United States Hotel Market Size & Forecast 2025–2033: Experience-Driven Travel Fuels a New Era of Growth

From domestic leisure booms to tech-enabled guest journeys, the U.S. hotel industry is redefining hospitality in a post-pandemic economy

United States Hotel Market Outlook

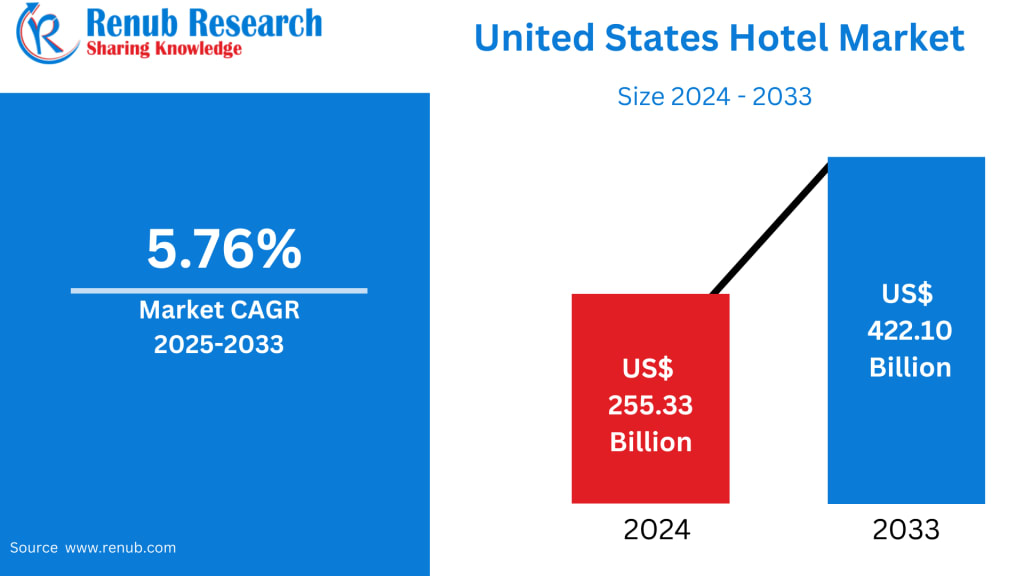

The United States hotel market is poised for steady and resilient expansion, rising from US$ 255.33 billion in 2024 to US$ 422.10 billion by 2033, reflecting a compound annual growth rate (CAGR) of 5.76% during 2025–2033. Growth is being driven by strong domestic travel demand, rising interest in experience-based stays, continued investment in hotel development, and the digital transformation of guest services. As leisure and business travel stabilize across the country, hotels of all categories—from luxury resorts to economy motels—are benefiting from shifting traveler preferences and renewed mobility.

A hotel is any facility that provides short-term or extended lodging along with a variety of hospitality services. These include private rooms, housekeeping, front-desk services, food and beverage operations, fitness centers, event spaces, and recreational amenities. The U.S. hotel ecosystem spans luxury resorts, upscale urban properties, boutique hotels, extended-stay suites, franchised brands, and budget accommodations. Collectively, they form a critical part of the nation’s tourism infrastructure and business travel economy.

Hotels remain deeply embedded in American travel culture. Millions of residents travel domestically for leisure, work, holidays, and road trips, creating sustained demand across metropolitan cities, coastal destinations, national parks, and entertainment hubs. International tourism further supplements occupancy in gateway markets. Emerging trends such as weekend getaways, wellness retreats, remote work travel, and experience-oriented stays continue to elevate the relevance of hotels in everyday lifestyle choices. With improved technology, loyalty programs, and diversified offerings, hotels are better positioned than ever to capture both volume and value from a broad traveler base.

Growth Drivers in the United States Hotel Market

Recovery and Expansion of Domestic Leisure Travel

Domestic leisure travel has become a primary growth engine for the U.S. hotel sector. Travelers increasingly favor short breaks, regional road trips, nature tourism, and city escapes, redistributing demand beyond traditional hubs. Secondary cities, national parks, coastal towns, and resort destinations have experienced rising occupancy, particularly during shoulder seasons.

