United States Medical Ceramics Market Size & Forecast (2026–2034)

Market Growth Accelerates on the Back of Advanced Implants, Aging Population, and Biomaterial Innovation

Market Overview

The United States Medical Ceramics Market is witnessing steady and sustained growth, driven by increasing demand for advanced biomaterials across orthopedic, dental, and surgical applications. Medical ceramics—known for their exceptional biocompatibility, corrosion resistance, and mechanical strength—have become essential components in modern healthcare solutions.

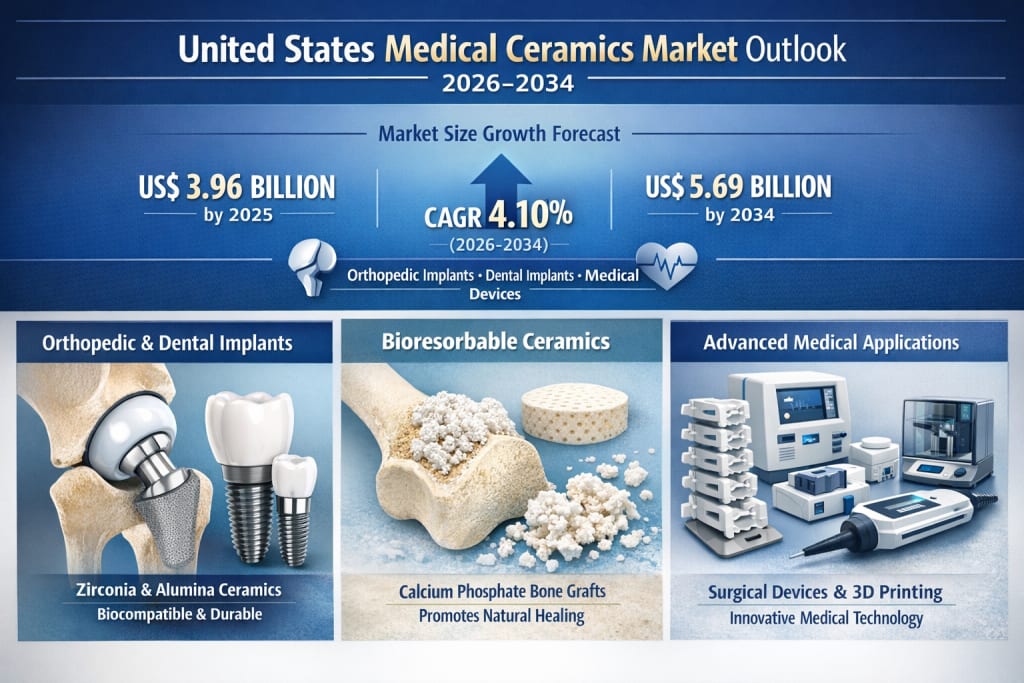

According to Renub Research, the U.S. medical ceramics market size stood at US$ 3.96 Billion in 2025 and is expected to reach US$ 5.69 Billion by 2034, expanding at a compound annual growth rate (CAGR) of 4.10% between 2026 and 2034. The market’s expansion is fueled by technological advancements, rising surgical volumes, an aging population, and increased preference for long-lasting, biologically compatible materials.

Medical ceramics include materials such as alumina, zirconia, calcium phosphate ceramics, and bioactive glass ceramics. These materials are widely used in joint replacements, dental implants, bone grafts, and reconstructive surgeries due to their superior performance compared to conventional metals and polymers.

United States Medical Ceramic Market Outlook

Medical ceramics play a critical role in the U.S. healthcare ecosystem because they provide a rare combination of strength, durability, and biological compatibility. Unlike traditional metallic implants, ceramics demonstrate minimal wear, reduced inflammatory response, and superior resistance to corrosion inside the human body.

The United States benefits from a highly developed healthcare system, strong research infrastructure, and widespread adoption of advanced medical technologies. These factors have positioned the country as a leading consumer and innovator in medical ceramic applications. Increasing incidences of orthopedic disorders, dental complications, and reconstructive surgeries have further strengthened demand for ceramic-based medical solutions.

