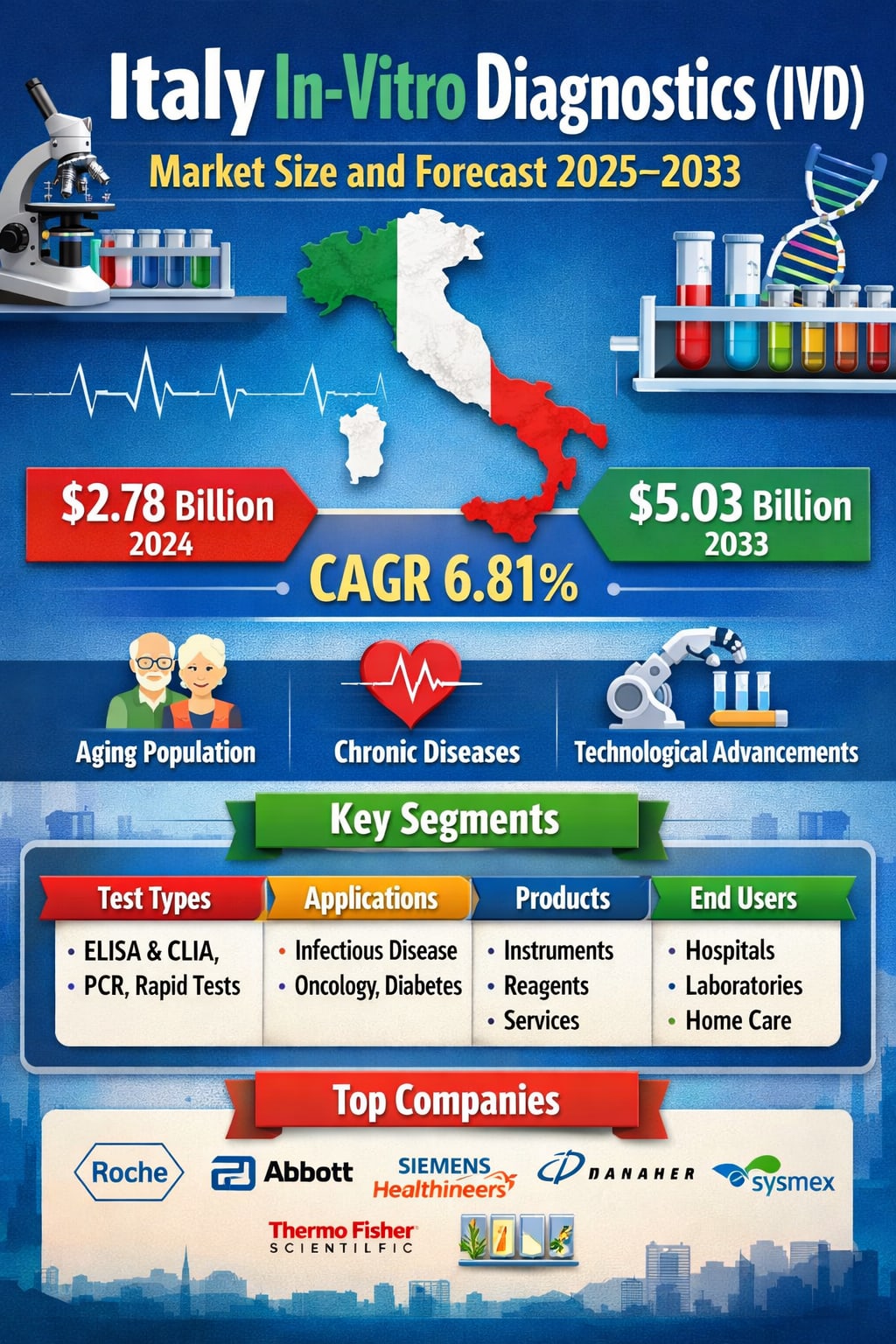

Italy In-Vitro Diagnostics (IVD) Market Size and Forecast 2025–2033

A Deep Dive into Growth Drivers, Technologies, Key Segments, and the Future of Diagnostics in Italy’s Evolving Healthcare System

Italy In-Vitro Diagnostics (IVD) Market Overview

In-Vitro Diagnostics (IVD) refers to medical tests performed on biological samples such as blood, urine, tissue, or saliva outside the human body. These tests are essential for detecting diseases, monitoring ongoing conditions, guiding treatment decisions, and supporting preventive healthcare strategies. From simple blood glucose tests to advanced molecular diagnostics and genetic screening, IVD technologies sit at the heart of modern medicine.

In Italy, the importance of IVD has grown steadily over the past decade, supported by a strong public healthcare system, rising healthcare awareness, and an aging population that requires continuous medical monitoring. The COVID-19 pandemic further highlighted how critical diagnostics are—not just for hospitals and laboratories, but also for public health planning and everyday clinical decision-making.

