Global In-Vitro Diagnostics Market Size and Forecast 2025–2033

How technology, preventive healthcare, and personalized medicine are reshaping the future of diagnostics worldwide

Introduction: Diagnostics at the Heart of Modern Healthcare

In-vitro diagnostics (IVD) has become one of the most critical pillars of modern healthcare systems. From routine blood tests to advanced genetic screening, these diagnostic tools guide clinical decisions, enable early disease detection, and help physicians monitor treatment outcomes with precision. As healthcare systems worldwide shift toward preventive and personalized care, the importance of reliable and accessible diagnostic testing continues to grow.

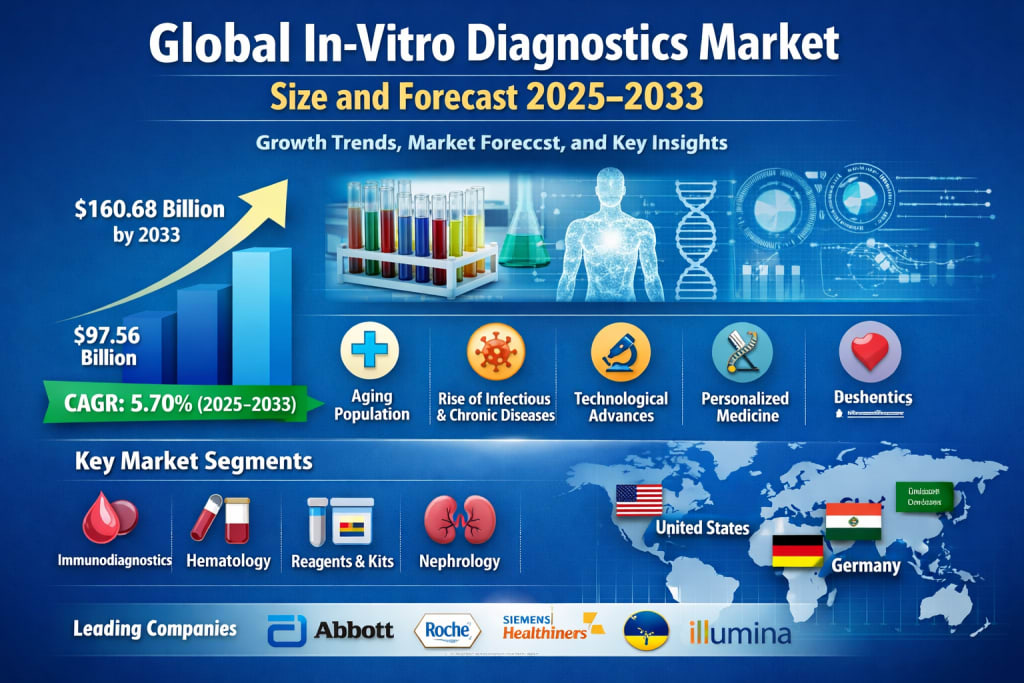

According to Renub Research, the global in-vitro diagnostics market is expected to expand from around US$ 97.56 billion in 2024 to nearly US$ 160.68 billion by 2033, registering a compound annual growth rate (CAGR) of 5.70% during 2025–2033. This steady growth reflects a healthcare landscape increasingly driven by aging populations, rising chronic and infectious disease burdens, rapid technological innovation, and the growing emphasis on precision medicine.

In essence, diagnostics is no longer just a supporting function in healthcare—it is becoming the foundation upon which modern medicine is built.

In-Vitro Diagnostics Market Overview

In-vitro diagnostics refers to medical tests and devices used to analyze biological samples such as blood, urine, or tissue outside the human body. These tests help clinicians diagnose diseases, monitor health conditions, assess disease progression, and evaluate treatment effectiveness. IVD products range from simple pregnancy tests to complex molecular and genetic assays used in oncology and infectious disease management.

Over the past decade, the global IVD market has witnessed remarkable transformation. The rising prevalence of chronic diseases such as diabetes, cardiovascular disorders, and cancer has significantly increased the demand for frequent and accurate testing. At the same time, infectious disease outbreaks—including the COVID-19 pandemic—have highlighted the critical role of fast, scalable, and reliable diagnostic solutions in public health preparedness.

Another powerful driver is the global aging population. Older individuals typically require more frequent medical testing due to higher susceptibility to chronic conditions and age-related disorders. This demographic shift is steadily increasing the volume of diagnostic procedures performed worldwide, thereby supporting long-term market growth.

Technological innovation has further accelerated adoption. Advances in molecular diagnostics, automation, digital pathology, and point-of-care testing have made diagnostics faster, more accurate, and more accessible. In parallel, the move toward personalized medicine—where treatments are tailored to individual patient profiles—has elevated the role of diagnostics in treatment planning and therapy selection.