Additionally, the presence of global medical device manufacturers, strict quality standards, and strong regulatory oversight ensures the continuous improvement and acceptance of medical ceramic products across U.S. hospitals and clinics.

Growth Drivers of the United States Medical Ceramics Market

Rising Demand for Orthopedic and Dental Implants

One of the primary drivers of the U.S. medical ceramics market is the growing number of orthopedic and dental implant procedures. The aging population, coupled with rising cases of arthritis, osteoporosis, joint degeneration, and tooth loss, has led to an increase in hip, knee, and dental implant surgeries.

Ceramics such as alumina and zirconia are widely used in these procedures due to their high wear resistance, smooth surface finish, and excellent compatibility with human tissues. Compared to metal implants, ceramic implants offer lower friction, reduced risk of allergic reactions, and improved long-term outcomes.

According to demographic studies, the U.S. population aged 65 and above is projected to rise significantly over the coming decades, directly contributing to higher demand for joint replacements and dental restorations. As surgical volumes increase, medical ceramics will remain a preferred material choice for implantable devices.

Technological Advancements and Material Innovation

Technological progress has significantly enhanced the performance and application range of medical ceramics in the United States. Innovations in ceramic processing techniques, surface modification, and additive manufacturing have improved mechanical strength, fracture resistance, and osseointegration capabilities.

Research and development efforts in bioactive and bioresorbable ceramics are opening new opportunities in regenerative medicine and tissue engineering. These materials support natural bone regeneration and eliminate the need for secondary surgeries, aligning with the growing demand for minimally invasive and patient-centric treatments.

In February 2025, CeramTec GmbH introduced a new range of lead-free piezoceramics designed for medical sensors and diagnostic devices. This innovation aligns with evolving U.S. and EU regulations on hazardous materials while offering safer solutions for medical applications.

Strong Healthcare Infrastructure and High Technology Adoption

The United States continues to lead globally in healthcare spending and technological adoption. Advanced surgical facilities, high patient awareness, and strong reimbursement frameworks support the widespread use of premium medical materials such as ceramics.

Surgeons increasingly prefer ceramic implants due to their long-term reliability and improved patient outcomes. The presence of major medical device manufacturers and continuous product innovation further accelerates market growth.

In October 2025, Stryker Corporation launched a new portfolio of advanced ceramic orthopedic implants, reinforcing its commitment to innovation and strengthening its competitive position in the U.S. orthopedic market.

Challenges Facing the United States Medical Ceramics Market

High Manufacturing and Material Costs

Despite strong demand, high production costs remain a key challenge. Manufacturing medical-grade ceramics requires sophisticated equipment, controlled environments, and high-purity raw materials such as alumina and zirconia. These factors significantly increase production expenses and can impact the pricing of final medical devices.

Cost pressures are particularly challenging for smaller manufacturers, prompting industry players to focus on process optimization and economies of scale.

Stringent Regulatory and Approval Processes

Medical ceramics used in implants and devices must undergo rigorous testing and approval processes governed by U.S. regulatory authorities. While these regulations ensure patient safety and product efficacy, they can also lead to extended approval timelines and increased development costs.

For emerging companies, navigating complex regulatory requirements can delay product launches and limit market entry opportunities.

United States Bioinert Medical Ceramics Market

Bioinert ceramics such as alumina and zirconia dominate the U.S. medical ceramics market due to their exceptional mechanical strength and long-term stability. These materials do not chemically interact with surrounding tissues, ensuring durability and biocompatibility in weight-bearing applications.

The rising number of hip and knee replacement surgeries continues to drive demand for bioinert ceramics. Strong surgeon acceptance and established clinical success make bioinert materials a cornerstone of orthopedic and dental implant solutions in the United States.

United States Bioresorbable Medical Ceramics Market

Bioresorbable medical ceramics are gaining momentum as healthcare providers seek materials that support natural healing. Calcium phosphate-based ceramics such as hydroxyapatite and tricalcium phosphate are widely used in bone grafts, dental fillers, and tissue engineering applications.

