Japan Personal Computer Market Size & Forecast 2025–2033

From Mobile-First Culture to High-Performance Computing: Japan’s PC Market Enters a New Growth Phase

Japan Personal Computer Market Overview

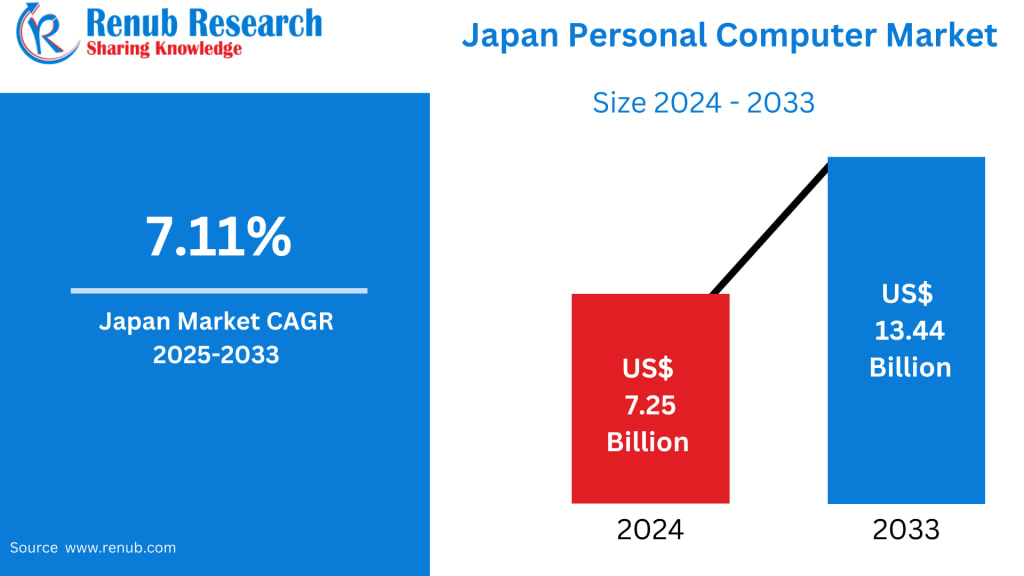

Japan’s personal computer market is entering a renewed phase of expansion, supported by evolving work habits, digital education programs, and increasing demand for high-performance computing. According to Renub Research, the Japan Personal Computer Market is projected to grow from US$ 7.25 billion in 2024 to US$ 13.44 billion by 2033, registering a Compound Annual Growth Rate (CAGR) of 7.11% during 2025–2033.

Historically, Japan has been a mobile-first nation, with smartphones and tablets dominating everyday digital interactions. However, the post-pandemic era has reinforced the importance of full-scale computing devices capable of handling productivity software, enterprise security requirements, content creation, and advanced gaming. As a result, PCs—especially laptops and hybrid devices—are reclaiming relevance across consumer, education, and enterprise segments.

In addition, the convergence of cloud computing, AI-driven applications, and cybersecurity compliance is pushing individuals and organizations to upgrade their computing infrastructure. These dynamics are transforming the PC market from a replacement-driven industry into a growth-oriented ecosystem.

Japan Laptops / Notebooks Market

Laptops and notebooks remain the backbone of Japan’s personal computer industry. Compact living spaces, heavy reliance on public transportation, and a preference for lightweight electronics make portable PCs the preferred choice for Japanese consumers.

Ultrabooks, 2-in-1 convertibles, and slim notebooks with extended battery life are particularly popular among professionals and university students. Devices offering stylus compatibility and detachable keyboards are increasingly viewed as full replacements for traditional desktops. Chromebooks and cost-effective notebooks have also gained traction through government-backed education initiatives, most notably the GIGA School Program, which aims to provide every student with a digital learning device.

At the premium end, high-specification laptops equipped with powerful GPUs attract creative professionals, software developers, and gamers. This diverse demand ensures that notebooks will continue to dominate PC shipments in Japan throughout the forecast period.

Japan Large Enterprise Personal Computer Market

Large enterprises across Japan—including manufacturing conglomerates, financial institutions, and technology firms—represent a stable and recurring source of PC demand. These organizations typically follow structured device refresh cycles to maintain productivity, ensure cybersecurity compliance, and support enterprise software ecosystems.

