Smart Budgeting for Working Women: Practical and Achievable Strategies

Discover practical budgeting tips for working women that simplify money management, reduce financial stress, and help you achieve long-term financial independence

Managing money isn’t just about spreadsheets and calculators—it’s about shaping a life that supports your goals, values, and priorities. For working women, budgeting carries unique challenges.

You might be balancing career demands with family responsibilities, dealing with wage gaps, or planning for both short-term stability and long-term independence. On top of that, unexpected costs—from car repairs to childcare—can make sticking to a financial plan feel nearly impossible.

But here’s the truth: budgeting doesn’t have to be complicated or restrictive. It can be empowering, flexible, and designed to fit your lifestyle. The key lies in creating a plan that feels realistic and achievable, not overwhelming or punishing.

This article dives into budgeting tips for working women that are both practical and detailed. Instead of vague advice like “just save more,” we’ll cover strategies you can implement today, plus deeper insights into why these steps work in real life.

Why Budgeting Matters for Working Women

For many women, money is closely tied to security and independence. Budgeting gives you the ability to make decisions from a place of strength, not stress. Without it, financial choices can feel reactive—responding to bills and emergencies as they come instead of being prepared.

A solid budget can:

- Provide clarity: Knowing exactly where your money goes helps eliminate that constant feeling of “where did it all disappear?”

- Create control: You choose how your money is spent instead of letting small, unnoticed expenses control you.

- Build confidence: When emergencies arise, you don’t panic—you already have a plan.

- Support your goals: From buying a home to retiring early, budgeting makes dreams actionable rather than distant wishes.

For working women especially, budgeting helps navigate unique financial realities such as childcare expenses, gender pay gaps, or career breaks for family care. With a clear plan, these challenges become manageable, not roadblocks.