Experience-driven tourism is reshaping the hotel value proposition. Travelers are now seeking more than accommodation—they want curated local experiences, wellness programs, outdoor activities, and cultural immersion. Hotels are responding by offering tailored packages, partnerships with local operators, upgraded on-site dining, and activity-based itineraries. This shift not only boosts room demand but also strengthens ancillary revenue streams.

Importantly, reliance on domestic travel makes the industry more resilient to global disruptions. A notable development came in October 2025, when Brand USA launched its most ambitious tourism campaign to date, America the Beautiful, during its Travel Week in the UK & Europe. The initiative aims to elevate the country’s global tourism profile while reinforcing long-term visitor demand.

Corporate and Group Travel Rebound

Business travel, conferences, trade shows, and corporate meetings remain vital contributors to hotel revenues. As organizations return to in-person collaboration, weekday occupancy and group bookings are recovering across urban centers, convention destinations, airport corridors, and suburban business hubs.

Corporate travelers generate higher average daily rates (ADR) and contribute significantly to food and beverage, meeting space, and premium services. Hotels are upgrading audiovisual capabilities, high-bandwidth connectivity, and flexible meeting environments to support hybrid events and remote participation.

In October 2025, host agency Fora Travel launched a specialized group travel division to serve corporate off-sites, incentive programs, destination events, and meetings, reflecting rising demand for structured business and group travel solutions. This rebound in corporate activity strengthens RevPAR (revenue per available room) and stabilizes year-round hotel demand.

Technology, Distribution, and Loyalty Optimization

Digital transformation is redefining hotel operations and guest engagement. Mobile check-in, digital room keys, in-room automation, AI-driven personalization, and CRM platforms are enhancing both convenience and profitability. Revenue management systems now enable real-time pricing optimization and smarter channel distribution, helping hotels shift inventory toward higher-margin bookings.

Loyalty programs and direct-booking strategies are increasingly central to profitability. Hotels offer member-only discounts, free upgrades, bonus points, and exclusive perks to reduce reliance on third-party platforms. According to the American Hotel & Lodging Association (AHLA), 2024 recorded 33 strategic alliances across technology, sustainability, media, and guest experience. One notable partnership with DIRECTV HOSPITALITY expanded customized in-room entertainment solutions for properties of all sizes, reinforcing the role of technology in modern hospitality.

Challenges in the United States Hotel Market

Labor Shortages and Rising Wage Pressures

The hospitality sector remains highly labor-intensive, making workforce shortages one of the industry’s most persistent challenges. Hotels depend on staff across housekeeping, food service, maintenance, front desk operations, and event management. Recruiting and retaining employees has become increasingly difficult, driving higher wages, expanded benefits, overtime reliance, and temporary staffing costs.

Labor constraints can limit service quality, slow room turnover, reduce restaurant hours, and affect overall guest satisfaction. To mitigate these pressures, hotels are investing in automation such as self-service kiosks, mobile room controls, and housekeeping productivity tools. However, technology cannot fully replace human interaction—especially in premium service segments—forcing operators to carefully balance cost control with guest experience.

Inflation and Operating Cost Pressures

Rising costs continue to challenge hotel margins. Utilities, food and beverage inputs, linens, cleaning supplies, maintenance materials, and insurance premiums have all increased. At the same time, capital expenditures for renovations, health standards, sustainability upgrades, and digital infrastructure place additional strain on budgets.

While selective price increases can offset some expenses, aggressive rate hikes risk demand erosion in price-sensitive segments. Independent hotels and smaller owner-operators are particularly vulnerable due to limited purchasing power and economies of scale. As a result, operators are prioritizing energy efficiency, procurement optimization, and supplier renegotiation while using sophisticated revenue management to protect occupancy and profitability.

Segment Analysis of the United States Hotel Market

Luxury Hotel Market

The U.S. luxury hotel segment caters to affluent, experience-driven travelers who prioritize premium service, exclusivity, and personalization. These properties include landmark urban hotels, high-end resorts, and boutique luxury brands that command premium rates through concierge services, fine dining, wellness programs, and curated excursions.

