Smart Investment Strategies for Single Mothers: Practical and Accessible Tips

Practical and Low-Cost Investment Strategies Every Single Mother Can Use to Build Financial Security and Independence

Balancing the role of both parent and provider is no small task. For single mothers, every dollar has a purpose, and financial decisions often come with weighty consequences. In this environment, investing may feel like a luxury reserved for those with more disposable income or fewer responsibilities. Yet, that perception keeps many from building the financial security they truly deserve.

The reality is that investing isn’t just for the wealthy—it’s for anyone willing to start small, stay consistent, and think long-term. For single mothers, investments can be more than just numbers on a statement; they represent stability, empowerment, and a future where financial stress takes up less space in daily life.

Why Investing Matters for Single Mothers

Parenting alone means that the financial safety net is thinner. There’s no partner to lean on if income drops or unexpected bills arrive. That’s where investing steps in—not as a quick fix, but as a strategy to gradually build resilience.

When you invest, you’re not just chasing returns. You’re creating:

- Wealth that compounds over time. Even small contributions grow exponentially through the power of compound interest.

- Protection for your children’s future. Money saved and invested today can later cover tuition, housing, or help them get a strong start in life.

- Independence from debt. Investing helps shift the focus away from short-term borrowing and toward long-term security.

Think of it this way: investing is planting seeds. At first, the growth is hard to notice. But with time, those seeds turn into something strong, rooted, and dependable.

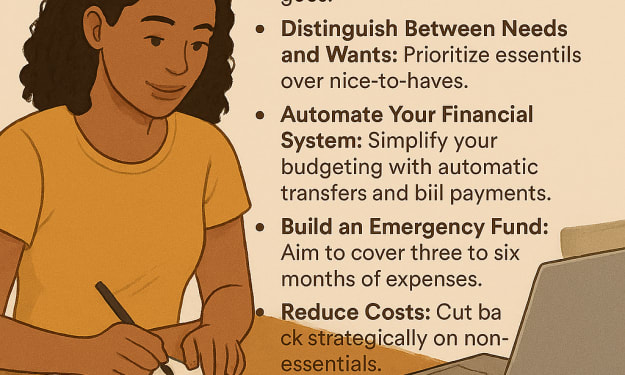

Before diving into investment accounts or stocks, your priority should be an emergency fund. This isn’t just another savings goal—it’s a lifeline.

Life happens, and for single mothers, disruptions hit harder. A flat tire, a medical bill, or a cut in work hours can quickly unravel financial plans. Having a cushion means those events don’t force you into credit card debt or early withdrawals from investment accounts.

What a strong emergency fund looks like:

- Three to six months of necessary expenses. Think rent, groceries, utilities, transportation—not luxuries.

- Stored in a high-yield savings account. This ensures it grows a little, while still being accessible.

- Separate from checking. Keeping it distinct helps prevent accidental spending.

Once this foundation is in place, you can approach investing without fear of pulling money out too soon.

Investment Options That Work for Tight Budgets

The idea of investing often conjures up images of Wall Street brokers or people with stacks of cash. Thankfully, modern tools have changed that narrative. With just a few dollars a month, you can begin building wealth.

1. Employer-Sponsored Retirement Plans

If your workplace offers a 401(k) or similar plan, take advantage of it. Even contributing a small portion of your paycheck—say 3%—can snowball over decades. If your employer matches contributions, it’s essentially free money that accelerates growth.

2. Roth IRA or Traditional IRA

An IRA (Individual Retirement Account) is designed for long-term growth. The Roth IRA, in particular, is a powerful tool for single mothers. Contributions are made with after-tax income, but withdrawals in retirement are tax-free—making it ideal for those expecting higher future tax rates.

3. Index Funds and ETFs

Rather than betting on individual companies, index funds spread your money across hundreds of businesses. They’re cost-effective, simple to manage, and have historically provided steady returns. Think of them as a basket of investments working for you, even when you’re not watching the market every day.

