Europe In-Vitro Diagnostics (IVD) Market Trends & Growth Outlook (2025–2033)

Rising Disease Burden, Aging Population, and Diagnostic Innovation Power Europe’s IVD Market Expansion

Introduction: Diagnostics at the Heart of Modern European Healthcare

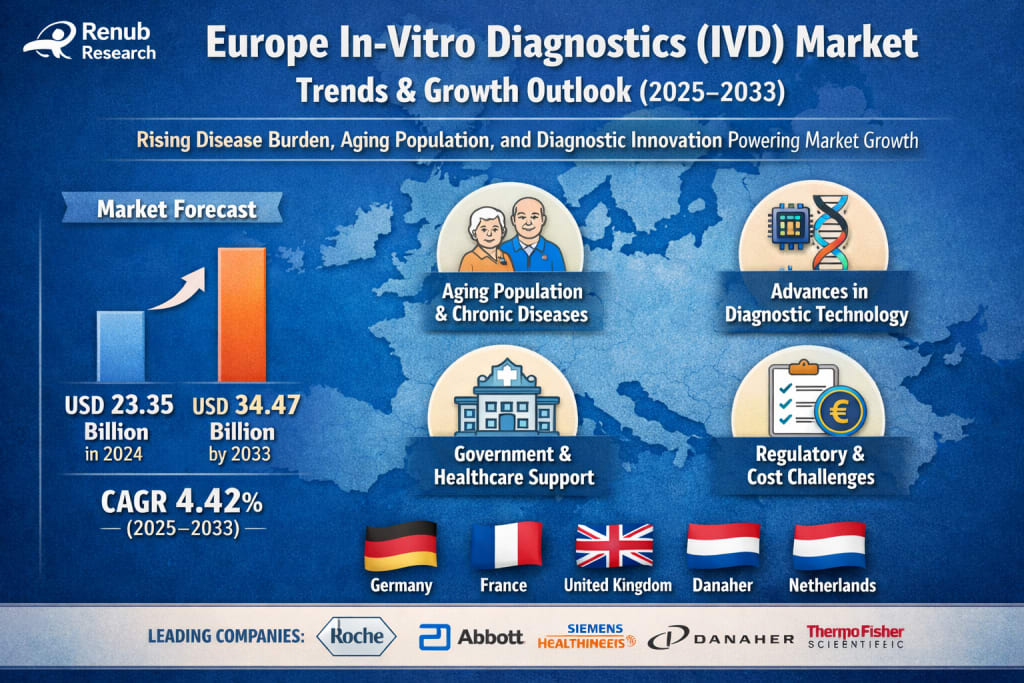

The Europe In-Vitro Diagnostics (IVD) market is entering a decisive phase of growth, driven by rising healthcare demands, rapid technological innovation, and a strong policy focus on early disease detection. According to Renub Research, the Europe In-Vitro Diagnostics (IVD) Market was valued at USD 23.35 billion in 2024 and is expected to reach USD 34.47 billion by 2033, expanding at a CAGR of 4.42% from 2025 to 2033.

This steady growth reflects the central role diagnostics now play in healthcare decision-making. In-vitro diagnostics involve tests performed on samples such as blood, urine, or tissues taken from the human body to detect diseases, infections, or medical conditions. These tests are conducted outside the body in controlled environments using specialized instruments, reagents, and software systems. From routine blood glucose testing and pregnancy tests to complex molecular diagnostics and cancer biomarker analysis, IVD solutions are now indispensable to modern medicine.

Across Europe, healthcare systems are under increasing pressure from aging populations, rising chronic disease prevalence, and the need to control healthcare costs while improving outcomes. In this context, IVD technologies offer a powerful tool: enabling early diagnosis, supporting personalized treatment strategies, and helping clinicians monitor disease progression more accurately and efficiently.

Europe IVD Market Outlook: A Strong Foundation for Long-Term Growth

Europe has one of the world’s most developed healthcare ecosystems, supported by strong public health systems, advanced research institutions, and a mature medical technology industry. Countries such as Germany, France, and the United Kingdom are at the forefront of adopting new diagnostic technologies, while nations across Western and Northern Europe continue to invest heavily in laboratory infrastructure and digital health solutions.

IVD testing is now routine not only in hospitals and centralized laboratories but also increasingly in outpatient clinics and home-care settings. The growth of point-of-care testing and self-testing kits has expanded access to diagnostics, reduced the burden on hospitals, and improved patient convenience. The COVID-19 pandemic played a major role in accelerating public awareness and acceptance of diagnostic testing, a trend that has continued into other disease areas such as infectious diseases, diabetes, and cardiovascular conditions.

At the same time, Europe’s growing focus on personalized medicine and preventive healthcare is reshaping the diagnostics landscape. Advanced molecular diagnostics, genetic testing, and biomarker-based assays are becoming essential tools for tailoring treatments to individual patients, improving outcomes, and optimizing healthcare spending.

