Colon Screening Market Size and Forecast: A Global Push Toward Early Detection

Why rising colorectal cancer cases, government screening programs, and AI-powered diagnostics are reshaping the global colon screening industry through 2033

Introduction: A Market Built Around Prevention

The global healthcare industry is undergoing a quiet but powerful shift—from treating diseases after they appear to preventing them before they become life-threatening. Few areas reflect this transformation more clearly than the colon screening market. As awareness of colorectal cancer continues to rise, so does the urgency to detect it earlier, treat it faster, and ultimately save more lives.

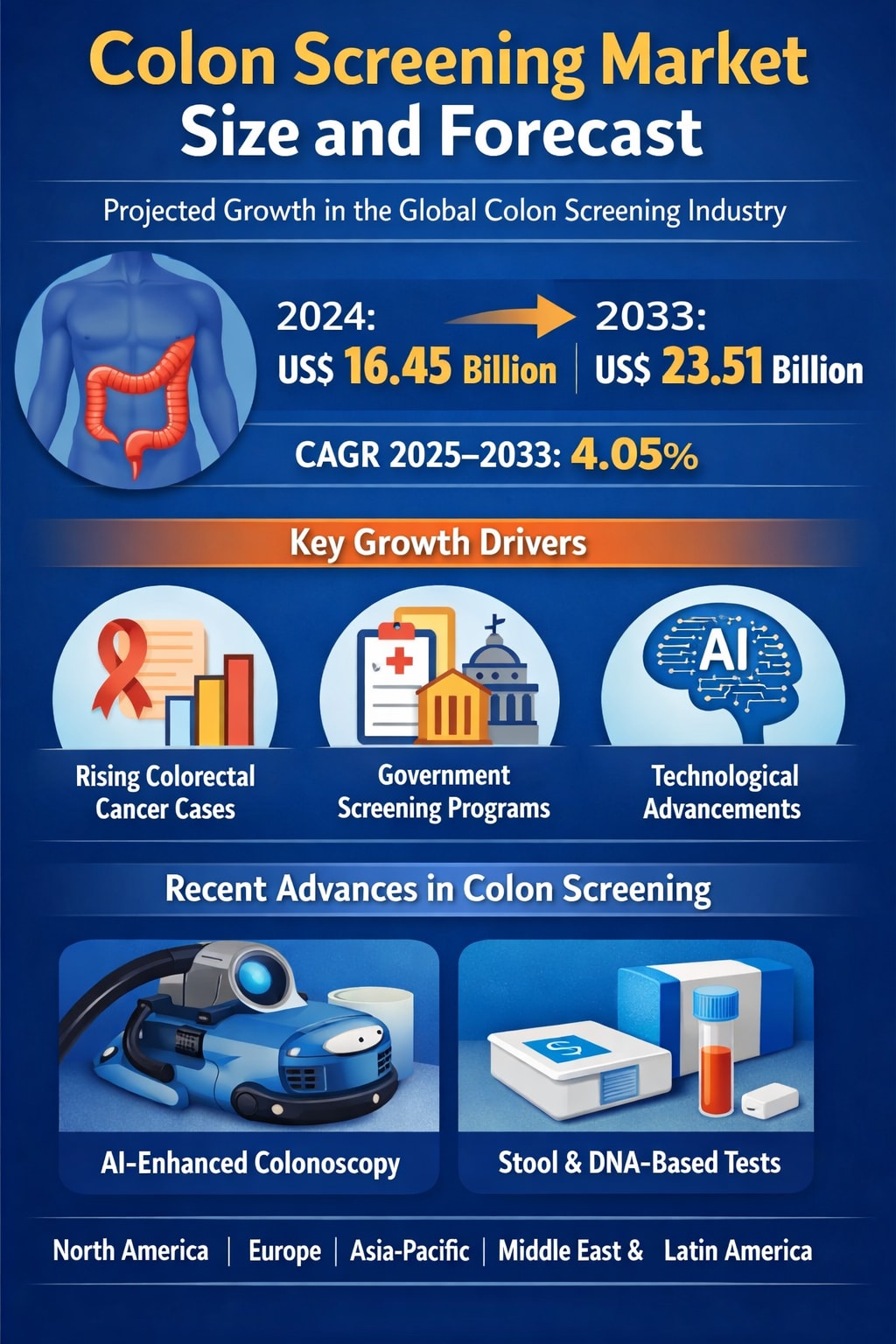

According to Renub Research, the Global Colon Screening Market is expected to reach US$ 23.51 billion by 2033, up from US$ 16.45 billion in 2024, growing at a CAGR of 4.05% from 2025 to 2033. This steady growth is being driven by three major forces: the rising incidence of colorectal cancer, expanding government-backed screening programs, and continuous technological improvements in diagnostic tools.