4. Micro-Investing Apps

Platforms like Acorns or Stash make investing approachable. They allow you to start with spare change—literally. These apps round up everyday purchases and invest the difference. It’s a subtle, low-pressure way to grow money over time.

5. 529 Plans for Education

If college savings are a priority, a 529 plan offers tax benefits and long-term growth. Contributing even $25 a month can make a significant difference when compounded over 10–15 years.

How to Begin: Actionable Steps

- Starting is often the hardest part. But momentum builds quickly once the first steps are taken.

- Review your budget. Identify areas where even $25–$50 per month can be redirected toward investments.

- Set up automatic contributions. Automation ensures consistency and reduces the temptation to skip.

- Choose your first account. Whether it’s a Roth IRA, 401(k), or a micro-investing app, begin with one platform before spreading out.

- Track progress monthly. Watching your investments grow reinforces the habit and keeps motivation strong.

- Adjust as life changes. Income, expenses, and goals shift—your investment plan should evolve too.

Avoiding Common Missteps

It’s easy to get caught up in mistakes, especially with so many voices offering “advice.” Protect yourself by staying grounded.

- Don’t invest money you need soon. Short-term savings should remain separate from long-term investments.

- Resist trendy hype. High-risk opportunities like speculative crypto coins often lead to losses.

- Watch out for hidden fees. A fund with a 1% fee may not seem like much, but over decades, it can eat away thousands in returns.

- Diversify. Spreading money across multiple assets reduces the risk of major losses.

Building Confidence in Your Financial Journey

Single mothers often underestimate their financial strength. Remember, the act of investing—even a modest amount—is already a victory.

- Celebrate milestones. Every time you reach a new savings target or make a consistent contribution, acknowledge it.

- Prioritize consistency over perfection. Missing one month doesn’t erase years of effort. Keep moving forward.

- Learn continuously. Explore personal finance books, podcasts, or workshops designed for beginners. The more you know, the more empowered you’ll feel.

- Find community. Many local organizations, online groups, and even banks host free financial literacy sessions geared toward women and parents.

The Bigger Picture: Long-Term Security

At its core, investing isn’t about making quick money—it’s about building a future that feels less uncertain. For single mothers, the goal is stability, choice, and peace of mind. The ability to cover emergencies, support children, and enter retirement with dignity starts with small steps today.

Remember: You don’t need to be an expert. You don’t need thousands to start. What matters most is the commitment to begin, stay consistent, and let time do the heavy lifting.

Investing is not about how much you have at the beginning. It’s about starting where you are, using accessible tools, and building momentum. For single mothers, this approach transforms investing from something intimidating into a pathway toward financial security and independence.

About the Creator

Richard Bailey

I am currently working on expanding my writing topics and exploring different areas and topics of writing. I have a personal history with a very severe form of treatment-resistant major depressive disorder.

Keep reading

More stories from Richard Bailey and writers in Trader and other communities.

Smart Budgeting for Working Women: Practical and Achievable Strategies

Managing money isn’t just about spreadsheets and calculators—it’s about shaping a life that supports your goals, values, and priorities. For working women, budgeting carries unique challenges.

By Richard Bailey4 months ago in Trader

Stanislav Kondrashov on Greenland’s Strategic Role in the Future of Global Trade and Resources

By all appearances, Greenland is on the brink of becoming one of the world’s most closely watched regions—not for its glaciers, but for what lies beneath and beyond them. Stanislav Kondrashov, economic analyst and founder of TELF AG, has recently cast a spotlight on the island’s rising significance in global trade and resource strategy. And his perspective is clear: Greenland is not just a geographical outlier—it is a future linchpin.

By Stanislav Kondrashova day ago in Trader

Blox Stock: Investors Are Taking Notice Here’s Why

Blox stock has been gaining attention lately, and many investors are wondering if it’s the right time to buy. With its recent surge and growing market interest, blox stock is becoming a stock to watch closely. They will break down what makes blox stock appealing, analyze trends, and explain why it could play an important role in your investment portfolio.

By John.doe798a day ago in Trader

Comments

There are no comments for this story

Be the first to respond and start the conversation.