Legacy vs Innovation: How the German Automotive Industry is Pivoting in the Age of EVs

Germany stands as the undisputed heart of European vehicle manufacturing. The Germany automotive industry commands global attention due to its engineering excellence, massive production capabilities, and brand heritage.

Key Takeaways

- The Germany automotive market is projected to expand at a steady 3.5% annual rate to reach nearly 2 million units by 2033.

- Domestic manufacturers export roughly 76% of all vehicles produced, which creates a heavy reliance on international economic health.

- Electric vehicle production is forecast to rebound sharply in 2025 as strict EU emission targets force automakers to ramp up sales.

- High energy prices and emerging Chinese competitors currently pose the most significant threats to the profitability of legacy German brands.

- Government policy aims to have 15 million electric vehicles in operation by 2030 to accelerate the transition away from combustion engines.

Germany stands as the undisputed heart of European vehicle manufacturing. The Germany automotive market commands global attention due to its engineering excellence, massive production capabilities, and brand heritage. However, the industry currently faces a pivotal moment of transformation. According to the latest data from the IMARC Group, the market size reached 1,443.5 Thousand Units in 2024. This figure represents more than just sales; it signifies a baseline for a sector actively redefining itself amidst electrification, digitalization, and geopolitical shifts.

Investors, stakeholders, and enthusiasts often ask where this industrial titan is heading. The answers lie deep in the data. While recent years introduced volatility through supply chain shocks, the long-term outlook remains positive. We analyzed government reports, VDA statistics, and market intelligence to provide a clear view of the road ahead. This comprehensive guide explores the forecasts, challenges, and opportunities shaping the future of German mobility.

How big is the German Automotive Market today?

The market volume currently stands at 1,443.5 Thousand Units, marking 2024 as a critical stabilization year.

Following the disruptions of the global pandemic and subsequent supply chain crises, the German automotive sector focused intensely on recovery. In 2024, production lines smoothed out, and semiconductor shortages eased significantly. Consequently, manufacturers could finally clear their order backlogs. The VDA (Verband der Automobilindustrie) reported domestic production reaching approximately 4.15 million passenger cars. However, domestic sales figures reflect a cautious consumer base. High inflation and general economic uncertainty curbed immediate spending power for many households.

Despite these headwinds, the baseline volume of over 1.4 million units proves the market’s resilience. This solid foundation provides the necessary stability for the anticipated growth over the next decade. Furthermore, this volume highlights the separation between mass-market stagnation and the continued booming demand for the premium luxury segment, where German brands like Porsche, BMW, and Mercedes-Benz continue to excel.

Request the full research report with the list of TOC

What is the projected growth rate through 2033?

Experts forecast the market to grow at a Compound Annual Growth Rate (CAGR) of 3.5% between 2025 and 2033.

Stability defines this growth trajectory rather than explosive expansion. The IMARC Group predicts the market will reach 1,967.3 Thousand Units by 2033. For investors, a 3.5% CAGR suggests a mature, steady climb. This growth relies heavily on the successful transition from Internal Combustion Engines (ICE) to electric mobility. Additionally, the replacement cycle for aging commercial fleets will drive consistent demand.

We must also consider the context of this growth. Unlike emerging markets that might see double-digit growth, Germany is a saturated, replacement-driven market. Therefore, growth comes not just from selling more cars, but from selling higher value cars embedded with advanced software and connectivity features. Investors should view this forecast as a signal of long-term health. The German market prioritizes sustainable value over short-term gains, aligning perfectly with broader European Union economic goals.

Visual Data Analysis: Production vs. Export

How much of Germany’s automotive output actually stays within its borders? The data reveals a heavy reliance on international trade.

The following table compares domestic production against export volumes for the 2024 fiscal period. This comparison is vital for understanding the industry's risk exposure.

Key Takeaway: Germany builds for the world. With nearly three-quarters of all cars produced leaving the country, the health of the Germany automotive market depends heavily on global economic stability. Consequently, trade tariffs, international logistics, and the economic health of key partners like China and the USA play a massive role in sector profitability. If global demand slows, German factories feel the impact immediately.

Why is the Electric Vehicle (EV) sector fluctuating?

The sudden removal of government subsidies in late 2023 caused a temporary slump, yet strict regulations necessitate a rapid rebound.

The numbers tell a stark story regarding e-mobility adoption. In 2024, the market share of Battery Electric Vehicles (BEVs) dropped to 13.5%, down from 18.4% the previous year. Consumers reacted negatively to the sudden price hike caused by the subsidy cuts. Additionally, high electricity prices in Germany made the "Total Cost of Ownership" argument for EVs less compelling for the average driver.

However, this decline is likely temporary. The VDA forecasts a massive 75% increase in BEV production for 2025. Why such a sharp turnaround? New, stricter EU fleet emission targets kick in this year. Manufacturers must sell more EVs to avoid hefty fines. Therefore, we expect aggressive pricing strategies, attractive leasing deals, and new model launches to revitalize this segment immediately. The industry is currently in a "valley of death" between early adopters and the mass market, but the regulatory push ensures they will cross it.

Which market segments are dominating the industry?

Passenger cars continue to lead in volume, but commercial vehicles are seeing rapid technological integration.

We can analyze the IMARC segmentation to understand the market composition better:

Vehicle Type: Passenger cars hold the lion's share of the market. However, the commercial vehicle segment is expanding due to logistics demands. The rise of e-commerce delivery fleets requires robust, reliable vans, many of which are now electrifying to meet urban "Low Emission Zone" requirements.