According to Renub Research, the Italy In-Vitro Diagnostics (IVD) Market was valued at USD 2.78 billion in 2024 and is expected to reach USD 5.03 billion by 2033, expanding at a CAGR of 6.81% from 2025 to 2033. This growth reflects increasing demand for early and precise diagnosis, continued investment in laboratory infrastructure, and rapid adoption of automation and molecular testing technologies across the country.

Italy’s healthcare model, which combines strong public funding with an expanding private diagnostics sector, has created fertile ground for innovation in IVD. Today, diagnostics are no longer seen as a supporting service alone—they are a strategic pillar of healthcare delivery, disease prevention, and cost-effective patient management.

Market Growth Outlook: Why Italy’s IVD Sector Is Expanding

The Italian IVD market is being shaped by a combination of demographic, clinical, and technological forces. Together, these trends are pushing diagnostics from a reactive tool toward a proactive, predictive, and personalized healthcare solution.

Aging Population and Rising Chronic Disease Burden

Italy has one of the oldest populations in Europe, with a median age exceeding 48 years and nearly one in four residents aged over 65. This demographic reality has major implications for healthcare demand. Chronic conditions such as diabetes, cardiovascular diseases, cancer, kidney disorders, and autoimmune diseases require continuous testing for diagnosis, monitoring, and treatment optimization.

IVD technologies play a central role in managing these long-term conditions. Regular blood tests, biomarker analysis, and molecular diagnostics allow clinicians to track disease progression, adjust therapies, and prevent complications. As awareness of preventive healthcare grows, both public and private healthcare providers in Italy are increasing their reliance on diagnostic testing—directly boosting the demand for IVD products and services.

Government Investment and National Screening Programs

The Italian government actively supports public health through nationwide screening programs for cancer, infectious diseases, and genetic conditions. These initiatives rely heavily on in-vitro diagnostics for early and accurate detection, which is critical for improving treatment outcomes and reducing long-term healthcare costs.

In recent years, healthcare funding and alignment with broader EU health strategies have strengthened laboratory infrastructure and accelerated the adoption of advanced diagnostic equipment. Public awareness campaigns and free or subsidized screening programs have also increased test volumes across the country, firmly embedding IVD into routine healthcare practice.

A notable example is the 2025 budget framework, which includes incentives for innovative anti-infective treatments. Such policy measures indirectly support the diagnostics sector, as effective treatment strategies depend on precise and timely diagnostic information. This policy-driven environment continues to create a favorable outlook for the Italian IVD market.

Technological Advancements and Laboratory Automation

Italy’s diagnostics landscape is rapidly evolving with the adoption of automation, digital diagnostics, and molecular testing platforms. Clinical laboratories are investing in high-throughput systems that improve efficiency, reduce human error, and deliver faster turnaround times.

Technologies such as CLIA, PCR, and next-generation sequencing are increasingly used in oncology, infectious disease testing, and genetic screening. Automation not only improves productivity but also enhances diagnostic accuracy and consistency—key priorities for both public hospitals and private laboratories.

Partnerships between diagnostic companies, such as collaborations to distribute advanced immunoassay and point-of-care solutions, further illustrate how innovation is shaping the market. As laboratories modernize their workflows, the demand for sophisticated instruments and reagents continues to rise.

Key Challenges Facing the Italy IVD Market

Despite strong growth prospects, the Italian IVD market also faces structural and economic challenges that could influence its long-term trajectory.

Regional Disparities in Healthcare Access

Italy’s decentralized healthcare system has led to noticeable differences in diagnostic infrastructure between regions. Northern regions typically have better-equipped laboratories and faster access to advanced technologies, while some southern regions face limitations in infrastructure, funding, and skilled personnel.

These disparities affect both patient access to high-quality diagnostics and the overall market’s growth potential. Bridging this gap will require targeted investment, policy coordination, and incentives to ensure more uniform access to diagnostic services nationwide.

Cost Constraints and Reimbursement Issues

Although Italy has a publicly funded healthcare system, budgetary pressures remain a reality. Not all advanced diagnostic tests receive full or timely reimbursement, particularly newer or highly specialized technologies. This can slow the adoption of innovative IVD solutions and limit the ability of laboratories to upgrade equipment.

Balancing innovation with cost-efficiency remains a central challenge. Market players must demonstrate not only clinical value but also economic benefits to ensure broader adoption within the healthcare system.

Segment Insights: How the Market Is Shaping Up

ELISA & CLIA: The Backbone of Immunodiagnostics

ELISA and CLIA technologies are among the most widely used diagnostic tools in Italy, especially for detecting infectious diseases, hormones, and cancer biomarkers. Their high sensitivity, specificity, and compatibility with automation make them ideal for both routine and specialized testing.

With Italy’s growing focus on early diagnosis—particularly in oncology and infectious diseases—CLIA platforms are increasingly being adopted in hospitals and large laboratories. Their ability to deliver high-throughput, reliable results supports large-scale screening programs and routine clinical workflows alike.

Rapid Tests: Convenience Meets Clinical Need

Rapid diagnostic tests have gained strong momentum in Italy, especially after the COVID-19 pandemic familiarized both healthcare professionals and the general public with quick, point-of-care testing solutions.