Although operational costs are high, luxury hotels demonstrate resilience during economic fluctuations due to lower price sensitivity among their clientele. Gateway cities such as New York, Los Angeles, Miami, and elite resort destinations like Aspen, Napa Valley, and Palm Beach anchor this segment. Sustainability, art-driven design, and private membership models further differentiate offerings and strengthen brand loyalty.

Upper Midscale Hotel Market

Upper midscale hotels form a vital backbone of the U.S. lodging industry. Positioned between economy and upscale segments, they offer comfort, consistency, and essential amenities at accessible price points. Complimentary breakfast, fitness centers, reliable Wi-Fi, and limited meeting spaces make them appealing to families, moderate-budget business travelers, and group bookings.

These properties thrive in suburban areas, highway corridors, and secondary cities, benefiting from steady leisure and corporate demand. Their operational efficiency and standardized brand models make them attractive to franchise investors seeking stable returns with manageable capital expenditure.

Direct Booking Market

Direct bookings—made through hotel websites, mobile apps, or reservation centers—are a strategic priority for U.S. operators. By bypassing third-party commissions, hotels increase net revenue per booking while gaining valuable guest data for personalization and remarketing.

Hotels invest heavily in user-friendly digital platforms, loyalty incentives, targeted promotions, and CRM integration to grow direct traffic. While OTAs remain important for demand generation, increasing the share of direct bookings enhances long-term customer lifetime value and strengthens margin control.

Online Travel Agencies (OTAs)

OTAs continue to play a significant role in customer acquisition, especially among leisure travelers, international guests, and last-minute bookers. Their extensive reach and marketing capabilities deliver high visibility, but commission structures compress hotel margins.

Most operators adopt hybrid strategies—leveraging OTAs for demand while steering repeat guests toward direct channels. Advanced channel management systems help optimize exposure, promotional placement, and inventory distribution to balance occupancy with profitability.

Franchised Hotels

Franchised properties dominate much of the U.S. lodging landscape, enabling local owners to operate under established brands with proven systems, reservation platforms, and loyalty programs. Franchising reduces marketing risk, ensures standardized quality, and supports rapid network expansion.

While franchise fees and compliance costs can impact margins, the model remains attractive due to brand recognition, economies of scale, and operational support. Upper midscale, midscale, and limited-service categories are particularly franchise-heavy.

Owner-Operated Hotels

Independently owned hotels contribute diversity and authenticity to the hospitality sector. These properties range from boutique inns and heritage hotels to roadside motels and resort cottages. Personalized service, local culinary experiences, and community engagement allow independents to compete effectively in niche markets.

Challenges include limited marketing reach, lower purchasing power, and technology gaps. Many owner-operators partner with soft brands, consortia, or third-party platforms to gain distribution support while maintaining operational independence.

Business Traveler Segment

Business travelers represent a high-value customer group, favoring hotels near corporate centers, airports, and convention venues. Key expectations include high-speed internet, functional workspaces, loyalty rewards, and efficient service.

Although corporate travel rebounded unevenly, demand for meetings, incentives, conferences, and exhibitions (MICE) is steadily restoring weekday occupancy. Hotels catering to this segment invest in flexible meeting spaces, co-working zones, and day-use offerings to adapt to hybrid work patterns.

Regional Market Highlights

California

California hosts one of the nation’s most diverse hotel markets, spanning luxury coastal resorts, tech-driven urban hubs, entertainment destinations, and nature-based tourism. Silicon Valley, Los Angeles, San Francisco, Anaheim, and Napa Valley anchor year-round demand. In a strategic move, Visit California partnered with United Airlines in a multi-year marketing initiative to boost the state’s visibility as The Ultimate Playground, driving high-value travel across the region.

New York

New York remains a global hospitality powerhouse, with premium ADRs driven by international tourism, business travel, culture, and events. Manhattan’s luxury hotels, boutique properties, and large convention venues sustain year-round occupancy. High operating costs and real estate constraints have not deterred investment, as the city’s unmatched global appeal continues to attract travelers and capital.

New Jersey

New Jersey’s market blends corporate travel, airport demand, leisure tourism, and group business. Proximity to New York City, seasonal Jersey Shore tourism, pharmaceutical and logistics industries, and Atlantic City’s convention and gaming sector shape demand patterns. Upper midscale and midscale properties dominate, balancing seasonal leisure spikes with stable corporate occupancy.