Colon screening is no longer seen as a niche or optional medical service. It is increasingly becoming a core pillar of preventive healthcare strategies worldwide. From traditional colonoscopies to stool-based tests and emerging AI-assisted imaging systems, the market is evolving rapidly to meet both clinical needs and patient expectations.

Global Colon Screening Industry Overview

The global colon screening industry is expanding at a time when healthcare systems are under pressure to deliver better outcomes at lower long-term costs. Early detection of colorectal cancer plays a crucial role in achieving both goals. Screening methods such as colonoscopy, stool-based tests, and newer molecular and blood-based approaches help identify precancerous polyps and early-stage cancers, significantly improving survival rates.

Technological advancements have made screening more accurate, more accessible, and, in many cases, less invasive. This has helped improve patient compliance, which has historically been one of the biggest challenges in colorectal cancer prevention. At the same time, governments and public health agencies are investing more in awareness campaigns and organized screening programs, further accelerating market growth.

Another important factor shaping the industry is the shift toward value-based healthcare. Detecting cancer early is far less expensive than treating advanced-stage disease, and policymakers are increasingly aligning reimbursement models and guidelines around this reality. As a result, colon screening is moving from being a reactive tool to a proactive, system-wide preventive strategy.

Why Colorectal Cancer Is Driving the Market

One of the strongest forces behind the expansion of the colon screening market is the rising global burden of colorectal cancer. It is currently one of the most commonly diagnosed cancers worldwide and remains a leading cause of cancer-related deaths.

According to the World Cancer Research Fund, an estimated 1.93 million new cases of colorectal cancer were recorded globally in 2022. The World Health Organization has also highlighted that the highest incidence rates are found in regions such as Europe, Australia, and New Zealand, largely due to aging populations, dietary patterns, sedentary lifestyles, and other risk factors.

What makes colorectal cancer particularly suitable for screening is its slow progression. In many cases, the disease develops from benign polyps over several years. This long window creates a critical opportunity for early detection and intervention—if effective screening programs are in place and widely used.

As more countries recognize this, demand for reliable, scalable, and patient-friendly screening solutions continues to rise, directly fueling the growth of the global market.

Technology Is Redefining Colon Screening

The colon screening landscape is no longer limited to traditional methods. One of the most exciting developments in recent years has been the integration of artificial intelligence (AI) into colonoscopy procedures.

AI-powered computer-assisted detection (CAD) systems can analyze real-time video streams during colonoscopies and help physicians identify polyps and other abnormalities that might be missed by the human eye. This not only improves detection rates but also enhances consistency and reduces the risk of human error.

In May 2024, FUJIFILM introduced advanced endoscopic imaging technologies such as CAD EYE and SCALE EYE. CAD EYE is designed to improve the detection of colonic mucosal abnormalities, including adenomas and polyps, while SCALE EYE focuses on enhancing the precision and speed of lesion assessment during endoscopic procedures. These innovations reflect a broader industry trend toward smarter, more data-driven diagnostics.

Beyond AI, improvements in stool-based testing, molecular diagnostics, and imaging technologies are also making screening more accessible and less intimidating for patients—an essential factor in boosting participation rates.

Key Factors Driving Market Growth

1. Increasing Prevalence of Colorectal Cancer

The growing number of colorectal cancer cases worldwide is a primary driver of the colon screening market. Changes in diet, lifestyle, stress levels, and aging populations are all contributing to higher incidence rates. As more cases are diagnosed, especially among younger age groups, the importance of routine screening is becoming more widely recognized.

Healthcare providers and policymakers are placing greater emphasis on early detection, which directly increases demand for screening services, equipment, and diagnostic technologies.

2. Rising Awareness of Early Detection

Public awareness campaigns, advocacy groups, and medical professionals have played a major role in educating people about the life-saving potential of early screening. Today, more individuals understand that colorectal cancer is highly treatable when caught early—and that screening can often detect precancerous conditions before cancer even develops.

This shift in mindset is turning screening into a routine part of preventive healthcare, rather than something people only consider when symptoms appear.

3. Government Initiatives and Screening Guidelines

Many countries have introduced national colorectal cancer screening programs and clear clinical guidelines that recommend routine testing for specific age groups and high-risk populations. These programs often include subsidies or insurance coverage, which significantly improves access and participation rates.

Such policy support not only saves lives but also creates a stable, long-term growth environment for the colon screening market.

Challenges Holding the Market Back

High Costs of Screening Procedures

Despite its benefits, colon screening—especially colonoscopy—can be expensive. Costs related to the procedure itself, preparation, consultations, and follow-up care can deter many individuals, particularly in low- and middle-income regions. Advanced diagnostic options like virtual colonoscopy or stool DNA testing may also be out of reach for large segments of the population.