Growth Drivers in the In-Vitro Diagnostics Market

Rising Prevalence of Chronic and Infectious Diseases

The global burden of both chronic and infectious diseases continues to rise, creating sustained demand for reliable diagnostic solutions. Conditions such as diabetes, cancer, cardiovascular diseases, and autoimmune disorders require ongoing monitoring, while infectious diseases demand rapid and accurate detection to prevent widespread transmission.

Non-communicable diseases (NCDs) now account for a significant share of global mortality, including a large number of premature deaths in low- and middle-income countries. Lifestyle factors such as unhealthy diets, physical inactivity, tobacco use, excessive alcohol consumption, and air pollution further exacerbate this trend. As a result, routine screening and early diagnosis have become essential components of public health strategies worldwide.

At the same time, infectious disease outbreaks have reinforced the importance of robust diagnostic infrastructure. The COVID-19 pandemic demonstrated how critical large-scale testing capacity is for managing public health crises. This experience has led governments and healthcare systems to invest more heavily in diagnostic preparedness, benefiting the IVD market in the long term.

Technological Advances and Automation in Testing

Technological progress remains one of the strongest growth engines of the IVD industry. Automation, digitalization, and artificial intelligence have transformed laboratory workflows, enabling higher throughput, improved accuracy, and faster turnaround times. Modern diagnostic platforms can now process thousands of samples per day while minimizing human error.

Molecular diagnostics, next-generation sequencing (NGS), and advanced immunoassay systems have expanded the scope of what can be detected and analyzed. These technologies are especially impactful in oncology, genetic testing, and infectious disease diagnostics, where precision and sensitivity are critical.

Point-of-care (POC) testing is another major innovation, bringing diagnostics closer to patients. Compact and user-friendly devices allow testing to be performed in clinics, pharmacies, and even at home, improving access to care and speeding up clinical decision-making.

Increasing Use of Preventive and Personalized Medicine

Healthcare systems around the world are shifting from reactive treatment models to proactive and preventive care approaches. Regular screening programs, early risk assessment, and continuous health monitoring are becoming standard practice in many countries. This trend naturally increases the demand for diagnostic tests across a wide range of medical specialties.

At the same time, personalized medicine is gaining momentum. By using genomic, molecular, and biomarker-based diagnostics, clinicians can design targeted therapies that are more effective and have fewer side effects. Pharmaceutical companies also rely on companion diagnostics to identify the patients most likely to benefit from specific treatments, further strengthening the link between diagnostics and therapeutics.

Together, these trends are redefining diagnostics as a strategic tool for improving patient outcomes rather than just a supporting clinical service.

Challenges in the In-Vitro Diagnostics Market

High Cost of Advanced Diagnostic Technologies

Despite their clinical benefits, advanced diagnostic systems often come with high acquisition and operating costs. Automated platforms, molecular testing systems, and AI-enabled solutions require significant capital investment, as well as ongoing expenses for maintenance, calibration, and skilled personnel.

For smaller laboratories and healthcare facilities—especially in developing regions—these costs can be prohibitive. From a patient perspective, high out-of-pocket expenses for specialized tests may also limit access, reducing overall utilization. Balancing innovation with affordability remains a key challenge for the industry.

Stringent Regulatory and Reimbursement Barriers

The IVD industry operates under strict regulatory frameworks designed to ensure safety, accuracy, and reliability. While these regulations are essential, lengthy approval processes can delay product launches and slow down innovation. Moreover, regulatory requirements vary by region, increasing complexity and compliance costs for global manufacturers.

Reimbursement policies present another hurdle. In many markets, advanced diagnostic tests are not fully covered by insurance or public healthcare systems, which can discourage adoption even when the clinical value is clear. Aligning regulatory and reimbursement systems with the pace of technological progress will be critical for sustaining long-term growth.

Key Market Segments

Immunodiagnostics

Immunodiagnostics is one of the most important segments of the IVD market, focusing on the detection of antigens and antibodies. These tests are widely used in infectious disease diagnosis, cancer marker detection, and autoimmune disorder screening. Technologies such as ELISA and chemiluminescence immunoassays have significantly improved sensitivity, specificity, and efficiency.

The growing emphasis on early diagnosis and large-scale screening programs continues to support strong demand for immunodiagnostic solutions worldwide.

Hematology Diagnostics

Hematology diagnostics plays a crucial role in identifying and monitoring blood-related disorders such as anemia, leukemia, and infections. Automated hematology analyzers now provide rapid and accurate complete blood counts, supporting both routine check-ups and complex clinical decisions. The integration of digital imaging and flow cytometry has further enhanced diagnostic precision in this segment.