Key Drivers of Growth in the Europe IVD Market

Aging Population and Rising Chronic Diseases

One of the most powerful drivers of IVD demand in Europe is demographic change. The region is experiencing a significant increase in its elderly population, which is more vulnerable to chronic conditions such as diabetes, cardiovascular diseases, cancer, and kidney disorders. As life expectancy rises, so does the need for regular diagnostic testing to support early detection, ongoing disease monitoring, and treatment optimization.

Preventive healthcare is becoming a central priority across Europe, and IVD tests are a cornerstone of this approach. Routine blood tests, biomarker screenings, and metabolic panels are increasingly integrated into standard health check-ups. Countries like Germany and Italy, with large aging populations, are seeing particularly strong demand for diagnostic services that support long-term disease management.

Technological Progress in Diagnostics

Technological innovation is transforming the IVD sector at an unprecedented pace. Advances in automation, digitalization, artificial intelligence, and next-generation sequencing (NGS) have significantly improved the accuracy, speed, and efficiency of diagnostic testing. High-throughput platforms allow laboratories to process large volumes of samples quickly, while AI-driven tools support more precise data interpretation and clinical decision-making.

Europe has been quick to adopt these innovations, supported by strong investments in healthcare infrastructure and research. Laboratory automation and miniaturization of diagnostic devices are also expanding the reach of IVD testing beyond traditional lab settings into clinics and homes. These trends are not only improving patient outcomes but also helping healthcare systems manage costs and resource constraints more effectively.

Government Support and Healthcare Infrastructure

Europe benefits from robust public healthcare systems and proactive regulatory frameworks that promote access to diagnostic services. National and EU-level health programs emphasize disease prevention, early detection, and population screening—particularly in areas such as cancer and infectious diseases. Reimbursement policies in many countries further support the adoption of essential diagnostic tests.

Public funding for laboratory infrastructure, combined with partnerships between governments, research institutions, and diagnostic companies, has positioned Europe as a global leader in IVD innovation and implementation. These collaborations are critical for translating scientific advances into practical, widely accessible diagnostic solutions.

Challenges Facing the Europe IVD Market

Complex Regulatory Environment

The introduction of the EU In Vitro Diagnostic Regulation (IVDR) has significantly increased regulatory scrutiny for IVD manufacturers. While these regulations aim to improve patient safety and product quality, they also require more extensive clinical evidence, stricter conformity assessments, and greater involvement of notified bodies. For smaller companies in particular, this can mean higher compliance costs, longer approval timelines, and delays in bringing new products to market.

During the transition period, some products have faced temporary market disruptions, creating uncertainty for both suppliers and healthcare providers. Although the long-term impact of IVDR is expected to be positive in terms of quality and safety, short- to medium-term challenges remain.

High Costs and Reimbursement Limitations

Advanced diagnostic technologies often come with high upfront costs, which can be a barrier to adoption, especially in countries with tighter healthcare budgets. Not all diagnostic tests are fully reimbursed under public healthcare schemes, leading to disparities in access across different European markets. In addition, variations in reimbursement policies between countries complicate market entry strategies for multinational IVD companies.

Cost pressures within healthcare systems also place limits on how quickly new, premium-priced technologies can be adopted, even when they offer clear clinical benefits.

Key Market Segments Shaping Europe’s IVD Landscape

ELISA & CLIA Segment

ELISA (Enzyme-Linked Immunosorbent Assay) and CLIA (Chemiluminescence Immunoassay) technologies form a core part of Europe’s immunoassay market. These methods are widely used for detecting hormones, pathogens, and disease biomarkers, including those related to cancer, HIV, and hepatitis. Their high sensitivity, specificity, and suitability for automation make them essential tools in both routine screening and specialized diagnostics. Europe’s strong laboratory infrastructure continues to support sustained demand for these reliable technologies.

Rapid Test Segment

The rapid test market in Europe has gained strong momentum, driven by the demand for quick results and easier access to diagnostics. Rapid tests are commonly used for infectious diseases, pregnancy testing, glucose monitoring, and drug screening. The pandemic significantly boosted public familiarity with self-testing, and this behavior is now extending into other areas of healthcare. Rapid tests support decentralized care models, reduce pressure on hospitals, and empower patients to take a more active role in managing their health.

Instruments Segment

The instruments segment is growing steadily as hospitals, research centers, and laboratories invest in advanced diagnostic equipment. Key instruments include analyzers for hematology, molecular diagnostics, clinical chemistry, and immunoassays. Automation, robotics, and integration with laboratory information systems are improving workflow efficiency and reducing turnaround times. Public and private investments in modernizing laboratory infrastructure are major growth drivers for this segment.