With hybrid work now firmly established, enterprises are prioritizing secure notebooks with advanced endpoint protection, biometric authentication, and seamless cloud integration. Device-as-a-Service (DaaS) models and managed IT offerings are gaining popularity, allowing companies to outsource hardware lifecycle management while maintaining operational flexibility.

This enterprise-driven consistency helps stabilize the overall PC market, even during periods of consumer demand fluctuation.

Japan ARM-Based Personal Computer Market

ARM-based PCs are gradually carving out a meaningful position in Japan’s computing landscape. Apple’s MacBook lineup has played a central role in popularizing ARM architecture, thanks to its combination of high performance, long battery life, instant-on capability, and tight ecosystem integration.

Software optimization for ARM processors continues to improve, expanding compatibility across productivity, creative, and business applications. As Japanese enterprises pursue sustainability goals and mobile-first workflows, ARM-based systems are increasingly viewed as energy-efficient and future-ready alternatives to traditional x86 PCs.

Although still a niche compared to Windows-based systems, ARM PCs are expected to gain steady market share over the coming decade.

Japan Mid-Range Personal Computer Market

Mid-range personal computers form the foundation of Japan’s consumer and education markets. These systems deliver sufficient performance for remote learning, office productivity, multimedia consumption, and casual gaming—while remaining accessible to price-sensitive buyers.

Manufacturers in this segment focus on delivering SSD storage, efficient processors, slim designs, and reliable battery life without significantly increasing prices. Seasonal promotions, retail discounts, and bundled software offerings further enhance demand.

The mid-range segment acts as a stabilizing force for the overall market, ensuring consistent volumes even during economic uncertainty.

Japan Personal Computer Offline Retail and VARs Market

Despite the rise of e-commerce, offline retail continues to play a vital role in Japan’s PC sales ecosystem. Japanese consumers often prefer hands-on evaluation before purchasing, especially when comparing displays, keyboards, and build quality.

Large electronics retailers remain influential, while value-added resellers (VARs) serve small and medium-sized businesses, government bodies, and educational institutions. VARs differentiate themselves by offering bundled services such as installation, training, system integration, and after-sales support.

Back-to-school seasons, fiscal year-end budgets, and holiday promotions consistently drive foot traffic and offline sales.

Japan Windows Personal Computer Market

Windows PCs continue to dominate Japan’s personal computer market, particularly in enterprise, government, and education sectors. Legacy software dependencies, enterprise applications, and widespread IT familiarity ensure the continued relevance of the Windows ecosystem.

For gamers, Windows remains the preferred platform due to its extensive game library and hardware customization options. Meanwhile, affordable Windows laptops serve as entry-level solutions for households and students.

Strong partnerships between Microsoft and hardware vendors ensure a broad portfolio of devices across all price bands, reinforcing Windows’ leadership position.

Regional Market Insights

Tokyo Personal Computer Market

Tokyo stands as Japan’s largest PC market, driven by its concentration of corporate headquarters, financial institutions, government ministries, and creative industries. Demand spans secure enterprise notebooks, high-performance workstations, and lightweight consumer laptops suited for commuting professionals.

Aichi Personal Computer Market

Aichi’s economy, anchored by automotive and industrial manufacturing, fuels strong enterprise demand for robust PCs used in engineering, design, and supply chain management. VARs play a critical role in supporting enterprise IT integration.

Shizuoka Personal Computer Market

Shizuoka’s PC demand is shaped by SMEs, educational institutions, and households. The GIGA School Program sustains notebook sales, while families favor mid-range laptops for shared home use.

Market Segmentation

By Form Factor

Laptops / Notebooks

Desktop Towers and SFF

All-in-One PCs

Tablets / Detachables

By End User

Consumer

Small & Medium Business

Large Enterprise

Government & Education

By Processor Architecture

x86 (Intel–AMD)

ARM-based

RISC-V & Others

By Price Band

Entry-Level (< USD 600)

Mid-Range (USD 600–1200)

Premium / Gaming (> USD 1200)

By Distribution Channel

Offline Retail and VARs

E-commerce and Direct-to-Consumer

By Operating System

Windows

macOS

ChromeOS

Linux Distributions

Top Cities Covered

Tokyo, Kansai, Aichi, Kanagawa, Saitama, Hyogo, Chiba, Hokkaido, Fukuoka, Shizuoka

Key Players Analysis

The competitive landscape of Japan’s PC market includes global and regional technology leaders. Each company has been evaluated across five viewpoints: Overview, Key Person, Recent Developments, SWOT Analysis, and Revenue Analysis.

