Japan Pet Food Market Size and Forecast, 2026–2034

Premium Nutrition, Aging Pets, and Humanization Trends Redefine Japan’s Pet Food Industry

Market Snapshot

The Japan Pet Food Market is projected to expand significantly, growing from US$ 6.72 billion in 2025 to US$ 14.68 billion by 2034, registering a robust CAGR of 9.07% during the period 2026–2034. This growth is being driven by rising pet ownership, increasing pet humanization, strong demand for premium and functional nutrition, and growing awareness around pet health, aging, and preventive care.

Despite Japan’s declining population, the pet food sector remains one of the country’s most resilient consumer markets. Higher per-pet spending, sophisticated consumer preferences, and innovation in nutrition science continue to shape a market that prioritizes quality, safety, and tailored dietary solutions.

Japan Pet Food Market Outlook

Pet food refers to commercially prepared products formulated to meet the nutritional requirements of domesticated animals such as dogs, cats, birds, and fish. These foods are designed to deliver balanced proportions of proteins, fats, carbohydrates, vitamins, and minerals necessary for growth, energy, immunity, and long-term health. They are offered in multiple formats—dry kibble, wet and canned foods, semi-moist options, treats, and therapeutic diets—often customized by life stage, breed size, and medical condition.

In Japan, pet food consumption has become increasingly sophisticated. The country’s demographic structure—characterized by an aging population, rising numbers of single-person households, delayed marriages, and shrinking family sizes—has transformed pets into emotional companions and family members. As a result, Japanese pet owners are more willing than ever to invest in high-quality nutrition, particularly for small dog breeds, indoor cats, and senior animals.

Limited living space in urban centers has further shaped consumption habits, creating demand for portion-controlled packaging, easy-to-store formats, and specialized indoor pet diets. Health, longevity, and disease prevention have emerged as central themes in purchasing decisions, ensuring that the market continues to grow even as the overall pet population stabilizes.

Key Growth Drivers in the Japan Pet Food Market

Increasing Humanization of Pets

One of the most powerful forces reshaping the Japanese pet food market is the growing emotional bond between owners and their animals. Pets are no longer viewed as companions alone; they are increasingly treated as family members. This cultural shift is closely linked to societal trends such as delayed marriage, fewer children, urban isolation, and an aging population seeking companionship.

Pet owners now prioritize nutrition standards similar to those they apply to their own diets. This has driven strong demand for premium, super-premium, and “human-grade” products that emphasize ingredient transparency, safety, and ethical sourcing. Japanese consumers are particularly attentive to labeling, production standards, and brand reputation, reinforcing the importance of trust and reliability in purchasing decisions.

As of 2023, approximately 397,000 dogs and 369,000 cats were newly adopted into Japanese households, reflecting steady inflows despite demographic constraints. Older adults and single-person households in urban areas increasingly rely on pets for emotional support, further reinforcing spending on specialized and high-quality nutrition.

Rising Demand for Health-Focused and Functional Nutrition

Health and wellness have become defining themes in Japan’s pet food industry. Pet owners are highly aware of the relationship between diet, longevity, and quality of life. This has accelerated demand for functional pet foods targeting digestive health, joint mobility, skin and coat care, kidney support, weight management, and stress reduction.

The aging pet population is a particularly strong growth driver. With dogs and cats living longer due to better veterinary care and nutrition, age-specific diets are in high demand. Products formulated for senior pets now include enhanced protein profiles, controlled fat levels, and added supplements such as glucosamine, omega-3 fatty acids, and antioxidants.

Veterinary endorsement plays a critical role in shaping consumer behavior. Japanese pet owners exhibit high trust in scientifically developed and clinically tested products. Reflecting this trend, in January 2025, Hill’s Pet Nutrition introduced new additions to its Prescription Diet portfolio, including low-fat dog food and stress-management formulations for cats—highlighting the growing intersection between clinical care and everyday nutrition.

Premiumization and Convenience-Driven Innovation

Japan’s highly urbanized lifestyle has made convenience a central factor in purchasing decisions. Smaller living spaces, busy work schedules, and changing household structures are fueling demand for easy-to-store, ready-to-serve, and portion-controlled pet food formats. Single-serve wet food pouches, resealable packaging, and customized “meal-style” offerings are becoming increasingly popular.

At the same time, premiumization continues to reshape the market. Consumers are moving beyond basic nutrition toward high-value propositions centered on ingredient quality, traceability, safety standards, and functional benefits. Japanese buyers are willing to pay higher prices for trusted brands that deliver consistent quality and meet stringent regulatory and ethical benchmarks.

