑first)

What to do: Add FTZ nodes in key corridors to defer duty until consumption; centralize returns/repairs through zones to avoid double taxation; evaluate final kitting/packaging in‑zone (does not change origin) to match actual orders.

Rolex: Single national zone for core models; ship just‑in‑time to ADs against confirmed clients.

Swatch Group: Multi‑brand FTZ with shared QC and kitting cells to flex inventory between Omega/Tissot/Longines.

Richemont/LVMH: Group‑level zoning to harmonize compliance and speed cross‑brand reallocation during launches.

Quick brand cheat‑sheet (what “good” looks like):

Rolex: Scarcity + immaculate service; tiny, targeted MSRP moves; zero discounting; airtight allocations.

Omega (Swatch Group): Technical credibility + boutiques; value bundles over markdowns; defend entry via Tissot.

Tissot/Longines: Keep entry points compelling; accessories/financing to ease first‑time buyers; watch leakage vigilantly.

Cartier/IWC (Richemont): Elevate after‑sales theater; protect icons; allocate by CRM performance.

TAG Heuer/Hublot/Zenith (LVMH): Price power via limited tech/materials; Carrera/El Primero carry velocity; boutique‑first for storytelling.

Bottom line: Treat Phase 1 as a cash and compliance bridge, Phase 2 as a pricing and allocation reset, and Phase 3 as a structural rebuild that protects Swiss halos while preserving accessible rungs. The names may differ by maison, but the winning sequence is the same.

Conclusion

The 39% tariff is a stress test—but it is also a strategy test. Switzerland must negotiate from strength while cushioning exporters at home. Brands must act with sequence and focus: stabilize now, reset through year‑end, and rebuild for durability. The winners will be those who treat this not as a one‑off tax shock, but as the catalyst to refine pricing power, operational agility, and the value story that made Swiss watchmaking desirable in the first place.

About the Creator

Silver Screen Magic with Mae West

American actress and singer Mae West became a popular film actress during the Great Depression. She started entertaining in vaudeville, then performed on Broadway, and finally went to Hollywood. She signed up with Paramount Pictures and made her debut in the 1932 film “Night After Night.” She also starred in musicals, comedies, and crime dramas. The American Film Institute named her one of the best classic Hollywood actresses.

By Rasma Raisters6 days ago in Geeks

Michael Vartan

Michael Vartan has long been one of Hollywood’s most recognizable yet understated actors. Known for his charm, emotional range, and consistent performances, Vartan built a career that resonated strongly with television audiences, particularly during the early 2000s. While he may not dominate headlines today, interest in Michael Vartan now reflects how lasting his impact has been on fans who grew up watching his work. Early Life and Entry Into Acting Michael Vartan was born on November 27, 1968, in Boulogne-Billancourt, France. Raised between France and the United States, he grew up in a multicultural environment that shaped his worldview. His mother was an American artist, and his father was a French actor and writer, which gave him early exposure to the creative world. Before acting became a serious pursuit, Vartan worked behind the scenes in the film industry. He served as an assistant to directors, gaining firsthand experience with the mechanics of filmmaking. This background gave him a grounded understanding of storytelling—an element that later showed in the depth and restraint of his performances. Breakthrough Roles and Rising Popularity Michael Vartan’s acting career began in the 1990s with roles in films such as The Pallbearer and Never Been Kissed. While these projects introduced him to mainstream audiences, his true breakthrough came with television. In 2001, Vartan was cast as Michael Vaughn in the spy drama Alias. The show quickly became a cultural phenomenon, and his portrayal of the calm, morally driven CIA agent earned widespread praise. His on-screen chemistry with Jennifer Garner played a significant role in the series’ success and cemented Vartan’s status as a fan favorite. Alias allowed Michael Vartan to showcase more than just leading-man appeal. His character balanced action with emotional vulnerability, making him relatable despite the high-stakes spy narrative. For many viewers, this role remains the defining chapter of his career. Career After Alias Following the end of Alias, Michael Vartan continued working steadily in both television and film. He appeared in movies like Monster-in-Law and One Hour Photo, demonstrating his willingness to explore varied genres. On television, he took on leading and supporting roles in shows such as Hawthorne, Bates Motel, and The Arrangement. These performances reflected a shift toward more mature, nuanced characters, aligning naturally with his growth as an actor. Rather than chasing constant visibility, Vartan seemed selective, choosing projects that interested him creatively. This approach contributed to his reputation as a dependable and thoughtful performer rather than a celebrity driven by trends. Michael Vartan Now: Life Away From the Spotlight When people search for Michael Vartan now, they are often curious about why he appears less frequently on screens. The answer is not controversy or retirement, but balance. In recent years, Vartan has stepped back from high-profile roles, focusing more on personal life and selective professional opportunities. He has spoken openly in the past about the pressures of fame and the importance of mental health. This honesty resonated with fans and helped explain his quieter presence in Hollywood. Instead of constant exposure, Michael Vartan now represents a different model of success—one defined by longevity and personal well-being. Though he is not as active as he once was, he remains connected to the industry and continues to receive interest from both creators and audiences. His legacy ensures that his work is still revisited by new viewers discovering his shows through streaming platforms. Acting Style and Lasting Appeal What sets Michael Vartan apart is his subtlety. He is not known for over-the-top performances or dramatic transformations. Instead, his strength lies in emotional authenticity. Whether playing a spy, a doctor, or a troubled partner, his characters often feel grounded and believable. This realism helped him maintain relevance across different eras of television. His performances age well because they rely on human emotion rather than stylistic trends. For fans revisiting his work today, that quality remains just as compelling. Cultural Impact and Fan Connection While Michael Vartan may not dominate social media or entertainment news cycles, his fan base remains loyal. Online discussions, rewatch threads, and renewed interest in shows like Alias continue to introduce his work to younger audiences. His career serves as an example of how consistency and integrity can leave a lasting impression without constant self-promotion. In an industry that often rewards noise, Vartan’s quieter approach stands out. Final Thoughts Michael Vartan’s journey through Hollywood reflects a career built on steady growth, thoughtful choices, and respect for the craft of acting. From his early days behind the camera to his memorable television roles, he carved out a space that remains relevant even years later. For those wondering about Michael Vartan now, the answer is simple: he is living on his own terms, with a legacy already firmly established. His story reminds us that success in entertainment does not always mean being everywhere—it can also mean being remembered.

By Saboor Brohi 4 days ago in Geeks

Comments

There are no comments for this story

Be the first to respond and start the conversation.