These tests are now widely used for infectious diseases, chronic condition monitoring, and preliminary screening. Their ease of use, fast results, and suitability for home care settings make them particularly attractive in an aging society where mobility and convenience matter. As home-based healthcare continues to expand, rapid tests are expected to remain a key growth area within the IVD market.

Instruments: Powering the Shift Toward Automation

The demand for advanced IVD instruments in Italy is rising as laboratories move toward automation and digital integration. Hematology analyzers, molecular diagnostic systems, and clinical chemistry analyzers are being deployed to handle increasing test volumes more efficiently.

Hospitals and private labs are investing in scalable, high-throughput platforms that integrate with Laboratory Information Management Systems (LIMS). This digital connectivity improves data accuracy, streamlines workflows, and supports faster clinical decision-making—making instruments a critical pillar of market growth.

Application and Technology Trends

Infectious Disease Diagnostics: A Strategic Priority

Infectious disease testing remains a cornerstone of Italy’s IVD market. Continuous demand for COVID-19, influenza, HIV, hepatitis, and STI testing keeps this segment robust. Government surveillance programs and public health initiatives further support sustained testing volumes.

Molecular diagnostics and antigen tests are widely used in both centralized laboratories and point-of-care settings, ensuring rapid response and effective disease control strategies.

Clinical Chemistry: The Stable Core of Diagnostics

Clinical chemistry testing forms the backbone of routine diagnostics in Italy, covering tests for glucose, electrolytes, enzymes, and metabolic markers. These tests are essential for managing chronic diseases such as diabetes, cardiovascular conditions, and kidney disorders.

Italian laboratories prioritize reliability, automation, and efficiency in this segment. Modern clinical chemistry analyzers now offer compact designs, high throughput, and low maintenance—ensuring this segment remains stable and essential within the broader IVD market.

End Users: Where the Demand Comes From

Italy’s IVD market is served primarily by hospitals, laboratories, and an expanding home care segment.

Hospitals and centralized laboratories account for the majority of testing volumes, especially in urban areas. These institutions are increasingly adopting automated systems, AI-assisted diagnostics, and digital lab management tools to cope with rising demand and complexity.

At the same time, home care diagnostics are gaining traction, driven by an aging population, chronic disease management needs, and patient preference for convenient testing solutions outside traditional healthcare facilities.

Key Market Segments

By Test Types:

ELISA & CLIA

PCR

Rapid Test

Fluorescence Immunoassays (FIA)

In Situ Hybridization

Transcription Mediated Amplification

Sequencing

Colorimetric Immunoassay

Radioimmunoassay (RIA)

Isothermal Nucleic Acid Amplification Technology

Others

By Product:

Services

Instruments

Reagents

By Application:

Infectious Disease

Diabetes

Cardiology

Oncology

Nephrology

Autoimmune Diseases

Drug Testing

Other Applications

By Technology:

Immunoassay

Clinical Chemistry

Molecular Diagnostics/Genetics

Hematology

Microbiology

Coagulation

Others

By End User:

Hospitals

Laboratories

Home Care

Others

Competitive Landscape and Key Players

The Italian IVD market is highly competitive, with major global players maintaining strong positions through broad product portfolios, technological innovation, and strategic partnerships. Key companies include:

Roche Diagnostics

Abbott Diagnostics

Siemens Healthineers

Danaher Corporation

Thermo Fisher Scientific

Sysmex Corporation

These companies compete across multiple dimensions, including technology, service quality, automation capabilities, and geographic reach. Their continued investment in R&D and digital diagnostics is expected to shape the future of Italy’s IVD ecosystem.

Final Thoughts: A Market Built for the Future

The Italy In-Vitro Diagnostics (IVD) Market is on a strong and sustainable growth path, driven by demographic trends, government healthcare initiatives, and rapid technological progress. From USD 2.78 billion in 2024 to an expected USD 5.03 billion by 2033, the market’s expansion at a 6.81% CAGR reflects the rising strategic importance of diagnostics in modern healthcare.

As Italy continues to prioritize early detection, preventive care, and efficient disease management, IVD will remain at the center of its healthcare transformation. While challenges such as regional disparities and reimbursement pressures persist, ongoing investment in automation, molecular diagnostics, and digital health solutions positions the market for long-term resilience and innovation.

About the Creator

Europe Agricultural Equipment Market Size and Forecast 2025–2033

Introduction: A Market Driving Europe’s Food Security The Europe Agricultural Equipment Market stands at the heart of the continent’s food security, sustainability goals, and technological transformation. Valued at USD 46.86 billion in 2024, the market is expected to grow steadily to USD 67.68 billion by 2033, registering a CAGR of 4.17% from 2025 to 2033, according to Renub Research. This growth is not happening in isolation. It reflects a deeper structural shift in European farming—one shaped by rising labor costs, aging farmer populations, stricter environmental regulations, and the rapid adoption of precision agriculture technologies.

By Sakshi Sharmaa day ago in Trader

Comments

There are no comments for this story

Be the first to respond and start the conversation.