E-commerce, subscription services, and home delivery platforms are also expanding rapidly, adding another layer of convenience. These channels enable recurring purchases, personalized product recommendations, and broader access to specialty diets. In November 2023, Unicharm strengthened its domestic operations with the opening of a new Peparlet manufacturing facility in Shizuoka, reflecting ongoing investments in capacity, innovation, and supply chain efficiency.

Challenges in the Japan Pet Food Market

Declining Pet Population and Demographic Shifts

While per-pet spending continues to rise, Japan’s overall pet population faces long-term structural challenges. A shrinking national population, low birth rates, urban housing restrictions, and an aging society have reduced the number of new pet adoptions in recent years. Many rental properties restrict pet ownership, particularly in densely populated urban areas, limiting market expansion by volume.

As a result, manufacturers must increasingly rely on premiumization, functional innovation, and niche targeting rather than unit growth. Expanding into segments such as senior nutrition, wellness supplements, and therapeutic diets has become essential for sustaining long-term growth.

High Competition and Stringent Quality Expectations

The Japanese pet food industry is intensely competitive, featuring strong domestic players alongside global multinationals. Consumer expectations regarding safety, quality, and ingredient disclosure are among the highest in the world. Regulatory compliance, product testing, and quality assurance raise production costs, particularly for premium and prescription products.

Additionally, while Japanese consumers value quality, they remain sensitive to price. Brands must carefully balance cost structures with innovation and safety investments. Product recalls or quality controversies can have lasting reputational impacts, making consistency and transparency critical for market success.

Segment Insights

Japan Dog Food Market

The dog food segment remains the largest contributor to Japan’s pet food market. The popularity of toy and small dog breeds—such as toy poodles, chihuahuas, and dachshunds—has significantly shaped product development. These breeds require tailored nutrition, smaller kibble sizes, and specialized formulations that address dental care, digestion, and joint health.

The growing population of senior dogs has further increased demand for age-specific diets focused on mobility, weight management, and organ support. Convenience-oriented packaging, including portion-controlled and easy-serve formats, aligns well with urban lifestyles. Additionally, consumer demand for “natural” ingredients, minimal additives, and transparent sourcing continues to elevate premium dog food categories, enabling sustained growth despite gradual declines in dog ownership.

Japan Cat Food Market

The cat food segment is expanding faster than dog food, driven by urbanization and the growing preference for cats as low-maintenance companions in apartment living. Cats are perceived as more suitable for smaller homes and independent lifestyles, making them increasingly popular among younger professionals and elderly households.

Japanese cat owners are particularly sensitive to taste, texture, and palatability. This has stimulated innovation in flavor varieties and product textures, especially in wet food and treats. Rising adoption rates, combined with higher per-pet expenditure, position the cat food segment as a key engine of market growth.

Japan Dry Dog Food Market

Dry dog food remains a cornerstone of the Japanese market due to its affordability, convenience, and extended shelf life. Modern kibble formulations are increasingly fortified with functional ingredients to support dental health, digestion, and joint mobility. Demand for smaller kibble sizes tailored to small breeds remains strong.

Health-driven innovation has also expanded offerings in grain-free, hypoallergenic, and low-calorie products, responding to rising concerns about obesity and food sensitivities among pets. Although wet and fresh foods are gaining popularity, dry dog food continues to dominate daily feeding routines due to its practicality and nutritional consistency.

Japan Wet Cat Food Market

Wet cat food is among the fastest-growing segments in Japan’s pet food industry. Japanese consumers widely perceive wet food as superior in taste, hydration, and digestibility—factors especially important for fussy eaters and aging cats.

Single-serve cans and pouches dominate this segment, aligning with preferences for freshness and portion control. Premium wet food products emphasizing high meat or fish content, minimal additives, and functional benefits are particularly popular. The increasing focus on urinary health, kidney care, and overall hydration has made wet cat food a central component of feline nutrition in Japan.

Japan Fish Food Market

Japan’s long-standing cultural affinity for ornamental fish—such as koi, goldfish, and tropical species—supports a stable fish food market. Fish are favored as pets due to their low space and maintenance requirements, especially in urban households.

Demand for specialized fish food that enhances coloration, growth, immunity, and water quality continues to grow. High-quality pellets and flakes formulated for koi and other premium species dominate this niche segment. While smaller than dog and cat food markets, fish food maintains consistent demand driven by hobbyists and aquaculture enthusiasts.

Distribution Channel Analysis

Store-Based Retailing

Store-based retailing remains the leading distribution channel for pet food in Japan. Supermarkets, specialty pet stores, and home centers provide nationwide accessibility and offer a wide assortment of trusted brands. Japanese consumers value the ability to inspect products, read labels, and seek expert advice from in-store professionals.

Specialty pet stores play a particularly important role in promoting premium and functional products, often introducing new formulations and educating customers. Private-label and store brands are also gaining traction by offering competitive pricing without compromising quality.

