Global Free-From Food Market Size & Forecast 2025–2033

Rising Health Awareness and Clean-Label Demand Drive a New Era of Inclusive Nutrition

Global Free-From Food Market Overview

The Global Free-From Food Market is witnessing a transformative expansion as consumers worldwide increasingly prioritize health, dietary transparency, and allergen-safe nutrition. According to Renub Research, the market is projected to grow from US$ 101.34 billion in 2024 to US$ 293.46 billion by 2033, registering a strong CAGR of 12.54% from 2025 to 2033.

This robust growth reflects a structural shift in global food consumption patterns. Free-from foods—products formulated without gluten, dairy, lactose, nuts, eggs, or other common allergens—are no longer niche offerings reserved for individuals with medical dietary needs. Instead, they have become mainstream lifestyle choices for consumers seeking cleaner labels, improved digestion, and preventive health benefits.

Rising food allergy awareness, increasing diagnosis of intolerances, and the rapid adoption of wellness-oriented diets such as vegan, paleo, and flexitarian eating are positioning free-from foods as a central pillar of the modern food industry.

Understanding Free-From Foods and Their Global Relevance

Free-from food products are specifically designed to eliminate ingredients commonly associated with allergies, intolerances, or dietary restrictions. These products cater to individuals with celiac disease, lactose intolerance, nut allergies, and egg sensitivities, as well as consumers who voluntarily avoid certain ingredients for health, ethical, or environmental reasons.

Beyond personal health management, free-from foods are increasingly perceived as healthier and more transparent alternatives. Clean ingredient lists, reduced artificial additives, and improved nutritional profiles make these products attractive to health-conscious shoppers. As a result, free-from foods are now widely adopted across households, foodservice operations, cafés, bakeries, and institutional catering services worldwide.

Manufacturers are also leveraging innovation in plant proteins, fermentation technologies, and alternative grains to create products that closely mimic traditional foods—without compromising safety or taste.

Key Drivers Fueling Market Growth

Rising Health Awareness and Lifestyle Shifts

One of the strongest growth catalysts in the free-from food industry is the global surge in health consciousness. Consumers are proactively reducing their intake of gluten, lactose, artificial preservatives, and allergens as part of preventive healthcare strategies. Fitness culture, wellness programs, and personalized nutrition trends have further accelerated this shift.

Millennials and Gen Z consumers are particularly influential, favoring clean-label, minimally processed, and ethically produced food products. Social media, health influencers, and digital nutrition platforms continue to amplify awareness, normalizing free-from consumption across age groups.

Increasing Prevalence of Food Allergies and Intolerances

The rising incidence of lactose intolerance, gluten sensitivity, and food allergies remains a major structural driver. Lactose intolerance is especially prevalent across Asia-Pacific, Latin America, and the Middle East, while gluten intolerance and celiac disease are more commonly diagnosed in North America and Europe.

Food hypersensitivity—covering both allergies and intolerances—affects an estimated 19% of the U.S. population and between 2% and 37% of Europeans, creating sustained demand for safe and reliable food alternatives. These health realities are driving consistent consumption of lactose-free dairy, gluten-free bakery items, and allergen-free snacks.

Retail Expansion and Product Innovation

The expansion of organized retail and e-commerce has significantly improved accessibility to free-from foods. Supermarkets, hypermarkets, convenience stores, and online platforms now dedicate entire sections to gluten-free, dairy-free, and allergen-free products.

Food manufacturers are investing heavily in R&D to enhance taste, texture, shelf life, and nutritional quality. Innovations such as plant-based cheese, gluten-free bread with improved softness, and allergen-free confectionery are attracting both medical and lifestyle consumers. Digital marketing, premium packaging, and transparent labeling further strengthen consumer trust.

Challenges Limiting Market Penetration

Higher Product Pricing

Despite growing demand, free-from foods often carry a price premium over conventional products. Specialized ingredients, dedicated manufacturing lines, and rigorous quality testing increase production costs. These higher prices can restrict adoption among price-sensitive consumers, particularly in emerging economies.

Taste and Texture Limitations

Although product quality has improved significantly, certain free-from products still face challenges in replicating the sensory experience of traditional foods. Gluten-free bakery items and dairy-free cheese alternatives sometimes fall short in texture or flavor, discouraging repeat purchases. Balancing clean-label formulations with sensory appeal remains a key industry focus.

Key Market Segments

Dairy-Free Free-From Food Market

The dairy-free segment is expanding rapidly due to lactose intolerance, plant-based diet adoption, and environmental concerns. Products such as almond milk, oat milk, soy yogurt, and vegan cheese are increasingly accepted by mainstream consumers. Continuous innovation has narrowed the taste gap with conventional dairy.

Lactose-Free Free-From Food Market

Lactose-free products retain traditional dairy ingredients while eliminating lactose, offering familiar taste and nutrition without digestive discomfort. This segment is particularly strong in Asia-Pacific and Latin America, where lactose intolerance is widespread.

Bakery & Confectionery Segment

Gluten-free breads, cakes, cookies, and allergen-free confectionery are among the most dynamic product categories. Improved formulations, indulgent yet healthy positioning, and dedicated retail shelf space are driving growth in this segment.

Free-From Snacks Market

Free-from snacks are among the fastest-growing categories, fueled by urban lifestyles and on-the-go consumption. Gluten-free chips, nut-free bars, dairy-free chocolates, and plant-based savory snacks appeal strongly to millennials and Gen Z consumers.