Lenovo Group Limited

HP Inc.

Dell Technologies Inc.

Apple Inc.

Acer Incorporated

Microsoft Corporation

Samsung Electronics Co., Ltd.

Huawei Technologies Co., Ltd.

Xiaomi Corporation

LG Electronics Inc.

Competition centers on innovation, ecosystem integration, pricing strategies, and service offerings, with vendors increasingly differentiating through sustainability and AI-enabled features.

Final Thoughts

Japan’s personal computer market is no longer defined solely by replacement demand. The combination of hybrid work, digital education, enterprise modernization, and energy-efficient computing is reshaping the industry’s trajectory.

With Renub Research forecasting growth from US$ 7.25 billion in 2024 to US$ 13.44 billion by 2033, PCs are reaffirming their role as essential productivity tools in Japan’s digital economy. Vendors that successfully balance mobility, performance, security, and sustainability will be best positioned to capture long-term value in this evolving market.

About the Creator

jaiklin Fanandish

Jaiklin Fanandish, a passionate storyteller with 10 years of experience, crafts engaging narratives that blend creativity, emotion, and imagination to inspire and connect with readers worldwide.

Keep reading

More stories from jaiklin Fanandish and writers in Futurism and other communities.

United States Digital Payment Market Size & Forecast 2025–2033

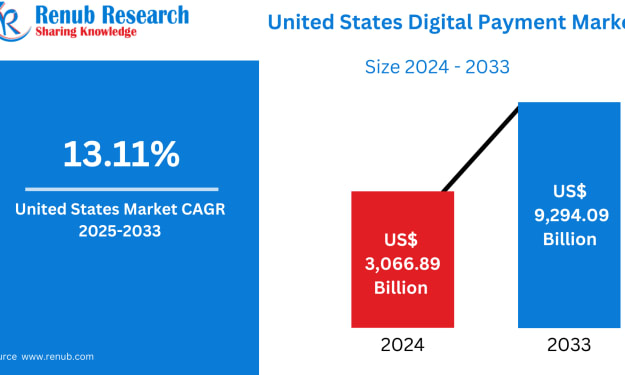

United States Digital Payment Market Overview The United States Digital Payment Market is entering a phase of remarkable acceleration as consumers, businesses, and institutions increasingly move away from cash-based transactions. According to Renub Research, the market is projected to expand dramatically from US$ 3,066.89 billion in 2024 to US$ 9,294.09 billion by 2033, registering a robust Compound Annual Growth Rate (CAGR) of 13.11% between 2025 and 2033.

By jaiklin Fanandish4 days ago in Futurism

About Binding Prometheus

I want to start actively advocating on behalf of my own work, and the most valuable part of my canon is, without a doubt, Binding Prometheus, the play I have been working on since 2019 and only finished in 2023 as part of my MA. The play itself is an amalgamation of a million different inspirations. On one end, it evokes the Ancient Greek myth-play, deriving its own title from the earliest extant work of Western drama we have, Aeschylus’s Prometheus Bound. On the other end, it borrows significantly from the sci-fi bulwarks from over the years, namely Mary Shelley’s Frankenstein and Karel Capek’s Rossum’s Universal Robots. The play could be an episode of Black Mirror, I fear. I don’t know. I’ve only ever seen one episode of Black Mirror.

By Steven Christopher McKnight10 days ago in Futurism

United States Dishwasher Market Size & Forecast 2025–2033

United States Dishwasher Market Overview The United States Dishwasher Market is poised for steady expansion over the next decade, reflecting the country’s growing reliance on modern, time-saving home appliances. According to Renub Research, the U.S. dishwasher industry is expected to grow from US$ 10.71 billion in 2024 to US$ 13.05 billion by 2033, registering a Compound Annual Growth Rate (CAGR) of 2.22% from 2025 to 2033.

By Aaina Oberoi4 days ago in Futurism

Comments

There are no comments for this story

Be the first to respond and start the conversation.