Reagents and Kits

Reagents and kits represent the largest revenue-generating segment of the IVD market due to their recurring use in routine testing. The COVID-19 pandemic highlighted their strategic importance, as demand for PCR and rapid antigen test kits surged worldwide. Ongoing innovation in assay design and the expansion of laboratory networks in emerging markets continue to drive growth in this segment.

IVD Instruments and Reusable Devices

Diagnostic instruments form the technological backbone of the industry, enabling automation, high-throughput testing, and data integration. Reusable IVD devices, in particular, are gaining attention for their cost-effectiveness and sustainability. While upfront costs can be high, their long-term economic and environmental benefits make them attractive to hospitals and large diagnostic laboratories.

Nephrology Diagnostics

With the global rise in chronic kidney disease—often linked to diabetes and hypertension—nephrology diagnostics is becoming increasingly important. Tests measuring creatinine, urea, and other biomarkers are essential for early detection and disease monitoring. Growing awareness and regular screening programs are steadily expanding this segment.

Clinical Laboratories

Clinical laboratories remain the primary end-users of IVD products. The ongoing shift toward automation, digital reporting, and AI-assisted interpretation is transforming laboratory operations, improving efficiency, and enhancing diagnostic accuracy. As test volumes continue to rise, this segment will remain a central driver of market growth.

Regional Market Insights

United States

The United States is the largest and most technologically advanced IVD market globally. High healthcare spending, strong research and development activity, and rapid adoption of innovative diagnostics support sustained growth. The country also leads in molecular diagnostics, companion testing, and digital pathology, reinforcing its role as a global innovation hub.

Germany

Germany stands out as a key player in Europe’s IVD market, supported by a robust healthcare system and strong emphasis on quality and preventive care. The country’s aging population and high prevalence of chronic diseases continue to drive demand, while strict regulatory standards ensure high product quality and reliability.

India

India’s IVD market is expanding rapidly due to rising healthcare awareness, urbanization, and improved access to diagnostics. The growing burden of diabetes, cancer, and infectious diseases, combined with government initiatives to strengthen healthcare infrastructure, is creating significant opportunities for both domestic and international manufacturers.

Saudi Arabia

Saudi Arabia’s IVD market is benefiting from the country’s healthcare transformation initiatives under Vision 2030. Increased investment in modern diagnostic infrastructure, combined with rising chronic disease prevalence and the growth of private healthcare, is positioning the country as a major diagnostics hub in the Middle East.

Competitive Landscape: Key Players

The global in-vitro diagnostics market is highly competitive, with major players focusing on innovation, strategic partnerships, and geographic expansion. Leading companies include:

Abbott Laboratories

Agilent Technologies Inc.

bioMérieux SA

Bio-Rad Laboratories Inc.

F. Hoffmann-La Roche Ltd

Fujifilm Holdings Corporation

Illumina Inc.

Qiagen NV

Quest Diagnostics

Sysmex Corporation

These companies continue to invest heavily in research and development to introduce next-generation diagnostic solutions and strengthen their market positions.

Final Thoughts

The global in-vitro diagnostics market is entering a new era—one defined by technological sophistication, preventive healthcare, and personalized medicine. With the market projected to grow from US$ 97.56 billion in 2024 to about US$ 160.68 billion by 2033, the industry is set for steady and sustainable expansion.

While challenges such as high costs and regulatory complexity remain, the long-term fundamentals are strong. Rising disease burdens, aging populations, and the relentless push for more precise and accessible healthcare will continue to place diagnostics at the center of medical decision-making.

About the Creator

North America Powder Dietary Supplements Market Size and Forecast 2025

Market Snapshot The North America powder dietary supplements market is estimated to be around USD 9.33 billion in 2024 and is anticipated to grow to USD 23.35 billion by 2033, expanding at a CAGR of 10.78% between 2025 and 2033. This impressive growth is being driven by rising health awareness, increasing demand for vitamin and protein supplementation, and a strong consumer preference for convenient, nutrient-dense powdered formats.

By shibansh kumarabout 5 hours ago in Trader

📢 Raise Your Voice Thread: 02/05/2026

Our “Raise Your Voice Threads” are hosted most alternating Thursdays at 12PM ET to offer creators more avenues to uncover exceptional stories on Vocal. As we are continuously searching for fresh creators and inspiring stories, this thread provides an opportunity to exchange and discuss the stories that have moved and motivated us on Vocal.

By Raise Your Voice by Vocal4 days ago in Resources

Comments

There are no comments for this story

Be the first to respond and start the conversation.