Insufficient Reimbursement Policies

In many countries, reimbursement for colon screening is inconsistent or limited to specific risk groups. This creates financial barriers for patients and slows the adoption of newer, more patient-friendly technologies. Without broader and more uniform coverage, participation rates may remain below optimal levels, limiting the overall public health impact of screening programs.

Regional Outlook: A Market with Uneven but Expanding Growth

United States

The U.S. colon screening market is growing steadily, supported by strong awareness, established guidelines, and a high prevalence of colorectal cancer. Recommendations to begin screening at earlier ages, combined with the availability of non-invasive tests, are improving participation. An aging population and a strong focus on preventive care continue to drive demand.

Germany

Germany has one of the most structured and effective screening systems in Europe. National guidelines recommend fecal immunochemical testing (FIT) for people aged 50–54 and colonoscopy every ten years for those over 55. More than 60% of eligible individuals participate in screening programs. According to the Robert Koch Institute, colorectal cancer accounts for about one in eight new cancer cases in the country, underlining the importance of continued screening efforts.

China

China’s colon screening market is evolving, with growing awareness and expanding pilot programs. However, overall screening coverage remains relatively low due to resource constraints and uneven healthcare access. Innovations such as fecal DNA methylation assays offer promise by combining high sensitivity with non-invasive testing, which could improve compliance in the future.

Saudi Arabia

In Saudi Arabia, colorectal cancer is among the most common cancers, particularly among men. Despite available screening methods like colonoscopy and FIT, more than 60% of the population has never been screened. Barriers include lack of referrals and fear of procedures. Government guidelines now recommend screening for individuals aged 45 to 75, but broader public awareness and organized national programs are still needed to unlock the market’s full potential.

Recent Developments in the Industry

The pace of innovation and collaboration in the colon screening space is accelerating:

In April 2024, UC Davis Health launched a new digital health initiative aimed at increasing colorectal cancer screening rates, particularly among younger populations where incidence is rising.

In October 2024, the GI Alliance partnered with Medtronic to roll out GI Genius AI Technology across more than 400 locations, enhancing real-time polyp detection during colonoscopies.

These developments highlight how technology and healthcare networks are working together to improve both access and diagnostic quality.

Market Segmentation Snapshot

By Type:

Stool-based

Colonoscopy

Others

By End Use:

Hospitals & Clinics

Clinical Laboratories

Diagnostic Imaging Centers

Others

By Region:

North America (United States, Canada)

Europe (France, Germany, Italy, Spain, UK, Belgium, Netherlands, Turkey)

Asia Pacific (China, Japan, India, Australia, South Korea, Thailand, Malaysia, Indonesia, New Zealand)

Latin America (Brazil, Mexico, Argentina)

Middle East & Africa (South Africa, Saudi Arabia, UAE)

Competitive Landscape

The market features a mix of established medical device giants and innovative technology-driven players. Key companies include:

Olympus Corporation

FUJIFILM Holdings Corporation

Medtronic

Ambu A/S

Bracco

Varay Laborix

EndoFresh (Daichuan Medical)

Baxter (Hillrom & Welch Allyn)

These companies are focusing on product innovation, AI integration, strategic partnerships, and global expansion to strengthen their market positions.

Final Thoughts: A Market with a Clear Preventive Mission

The global colon screening market is not just growing—it is becoming more strategically important to healthcare systems worldwide. With the market projected to rise from US$ 16.45 billion in 2024 to US$ 23.51 billion by 2033, the direction is clear: early detection, smarter diagnostics, and broader access will define the next decade.

While challenges such as cost and reimbursement remain, the combined impact of technology, policy support, and rising public awareness is steadily reshaping how societies approach colorectal cancer prevention. In the long run, the true value of this market will not only be measured in dollars, but in lives saved through timely and effective screening.

About the Creator

Tom Shane

Tom Shane is a content writer specializing in SEO-driven blogs, product descriptions, and thought leadership. He crafts engaging, research-backed content that connects with audiences and drives results.

DC Tax Filing 2026: Step-by-Step Guide to Maximize Your Refund/

DC Tax Filing 2026 is an important task for every Washington, DC resident. Filing taxes correctly not only ensures you avoid penalties but also helps you get the maximum refund possible. Many people miss simple opportunities to increase their refund because they don’t plan or track their expenses properly. They will walk you through a step-by-step approach to DC Tax Filing 2026 that is easy to follow and practical. From organizing documents to claiming deductions and credits, these steps will help you file accurately and confidently.

By John.doe7986 days ago in Trader

Junk Silver in 2026: Is It Still a Good Investment?

Junk silver refers to US currency coins in circulation prior to 1965. They are often considered a great way to get into silver investments. The reason for this is that junk silver coins have a 90% silver composition, which allows them to track the spot price of silver.

By Sound Money6 days ago in Trader

Comments

There are no comments for this story

Be the first to respond and start the conversation.