Propulsion Type: Internal Combustion Engines (ICE) still dominate the current road fleet. Nevertheless, the Hybrid and Electric Vehicle (EV) segments are capturing nearly all new investment capital. Diesel, once the backbone of German auto sales, continues its slow decline in market share.

End Use: The commercial sector is aggressively upgrading fleets to meet green standards. Corporate fleet managers prioritize TCO (Total Cost of Ownership), driving a shift toward electric options. Conversely, personal buyers are holding onto older vehicles longer, often awaiting more affordable EV options in the €25,000 range.

What are the primary drivers propelling market expansion?

Government mandates and the "Industry 4.0" revolution drive the current market momentum.

The German government set an ambitious target of putting 15 million electric vehicles on the road by 2030. This policy acts as the primary catalyst for growth, forcing infrastructure development. Additionally, the push for autonomous driving technology fuels innovation. Modern vehicles are no longer just machines; they are data centers on wheels.

Connectivity features and advanced driver-assistance systems (ADAS) attract younger buyers who view the car as an extension of their smartphone. Furthermore, substantial investments in charging infrastructure aim to remove "range anxiety." The expansion of the Deutschlandnetz (Germany Network) of fast-charging stations makes EV ownership viable for the average citizen, not just homeowners with private garages.

What challenges are hindering rapid growth?

High energy costs and fierce competition from Asian manufacturers pose significant threats to local producers.

German manufacturers face a "perfect storm" of economic pressure. Domestic energy prices remain high compared to the US or China, significantly increasing production costs for energy-intensive processes like steel and glass manufacturing. Simultaneously, Chinese OEMs (Original Equipment Manufacturers) like BYD, MG, and Nio are entering the European market.

These competitors offer high-tech electric vehicles at prices legacy German brands struggle to match. Moreover, a shortage of skilled labor complicates the shift to software-defined manufacturing. Germany needs more software engineers, not just mechanical engineers. To survive, German brands must leverage their reputation for quality, safety, and data security while drastically reducing overhead costs.

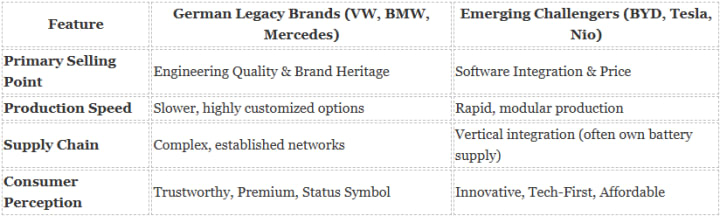

Comparison Chart: German Legacy vs. Emerging Competitors

How do traditional German brands stack up against new market challengers? The landscape has shifted from a hardware battle to a software battle.

Conclusion & Future Outlook

The Germany automotive market is navigating a complex but promising path.

The data confirms a steady trajectory. Starting from a base of 1,443.5 Thousand Units in 2024, the market moves toward a 2033 target of 1,967.3 Thousand Units. A CAGR of 3.5% ensures sustainable expansion. The transition to e-mobility is non-negotiable. While the "ICE vs. EV" battle creates short-term friction, the long-term trend points undeniably toward a digitized, electrified future.

For investors, the opportunities lie in the supply chain—batteries, software, and charging infrastructure—rather than just traditional vehicle assembly. German engineering must now prove it can master code as well as it mastered the combustion engine.

Frequently Asked Questions

Is the German automotive market growing?

Yes, the market is growing. Experts forecast a Compound Annual Growth Rate (CAGR) of 3.5% from 2025 to 2033, indicating steady recovery and expansion.

Who are the top automotive manufacturers in Germany?

The "Big Three" continue to dominate: Volkswagen Group (including Audi and Porsche), BMW Group, and Mercedes-Benz Group. Opel and Ford Germany also maintain significant manufacturing footprints.

What is the forecast for German car market size in 2033?

According to IMARC Group data, the market is expected to reach approximately 1,967.3 Thousand Units by 2033, driven by fleet renewals and EV adoption.

Why did EV sales drop in Germany in 2024?

Sales dropped primarily due to the sudden removal of government purchase subsidies (Umweltbonus) in late 2023. This increased the effective cost for consumers, causing a temporary hesitation in the market.

What is the export ratio of German cars?

Germany exports approximately 76% of its domestic car production. This makes the industry highly sensitive to global economic trends and international trade policies.

About the Creator

Joey Moore

I'm Joey Moore, a seasoned Research Analyst with 5+ years of experience in market research. Expert in data analysis, strategic planning, and industry insights. Proven track record in delivering actionable reports.

Keep reading

More stories from Joey Moore and writers in Journal and other communities.

Why the Europe Used Car Market is Growing Faster Than New Car Sales in 2026-2034

Key Takeaways The European used car market is currently valued at 65.1 billion USD and is projected to grow steadily to 93.8 billion USD by 2034. Used electric vehicle sales jumped by 57 percent in late 2024 due to price corrections and improved consumer trust in battery longevity. An aging fleet average of 12.3 years combined with economic inflation is pushing more buyers toward the secondary market for affordable mobility. Consumers are increasingly shifting from risky private sales in favor of organized dealerships that offer certified pre-owned protection and warranties. Future market growth will be driven by the rising dominance of SUVs and the expansion of digital retail platforms for online vehicle purchasing.

By Joey Mooreabout 6 hours ago in Journal

Comments

There are no comments for this story

Be the first to respond and start the conversation.