Veterinary Clinics

Veterinary clinics represent a critical niche channel, particularly for prescription and therapeutic pet food. These products are designed to manage specific conditions such as kidney disease, obesity, allergies, and digestive disorders. Given the high level of trust placed in veterinary professionals, recommendations from clinics strongly influence purchasing decisions.

Although this channel accounts for lower overall volume, it generates high margins and plays a key role in the expansion of functional and clinical nutrition categories.

Market Segmentation

By Product Type

Dog Food

Dog Treats and Mixers

Dry Dog Food

Wet Dog Food

Cat Food

Cat Treats and Mixers

Dry Cat Food

Wet Cat Food

Others

Bird Food

Fish Food

Small Mammal/Reptile Food

By Distribution Channel

Store-Based Retailing

E-Commerce

Veterinary Clinics

By Cities

Tokyo

Osaka

Aichi

Kanagawa

Saitama

Hyogo

Chiba

Hokkaido

Fukuoka

Shizuoka

Competitive Landscape

The Japan pet food market features a mix of domestic leaders and global giants, all competing through innovation, quality, and brand trust. Companies are evaluated across five key viewpoints: Overview, Key Personnel, Recent Developments, SWOT Analysis, and Revenue Performance.

Major Companies Covered

Mars Incorporated

Gex Corporation

Royal Canin

Hill’s Pet Nutrition

Unicharm

INABA-PETFOOD Co. Ltd

These companies continue to invest in product development, premium ingredients, advanced manufacturing, and localized formulations tailored to Japanese consumer preferences.

Final Thoughts

The Japan Pet Food Market is entering a dynamic growth phase shaped by premiumization, health awareness, and deep emotional bonds between owners and pets. Despite demographic headwinds and a gradually declining pet population, rising per-pet expenditure, aging companion animals, and strong demand for functional nutrition are driving sustained expansion.

With market value projected to grow from US$ 6.72 billion in 2025 to US$ 14.68 billion by 2034, Japan’s pet food industry stands as a model of quality-driven, innovation-led growth. For manufacturers, retailers, and investors, success will depend on maintaining trust, advancing nutritional science, and continuously adapting to the evolving lifestyles and expectations of Japanese pet owners.

In a society where pets increasingly serve as companions, caregivers, and family members, the future of pet food in Japan will be defined not just by what pets eat—but by how deeply their well-being is woven into everyday life.

About the Creator

Keep reading

More stories from Aaina Oberoi and writers in Petlife and other communities.

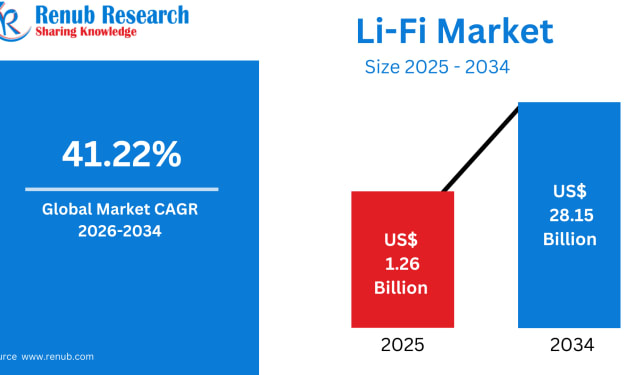

Global Li-Fi Market Size & Forecast 2026–2034

Introduction: Lighting the Next Chapter of Connectivity Wireless communication has become the backbone of the modern digital world. From smartphones and laptops to industrial automation and smart cities, connectivity defines productivity, convenience, and innovation. Yet, traditional radio-frequency (RF) technologies such as Wi-Fi and cellular networks are increasingly constrained by spectrum congestion, interference, security vulnerabilities, and performance bottlenecks.

By Aaina Oberoi4 days ago in Futurism

A Dart at Dusk

Seconds ago, the sullen sun set on the two of us… my exuberant furry companion and me. A fresh breeze embraces us, delivering welcome relief from the day’s oppressive heat. His typical stumbling and staggering along — apace with a sloth — has turned into trip-trapping, high-stepping, almost skipping along.

By Angie the Archivist 📚🪶5 days ago in Petlife

The Day I Realized My Home Might Be Stressing My Pet

For a long time, I thought my home was the safest place my pet could be. It was warm, familiar, filled with love. There were cozy corners for naps, toys scattered across the floor, and a predictable routine that gave us both comfort. I believed I was doing everything right — feeding the best food I could afford, keeping up with vet visits, and making sure my pet never felt alone.

By Inamullah Momand 5 days ago in Petlife

Comments

There are no comments for this story

Be the first to respond and start the conversation.