Infectious Disease Applications

Infectious diseases remain one of the most critical application areas within Europe’s IVD market. With ongoing concerns about global mobility and emerging pathogens, early detection and surveillance are top public health priorities. Molecular diagnostics and antigen-based tests are in high demand for conditions such as influenza, HIV, hepatitis, tuberculosis, and COVID-19. Innovations such as multiplex testing and syndromic panels are further enhancing the speed and accuracy of pathogen identification.

Clinical Chemistry Segment

Clinical chemistry is the backbone of routine diagnostic testing in Europe, covering metabolic panels, liver and kidney function tests, and electrolyte analysis. Automation and system integration have significantly improved efficiency and consistency in this segment. The growing burden of chronic diseases and the emphasis on preventive healthcare continue to drive demand for clinical chemistry diagnostics across the region.

Laboratories as the Core End-User

Laboratories remain the central hub of Europe’s IVD ecosystem. Both public and private labs are increasingly adopting digital and automated platforms to handle rising test volumes, reduce errors, and improve turnaround times. Centralized, high-throughput laboratories are expanding, particularly in urban areas, while collaborations with biotech firms and research institutions continue to fuel innovation.

Country-Level Insights

Germany

Germany leads the European IVD market thanks to its advanced healthcare infrastructure, strong R&D ecosystem, and extensive network of diagnostic laboratories. The country is a hub for innovation, supported by close collaboration between industry and academia. High standards for accuracy and quality drive strong adoption of molecular diagnostics, immunoassays, and automated systems.

France

France’s IVD market benefits from national health programs, large-scale screening initiatives, and a proactive approach to infectious disease control. Demand is particularly strong in molecular diagnostics for oncology and infectious diseases. Increasing automation and digitalization in laboratories are further improving efficiency and service delivery.

United Kingdom

The UK IVD market is dynamic and research-driven, supported by the National Health Service (NHS) and a vibrant biotech sector. Post-pandemic, there is strong emphasis on point-of-care and home-based testing, as well as genetic testing and personalized medicine. Regulatory changes following Brexit are reshaping the market environment, but innovation and investment remain strong.

Netherlands

The Netherlands stands out for its focus on high-throughput, automated diagnostics and digital health solutions. The country’s patient-centered care model supports the growth of home-based testing and advanced laboratory systems. Strong government support for innovation and close ties between academia and industry position the Netherlands as a forward-looking IVD market.

Competitive Landscape

Leading players in the Europe IVD market include Roche Diagnostics, Abbott Diagnostics, Siemens Healthineers, Danaher Corporation, Thermo Fisher Scientific, and Sysmex Corporation. These companies compete across multiple dimensions, including technology innovation, product portfolio breadth, geographic reach, and strategic partnerships. Continuous investment in R&D and portfolio expansion remains critical to maintaining competitive advantage in this rapidly evolving market.

Final Thoughts: A Market Built on Innovation and Necessity

The Europe In-Vitro Diagnostics (IVD) market is on a solid growth trajectory, supported by powerful structural drivers such as aging populations, rising chronic disease burden, technological progress, and strong healthcare systems. While regulatory complexity and cost pressures present challenges, the long-term outlook remains highly positive.

With the market expected to grow from USD 23.35 billion in 2024 to USD 34.47 billion by 2033 at a CAGR of 4.42%, IVD will continue to play a central role in shaping the future of European healthcare. As diagnostics become faster, more accurate, and more accessible, they will not only improve clinical outcomes but also help healthcare systems across Europe become more efficient, preventive, and patient-centered.

About the Creator

Keep reading

More stories from shibansh kumar and writers in Trader and other communities.

Global Millets Market Size and Forecast 2025–2033

Global Millets Market: A New Age for an Ancient Grain The Global Millets Market, valued at USD 11.15 billion in 2024, is projected to reach USD 18.65 billion by 2033, growing at a CAGR of 5.88% from 2025 to 2033. This steady and promising growth is being driven by a powerful mix of rising health awareness, increasing demand for gluten-free diets, and strong government support for sustainable and climate-resilient agriculture.

By shibansh kumara day ago in Trader

Australia Eco Friendly Bricks Market: Sustainable Construction on the Rise

The Australia eco friendly bricks market reached USD 24.0 Million in 2025 and is anticipated to grow to USD 42.6 Million by 2034, exhibiting a compound annual growth rate (CAGR) of 6.56% between 2026 and 2034.

By Amélie Belle4 days ago in Trader

The Light Turns

It's Tuesday 7:13 a.m. A cold and clear November morning awaits Ray on his morning commute. Ray rubs his hands together in the front seat of his Subaru. He turns the air temperature up, but keeps the air on low until the air warms up. He looks at the backup camera screen and reverses the Subaru out of his driveway onto Trimble Road.

By John R. Godwin8 days ago in Fiction

Comments

There are no comments for this story

Be the first to respond and start the conversation.