These materials gradually dissolve in the body, promoting bone regeneration without the need for removal surgery. Increasing investment in regenerative medicine and minimally invasive treatments is expected to accelerate growth in this segment over the forecast period.

United States Medical Ceramics in Plastic Surgery

The U.S. remains one of the largest markets for cosmetic and reconstructive surgery, supporting strong demand for medical ceramics in plastic surgery applications. Zirconia and bioactive ceramics are used in facial reconstruction, dental aesthetics, and craniofacial procedures due to their natural appearance and biocompatibility.

Rising consumer acceptance of aesthetic procedures and advancements in ceramic materials are expected to further expand this segment.

United States Orthopedic Medical Ceramics Market

Orthopedic applications represent the largest share of the U.S. medical ceramics market. Ceramic-on-ceramic and ceramic-on-polymer implants offer superior wear resistance, reduced failure rates, and extended implant lifespan compared to traditional materials.

An aging population and increasing prevalence of joint disorders ensure sustained demand for orthopedic medical ceramics throughout the forecast period.

Regional Market Insights

California Medical Ceramics Market

California leads the U.S. medical ceramics market due to its advanced healthcare infrastructure, strong research institutions, and high adoption of innovative medical technologies. The state’s prominence in orthopedic, dental, and cosmetic procedures continues to drive demand for ceramic-based solutions.

Texas Medical Ceramics Market

Texas is experiencing steady growth fueled by its large population base, expanding healthcare facilities, and rising demand for orthopedic and dental treatments. Investments in healthcare infrastructure and cost-effective medical services support long-term market expansion.

New York Medical Ceramics Market

New York’s well-developed healthcare system and high concentration of specialty hospitals contribute to strong demand for medical ceramics. An aging population and high healthcare expenditure make the state a key regional market.

Market Segmentation

By Material Type:

Bioinert

Bioactive

Bioresorbable

Piezo Ceramics

By Application:

Surgical Instruments

Plastic Surgery

Orthopedic

Dental

By Key States:

California, Texas, New York, Florida, Illinois, Pennsylvania, Ohio, Georgia, New Jersey, Washington, North Carolina, Massachusetts, Virginia, Michigan, Maryland, Colorado, Tennessee, Indiana, Arizona, Minnesota, Wisconsin, Missouri, Connecticut, South Carolina, Oregon, Louisiana, Alabama, Kentucky, Rest of United States

Competitive Landscape

Key players are analyzed across overview, leadership, recent developments, product portfolios, and financial performance.

CeramTec GmbH

Kyocera Corporation

Morgan Advanced Materials

3M

DSM

NGK Spark Plug Co. Ltd

DePuy Synthes

Zimmer Biomet Holding Inc

Straumann

BioMérieux SA

Final Thoughts

The United States Medical Ceramics Market is positioned for steady growth through 2034, supported by technological innovation, rising surgical volumes, and a growing aging population. While high production costs and regulatory challenges persist, ongoing advancements in ceramic materials and expanding applications across orthopedics, dentistry, and plastic surgery will continue to shape market evolution.

As healthcare providers increasingly prioritize long-term performance, patient safety, and biocompatibility, medical ceramics will remain a vital component of the U.S. medical device landscape.

About the Creator

Day 4 of Quitting

If this is how sobriety feels, maybe it’s better to go through life a little buzzed… this, along with other hits like, I want to kill myself, I wish I was dead, and I’m going to throw myself off a bridge have been the only thoughts on rotation these past few days. I promise myself that if, in a month, I still feel like this (‘this’ meaning despondent, full of rage, and simultaneously numb) I can go back to smoking. Until mid-February though? Nicotine is off the table.

By sleepy drafts27 days ago in Longevity

The Place That Stayed With Me: After a Treacherous Route Through Open Desert, at Mina Mina I Saw Holiness

A journey across silence, struggle, and spirit in the heart of the Australian desert Some places do not announce themselves with signs or grand entrances. They wait quietly, asking something of you before they reveal what they are. Mina Mina was one of those places.

By Fiaz Ahmed 4 days ago in Longevity

Comments

There are no comments for this story

Be the first to respond and start the conversation.