Toronto Dominion: Set For A Good 2021, But A Return To Pre-COVID Performance Now Reflected In The Share Price

It might have been difficult to imagine Toronto Dominion ( TD) making the financial gains it has recently a year ago

It might have been difficult to imagine Toronto Dominion ( TD) making the financial gains it has recently a year ago. It was clear that the economic environment back then was very scary. The early economic data was unlike anything ever before. It is not necessary to add any commentary on the potentially disastrous impact of credit losses on bank stocks. The fact that TD, a Canadian giant, has managed to comfortably keep its dividend streak may be a good indicator of how resilient the industry has been.

As with most industry players, the bank still feels a pinch of reality. Lower interest rates have put pressure on the bank's interest income. TD also saved C$7.2b last year for bad debt. This was an increase of just under C$3b in 2019, and C$2.5b for 2018, respectively. However, there are a few things that have prevented it from getting worse. First, the extraordinary downturn was met with a similarly unprecedented fiscal and monetary response by the authorities. TD also created its own loan deferral programs to help customers in need. The stimulus measures have also resulted in record profits for the investment banking segment of TD. This has helped to fill some of the gaps elsewhere. Also, the bank realized a substantial gain last year from the sale to Charles Schwab of broker TD Ameritrade. It retains a 13.5% share.

The bank was first featured here in September. I suggested that it was well worth a closer inspection. The stock had a 5.1% dividend yield, making it an attractive investment choice. Its stock, which is a play on Canada's economy and households and, to a lesser degree, the United States, likely means that it has a base case long term outlook of 5% in terms of annual growth. The starting yield of 5% or more was acceptable, even with the uncertainties caused by COVID and other factors. I like the bank very much, but the stock has risen to record heights since my last coverage makes it less appealing as an investment.

Core Business Shows Resilience

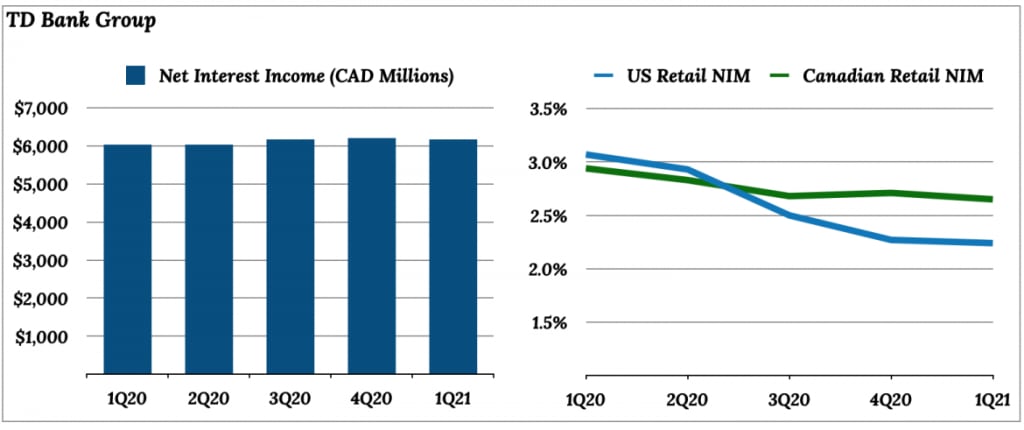

While core numbers for TD have been fairly stable, I believe its US retail business has been a significant drag relative to Canadian peers. It is obvious that the bank faces a challenge in terms interest income. In the bank's fiscal 1st quarter, interest margins fell sequentially on both sides. This was partially offset by an increase in domestic mortgage volume. Canada's housing market looks white hot right now - worth noting since loan growth elsewhere looks tough - and Canadian mortgages on the loan book increased by circa C$3.5b quarter-over-quarter. Nonetheless, this dynamic resulted in a sequentially flat net income of C$6b in Q1.

