What Happens If You Never Pay Off Your Credit Card?

The Real Consequences of Ignoring Credit Card Debt—From Credit Score Damage to Lawsuits and Financial Ruin

Credit cards can be helpful tools when used responsibly. They offer convenience, build credit history, and can even earn you rewards. But what happens if you never pay off your credit card? It’s a question that many avoid until it’s too late. The truth is, ignoring your credit card debt can lead to a serious financial snowball—one that could affect your life for years to come.

Let’s break down exactly what happens when you don’t pay off your credit card balance, what the long-term consequences look like, and how you can escape the trap before it’s too late.

1. Interest Keeps Piling Up

The moment you stop making payments on your credit card, interest continues to accrue—usually at a high rate. Most credit cards have interest rates ranging from 20% to 30% APR. That means a $1,000 balance could turn into $1,300 or more within just a few months. And that’s just the beginning.

Unpaid balances grow quickly. And the longer you wait, the more your debt compounds. What started as a manageable monthly payment can soon become a mountain of debt you can’t climb.

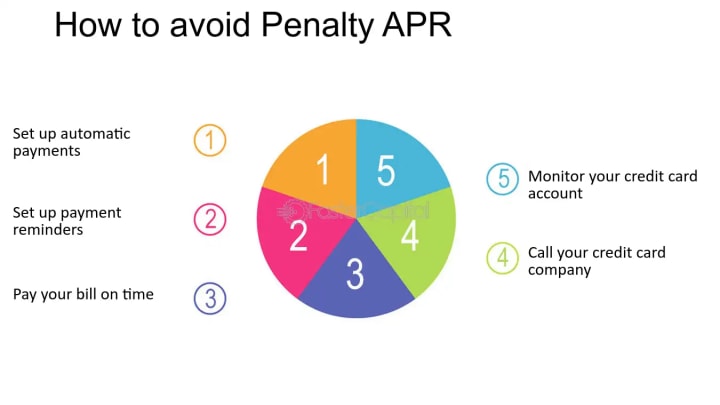

2. Late Fees and Penalty APRs Kick In

After just one missed payment, your card issuer will likely charge a late fee (often $30–$40). If you continue missing payments, you could be hit with penalty APRs, pushing your interest rate even higher.

Some card issuers will raise your interest rate to the maximum limit allowed if you're more than 60 days late. That means your debt is now growing even faster, making it nearly impossible to pay down the balance.

3. Your Credit Score Starts Dropping

This is one of the most damaging effects. Your credit score is your financial reputation, and missing payments can crush it. Credit card companies usually report missed payments to credit bureaus after 30 days.

- 30 Days Late: Small dip in your credit score.

- 60–90 Days Late: Bigger drop—up to 100 points or more.

- 120+ Days Late: You risk default and your account may be charged off.

With a lower credit score, you’ll face higher interest rates, denied loan applications, and difficulty renting an apartment or even getting a job in some industries.

4. Debt Collectors Get Involved

Once your account is seriously past due (usually after 120–180 days), your credit card company might sell your debt to a collection agency. Now, you’re not just dealing with missed payments—you’re being hounded by debt collectors.

These agencies are persistent. You might receive constant calls, letters, and even threats of legal action. Some debt collectors operate aggressively, making your life stressful and difficult.

5. Legal Action and Wage Garnishment

If the debt remains unpaid, the credit card company or collection agency might sue you in court. If they win, they can get a judgment against you, which may allow them to:

- Garnish your wages

- Freeze your bank accounts

- Place a lien on your property

Now, your unpaid credit card debt is no longer just a financial burden—it’s a legal one.

6. Long-Term Financial Consequences

Letting your credit card debt spiral out of control can affect your life in countless ways for years:

- Ruined Credit History: Late payments stay on your report for up to seven years.

- Higher Loan Costs: Even if you get approved for a loan, you'll likely pay much higher interest.

- Difficulty Rebuilding Credit: You may need to start over with a secured credit card or credit-builder loan.

Plus, there’s the mental toll: stress, anxiety, and feelings of helplessness that come from financial instability.

7. Can You Go to Jail for Not Paying a Credit Card?

No, you cannot be jailed for not paying a credit card bill—debtors’ prisons were abolished long ago. However, ignoring a court summons can result in legal trouble. Always respond to legal notices to protect your rights.

8. How to Get Out Before It’s Too Late

If you’ve missed payments or feel overwhelmed, don’t panic. You still have options:

Call Your Credit Card Company: Many lenders offer hardship programs.

Set Up a Payment Plan: Even small payments show good faith.

Seek Credit Counselling: Certified agencies can help negotiate with creditors.

Consider Debt Consolidation: Combine multiple debts into one lower-interest loan.

Explore a Balance Transfer: Move your balance to a card with 0% APR for a limited time (if your credit allows).

Final Thoughts: Don’t Wait—Act Now

Unpaid credit card debt doesn’t just disappear. It grows—along with the consequences. From massive interest and fees to lawsuits and destroyed credit, the price of ignoring your credit card is high.

But the sooner you act, the more control you can regain. Start with small steps. Talk to your creditors. Make partial payments. Ask for help.

Financial freedom starts with taking action—no matter how deep in debt you are.

About the Creator

Keep reading

More stories from Bevy Osuos and writers in Trader and other communities.

Elon Musk Loses $29 Billion in a Day! Is Tesla in Trouble?

Elon Musk, the visionary billionaire behind Tesla, SpaceX, and several other high-profile ventures, just faced one of the biggest financial hits of his career. In a single trading day, his net worth plummeted by a staggering $29 billion due to a sharp decline in Tesla’s stock price.

By Bevy Osuos10 months ago in Trader

Ctoph Exchange: Advancing Scalability and Security in Blockchain

Executive Summary In recent years, blockchain technology has emerged as a transformative force across multiple industries, redefining the way data is stored, transferred, and secured. Ctoph Exchange, a rising player in the financial technology ecosystem, has dedicated significant resources to studying blockchain and its applications. This report examines Ctoph Exchange’s research approach, technological focus areas, strategic implications, and the potential impact of their findings on the broader blockchain ecosystem.

By Ctoph Exchange4 days ago in Trader

Comments

There are no comments for this story

Be the first to respond and start the conversation.