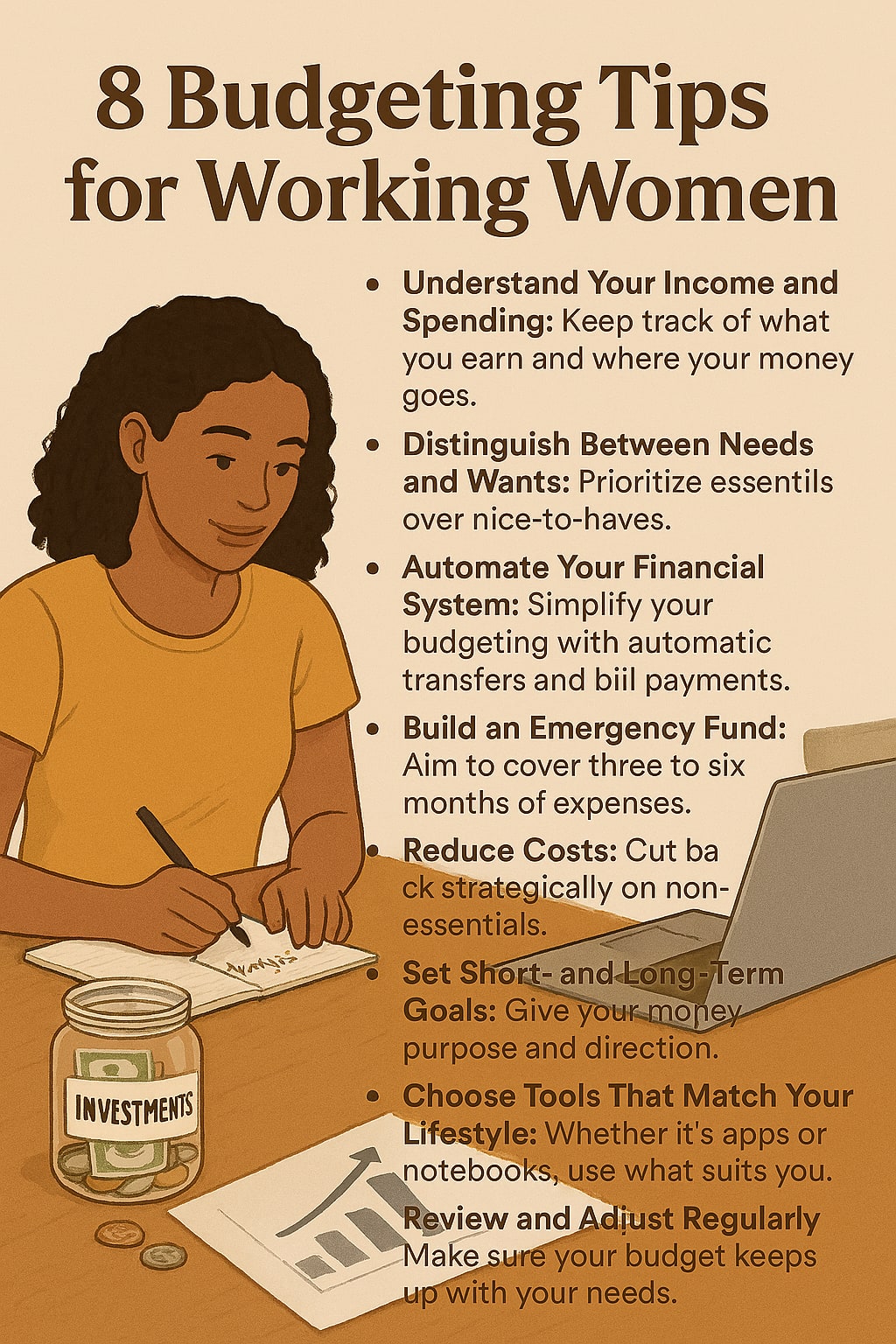

Step 1: Understand Your True Income and Spending Habits

Budgeting starts with knowledge. Most people know their salary but overlook the reality of net income—the amount you actually take home after taxes, insurance, retirement contributions, and other deductions. That’s your real starting point.

The next step is tracking spending, and this part often surprises people. Fixed bills like rent and utilities are easy, but discretionary spending is where money slips away unnoticed.

- That $4 coffee every workday? Over $80 per month.

- Subscription services you rarely use? Easily $30 to $50 monthly.

- Impulse buys at the grocery store? They add up.

For at least a month, write down every expense. Use an app if you prefer, or a simple notebook. The point is accuracy—don’t round numbers or estimate. Seeing your exact spending patterns is eye-opening and gives you a baseline for change.

Step 2: Distinguish Between Needs and Wants

Once you know where your money is going, organize your expenses into three categories:

- Needs: Housing, groceries, utilities, transportation, insurance.

- Wants: Dining out, streaming services, shopping, hobbies.

- Savings & Debt Payments: Emergency fund, retirement, loan payments, credit cards.

- Here’s the mindset shift: savings aren’t optional. They belong in the “needs” column because your future depends on them.

Example: If you earn $3,500 monthly after taxes:

- Needs might take $2,000.

- Wants could be $700.

- The rest—$800—should be divided between savings and debt repayment.

This isn’t rigid math; it’s a framework. You can adjust percentages, but always prioritize future security over short-term splurges.

Step 3: Automate Your Financial System

Many women are busy balancing career, home, and personal life, so remembering every due date is unrealistic. Automation makes budgeting almost effortless.

Savings: Schedule automatic transfers the day after payday. Even $50 weekly builds momentum.

Bills: Set recurring payments for utilities, credit cards, or rent to avoid late fees.

Sinking funds: Automate small amounts into separate accounts for predictable expenses like holidays, birthdays, or car maintenance.

By automating, you protect yourself from forgetting, overspending, or procrastinating. Money moves before you have the chance to use it elsewhere.

Step 4: Build an Emergency Fund for Peace of Mind

Life is unpredictable. Medical bills, job layoffs, or car breakdowns happen when you least expect them. An emergency fund is your safety net.

Experts recommend three to six months of living expenses. That might sound overwhelming, so start small. Saving $500 is an excellent first milestone, enough to cover minor emergencies without derailing your budget.