United States Hotel Market Segmentation

By Volume:

Number of Hotels

Number of Rooms Available

By Chain Scale:

Luxury

Upscale

Upper Midscale

Midscale

Economy

Independent

By Distribution Channel:

Direct Booking (Brand.com)

Online Travel Agencies (OTAs)

Global Distribution Systems (GDS)

Wholesale / Meta-Search / Others

By Ownership & Management Model:

Franchised

Managed

Owner-Operated

Lease

By End-User:

Leisure Travelers

Business Travelers

Group & MICE

Bleisure Travelers

Long-Term Residential Guests

By State:

California, Texas, New York, Florida, Illinois, Pennsylvania, Ohio, Georgia, New Jersey, Washington, North Carolina, Massachusetts, Virginia, Michigan, Maryland, Colorado, Tennessee, Indiana, Arizona, Minnesota, Wisconsin, Missouri, Connecticut, South Carolina, Oregon, Louisiana, Alabama, Kentucky, Rest of the United States

Company Analysis

Leading players shaping the U.S. hotel landscape include:

Marriott International

Hilton Worldwide Holdings

Wyndham Hotels & Resorts

InterContinental Hotels Group (IHG)

Choice Hotels International

Hyatt Hotels Corporation

Best Western Hotels & Resorts

G6 Hospitality (Motel 6 / Studio 6)

Extended Stay America

Red Roof

Each company is evaluated across four dimensions: overview, key leadership, recent developments, and revenue analysis, highlighting competitive strategies and market positioning.

Final Thoughts

The United States hotel market is entering a new phase of stable, experience-driven growth. With revenues forecast to rise from US$ 255.33 billion in 2024 to US$ 422.10 billion by 2033, the industry is benefiting from robust domestic travel, rebounding corporate demand, digital transformation, and diversified accommodation models.

While labor shortages, inflation, and rising operating costs present ongoing challenges, hotels that invest in technology, loyalty programs, sustainability, and differentiated guest experiences are well-positioned to thrive. As travel continues to evolve from a necessity into a lifestyle choice, the U.S. hotel sector stands as a resilient cornerstone of the nation’s tourism economy—adapting, innovating, and welcoming the future one guest at a time.

About the Creator

Marthan Sir

Educator with 30+ years of teaching experience | Passionate about sharing knowledge, life lessons & insights | Writing to inspire, inform, and empower readers.

Keep reading

More stories from Marthan Sir and writers in Filthy and other communities.

Japan Laundry Appliances Market Size and Forecast 2025–2033

Japan Laundry Appliances Market Overview The Japan Laundry Appliances Market is positioned for steady and resilient growth over the forecast period, reflecting the country’s deep-rooted culture of technological innovation, premium consumer expectations, and lifestyle-driven purchasing behavior. According to Renub Research, the market is projected to grow from US$ 3.12 billion in 2024 to US$ 4.08 billion by 2033, registering a CAGR of 3.02% from 2025 to 2033.

By Marthan Sir20 days ago in Filthy

Digital Signage Market Size and Forecast 2025–2033

Global Digital Signage Market Outlook: A New Era of Visual Communication The global digital signage market is undergoing a major transformation as organizations across industries shift from static displays to dynamic, data-driven visual communication platforms. Digital signage—encompassing LED, LCD, OLED, projection systems, and interactive kiosks—has become a cornerstone of modern advertising, information delivery, and customer engagement.

By Janine Root about 15 hours ago in Filthy

You Know Her

Many people say, “I know her,” when they hear the name Mia Khalifa. They say it with confidence, as if they truly understand who she is and what her life means. But knowing a name is not the same as knowing a person. Mia Khalifa is one of the most searched names on the internet, yet she is also one of the most misunderstood public figures of our time.

By John Smith7 days ago in Filthy

How, Too

Many people wonder how, too. You are not alone, and I am an expert. I will teach you how, too! First, you need to remit a small application fee and fill out an application describing the nature of your financial situation and how often payments will be made, as this will have great bearing on how well I teach you how, too.

By Harper Lewis3 days ago in Fiction

Comments

There are no comments for this story

Be the first to respond and start the conversation.