Interest income isn't the only thing that matters. TD is not the only bank that has seen a boost in non-interest income during this downturn. While the numbers were up last year due to the TD Ameritrade gain, the underlying performance is now better. There are still some areas that remain subdued. Credit card fees are still lower than pre-COVID levels. Other lines, such as transaction-based Wealth and fee, have made up the difference. The non-interest income from the Canadian retail sector grew 11% last quarter to C$3.4b. This is more than offset by the tougher numbers south.

The profit numbers for wholesale banking continue to rise compared to its pre-COVID baseline. The 13.5% Schwab stake, which is located in the US retail segment, generates approximately C$240m in quarterly profits at the moment.

Provision Expense Slides

All of this adds up to decent numbers for the core business. Based on straight math, I had a pre-provision profit after tax of around 5-6% in the last quarter. It's quite impressive, even though it was lower than Canadian peers due to US retail. However, this was boosted by a 15-year low provision cost for bad debt. TD had only C$313m of reserves in the first quarter. This is a decrease of around C$600m from the year before COVID. This is due to the large amount that was set aside for fiscal 2020 and ongoing stimulus measures. The above resulted in double-digit profit growth for the first quarter. After-tax profit was C$3.2b or C$1.77 per Share, an increase of around 10% over the previous year.

Outlook

Investors have obvious exposure to Canadian households. This is a country where the bubble talk about the housing market is not new. Over the years, price-income ratios have risen dramatically and households are taking on more debt. The 20-25% annual increase in house prices will only make matters worse. Approximately 40% of TD's loan book is for Canadian residential real property. Because of Canada's regulatory environment, the bank is not as vulnerable to defaults. The bank is also known for being a conservative underwriter with reasonable LTV ratios. However, future income growth risks are clear enough.

The bank also has some levers that it can pull. Performance in line with GDP may translate into higher profits if the bank can save money on costs. This is evident in the ongoing push for digital and mobile banking. Management seems to be keen to expand south of the border and possibly use the Schwab stake for funding. The US retail sector is less quality than its counterpart in Canada, as TD has key disadvantages there. However, it is still a good business and the US has excellent long-term growth prospects.

Currently, TD stock trades in Toronto at around C$82.25. Analysts now predict EPS of C$6.80 per shares, which would put the stock at 12x earnings. The quarterly dividend is still at C$0.79 per shares, but growth is expected to resume this year. The retained profit generation has helped to increase capital levels. TD's CET1 ratio was 13.6% at the last count. This is in line with the overall economic outlook that the vaccines have provided. It seems clear that regulators will allow for further dividend growth. Current dividend yields around 3.8%. Long-term, I believe the bank's nature supports a growth rate of about 5%. The shares are probably at fair value right now if we discount that to the present.

About the Creator

Keep reading

More stories from Melody Smith and writers in Trader and other communities.

Australia Construction Market: Infrastructure Expansion, Urban Growth & Industrial Momentum

Australia Construction Market Overview The Australia construction market remains a key driver of economic activity, employment and long-term growth, reflecting robust investment in public infrastructure, residential building, commercial developments and industrial facilities. The Australia construction market size was valued at USD 420.5 Billion in 2025. Looking forward, the market is expected to reach USD 603.0 Billion by 2034, exhibiting a CAGR of 4.09% from 2026-2034. The market is driven by the growing government infrastructure spending, economic expansion, which is leading to the construction of commercial, residential, and mixed complexes, and advanced technologies and sustainability trends. This sustained expansion stems from government infrastructure programmes, urbanisation trends, rising housing demand, and private sector investment in commercial and industrial projects. As Australia positions itself for future growth, the construction sector continues to mirror economic resilience, evolving policy focus and the shift toward sustainable development.

By Amyra Singh6 days ago in Trader

How, Too

Many people wonder how, too. You are not alone, and I am an expert. I will teach you how, too! First, you need to remit a small application fee and fill out an application describing the nature of your financial situation and how often payments will be made, as this will have great bearing on how well I teach you how, too.

By Harper Lewis3 days ago in Fiction

Comments

There are no comments for this story

Be the first to respond and start the conversation.