Convenience Store Distribution Channel

Convenience stores are increasingly stocking free-from snacks, beverages, and ready-to-eat meals. Premiumization trends in convenience retail align well with the health-focused positioning of free-from foods, supporting mainstream adoption.

Regional Market Insights

United States

The United States represents one of the most mature free-from food markets globally, supported by high consumer awareness, strong retail infrastructure, and rapid innovation. Gluten-free and dairy-free products are now mainstream across supermarkets and foodservice outlets.

In January 2024, Noat Foods launched sugar-free, nut-free chocolates made from sunflower seed butter, targeting allergy-aware consumers.

Germany

Germany leads Europe’s free-from food market, driven by strong demand for clean-label, organic, and allergen-free products. Retailers offer extensive free-from sections, while innovation remains high.

In March 2024, Kynda introduced Europe’s first zero-waste mycelium-based food solution, debuting its “Kynda meat” burger patty in Hamburg.

India

India’s free-from food market is emerging rapidly, supported by urbanization, rising disposable incomes, and widespread lactose intolerance. Branded dairy alternatives and gluten-free products are gaining traction, especially through e-commerce.

In June 2025, Wow! Momo launched India’s first gluten-free momos made from quinoa and chickpeas, reinforcing health-driven innovation.

Brazil

Brazil’s free-from market is expanding steadily, particularly in lactose-free and gluten-free categories. Urban consumers and rising middle-class incomes are supporting adoption.

In September 2024, EMBRAPA announced plans to develop new gluten-free foods using rice, corn, beans, and chickpeas.

Saudi Arabia

Saudi Arabia’s free-from food market is growing rapidly due to lifestyle changes, rising health awareness, and high lactose intolerance prevalence. Modern retail expansion and e-commerce are improving accessibility, while global brands dominate premium segments.

Market Segmentation Snapshot

By Type:

Dairy-Free | Gluten-Free | Lactose-Free | Others

By End Product:

Bakery & Confectionery | Dairy-Free Foods | Snacks | Beverages | Others

By Distribution Channel:

Supermarkets & Hypermarkets | Convenience Stores | Online Channels | Others

By Region:

North America | Europe | Asia Pacific | Latin America | Middle East & Africa

Competitive Landscape

Key players operating in the global free-from food market include:

Danone SA, General Mills Inc., Conagra Brands Inc., Mondelez International, Hain Celestial Group Inc., Dr. Schar AG/SpA, Alpro UK Limited, Doves Farm Foods Limited, Ener-G Foods Inc., and GreenSpace Brands Inc.

Each company is analyzed across five viewpoints: overview, key personnel, recent developments, SWOT analysis, and revenue performance.

Final Thoughts

The Global Free-From Food Market is transitioning from a specialty niche into a mainstream global industry. With rising health awareness, growing intolerance diagnoses, and rapid innovation in clean-label foods, the market is set for sustained double-digit growth through 2033.

As affordability improves and sensory quality continues to advance, free-from foods are expected to become an everyday choice for millions—reshaping the future of global nutrition and inclusive eating.

About the Creator

jaiklin Fanandish

Jaiklin Fanandish, a passionate storyteller with 10 years of experience, crafts engaging narratives that blend creativity, emotion, and imagination to inspire and connect with readers worldwide.

Keep reading

More stories from jaiklin Fanandish and writers in Feast and other communities.

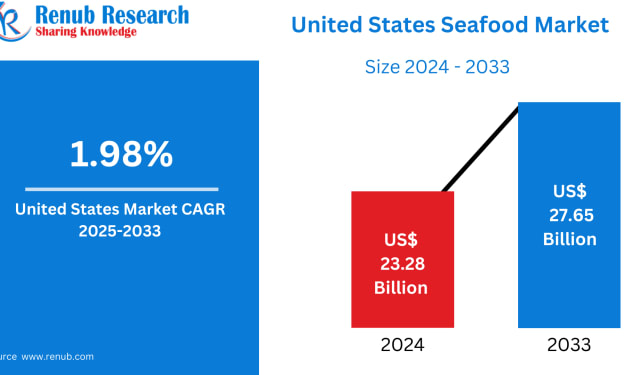

United States Seafood Market Size & Forecast 2025–2033

United States Seafood Market Outlook The United States seafood market is on a steady growth trajectory, reflecting changing consumer preferences, evolving supply chains, and advances in aquaculture and cold-chain logistics. According to Renub Research, the market is expected to expand from US$ 23.28 billion in 2024 to US$ 27.65 billion by 2033, registering a Compound Annual Growth Rate (CAGR) of 1.98% between 2025 and 2033.

By jaiklin Fanandish11 days ago in Feast

My Tous les Jours Trip

As someone who lives in a rural area, I don't get the chance to visit fancy restaurants or bakeries that often. So, when a friend told me about a French-Asian bakery that's less than an hour away, I knew I had to check it out and grab some pictures for social media. Tous les Jours ended up providing an immersive experience that went above and beyond my expectations--although I did leave with a few reservations.

By Kaitlin Shanks16 days ago in Feast

New Ways to Save on the Grocery Budget

With rising grocery prices and stagnant wages, it is time for many people to return to some old tried and true ways of saving money on groceries. While shopping sales and clipping coupons are great choices, there are some other ways that can help you to stretch your grocery budget.

By Brandi Browna day ago in Feast

Comments

There are no comments for this story

Be the first to respond and start the conversation.