To grow your emergency fund faster:

- Save tax refunds or work bonuses.

- Sell unused items online.

- Use cashback rewards and deposit them directly into savings.

The key is keeping this fund separate from your regular checking account. Out of sight often means out of temptation.

Step 5: Reduce Costs Without Sacrificing Enjoyment

A budget shouldn’t feel like punishment. Instead, it should maximize value from your money while cutting waste.

- Audit subscriptions: Cancel or pause services you don’t actively use.

- Cook smarter: Batch-cook meals or use slow cookers to save both money and time.

- Shop strategically: Use coupons, cashback apps, or wait for seasonal sales.

- Negotiate bills: Many service providers lower rates if you ask, especially when competitors offer better deals.

- Think of it this way: if you cut $100 in waste each month, that’s $1,200 annually. Redirect that toward debt or savings and watch your financial picture transform.

Step 6: Set Short- and Long-Term Financial Goals

Money management feels easier when it’s tied to something meaningful. Write down specific goals for different timelines:

- Short-term (within 1 year): Pay off a credit card, save for a vacation, or build your first $1,000 emergency fund.

- Medium-term (1–5 years): Buy a car, move to a new home, or save for continuing education.

- Long-term (10+ years): Retirement, buying property, or building generational wealth.

Having concrete goals gives purpose to every dollar saved. Instead of feeling like you’re depriving yourself, you’re working toward something exciting and rewarding.

Step 7: Choose Tools That Match Your Lifestyle

Budgeting doesn’t have to mean using the latest app. The best system is the one you’ll actually stick with.

- Apps like Mint or YNAB: Perfect if you prefer digital tracking and reminders.

- Bank alerts: Great for catching overspending in real time.

- Spreadsheets: Ideal if you enjoy customization and control.

- Cash envelope method: Old-school but powerful for visual spenders who want to see exactly how much is left.

Experiment and adjust. If one tool feels too complicated, switch. The best budget is the one you can maintain long term.

Step 8: Review and Adjust Regularly

A budget isn’t set in stone—it’s a living document. Life changes, so your financial plan should too.

- Got a raise? Redirect a portion into savings before adjusting lifestyle expenses.

- New expenses, like childcare? Rebalance your categories to stay realistic.

- Overspent one month? Don’t quit. Learn from the mistake and adapt.

Checking in monthly helps keep your budget aligned with reality. Over time, quarterly reviews are enough once you’ve built steady habits.

For working women, budgeting is less about rigid restriction and more about creating flexibility, security, and independence. It’s about knowing your numbers, setting priorities, and making conscious choices that reflect your values and future goals.

Start small. Track your spending, automate savings, and focus on one change at a time. Over months, those habits build momentum. Over years, they create stability and freedom.

Budgeting isn’t just about money—it’s about peace of mind, empowerment, and shaping a life where you’re in control.

About the Creator

Richard Bailey

I am currently working on expanding my writing topics and exploring different areas and topics of writing. I have a personal history with a very severe form of treatment-resistant major depressive disorder.

Keep reading

More stories from Richard Bailey and writers in Trader and other communities.

Simple Investment Strategies That Work for Beginners

Starting your investment journey can feel like stepping into a world filled with jargon, charts, and endless advice. Many beginners delay investing because they’re worried about making costly mistakes, or they think they need a finance degree to succeed. The truth is far simpler: building wealth doesn’t require complicated strategies or constant trading.

By Richard Bailey6 months ago in Trader

Australia Grocery Retail Market Growth, Forecast, and Strategic Insights by 2034

The grocery retail sector plays a vital role in Australia’s economy, serving millions of consumers who rely on supermarkets, convenience stores, and online platforms for everyday essentials. Over the past decade, the industry has evolved significantly as retailers adapt to changing consumer preferences, technological innovations, and new competitive pressures.

By Amélie Belleabout 10 hours ago in Trader

Comments

There are no comments for this story

Be the first to respond and start the conversation.