Clearer Vision, Bigger Market: The Global Intraocular Lens Industry Set for Strong Growth Through 2034

Rising cataract surgeries, premium lens adoption, and expanding eye-care access are reshaping the future of the intraocular lens market worldwide.

Intraocular Lens Market Size and Forecast 2026–2034

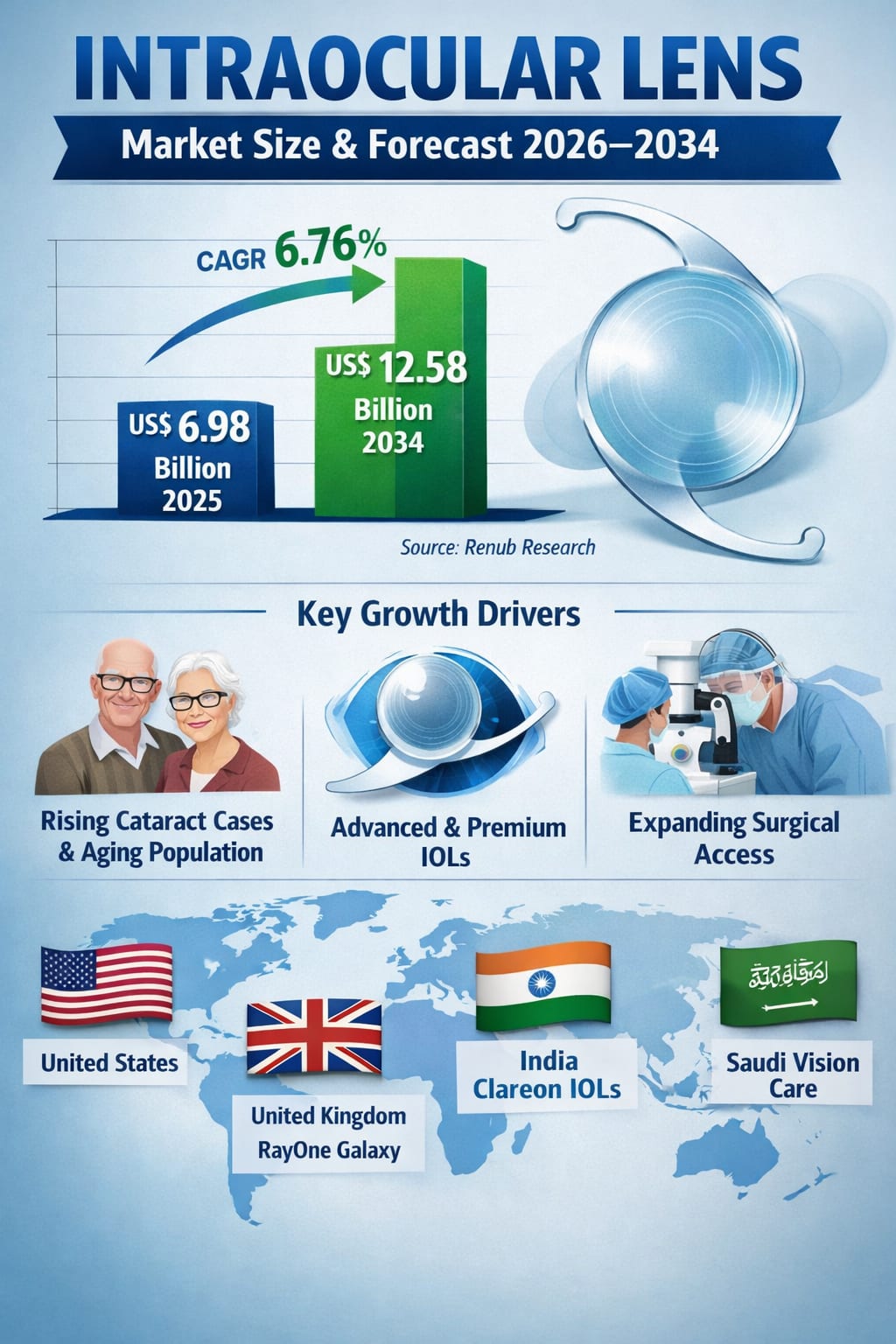

The global Intraocular Lens (IOL) Market is entering a phase of sustained expansion, driven by demographic shifts, rapid technological innovation, and widening access to eye-care services. According to Renub Research, the market was valued at US$ 6.98 billion in 2025 and is projected to reach US$ 12.58 billion by 2034, growing at a compound annual growth rate (CAGR) of 6.76% during the period 2026 to 2034.

This steady growth reflects more than just rising surgical volumes. It highlights a broader transformation in how vision correction is approached globally—moving from basic cataract treatment toward premium, lifestyle-enhancing visual outcomes. As populations age and expectations from eye surgery increase, intraocular lenses are becoming not only a medical necessity but also a quality-of-life investment.

Intraocular Lens Market Outlook

An intraocular lens (IOL) is a small artificial lens implanted in the eye, most commonly during cataract surgery, to replace the eye’s clouded natural lens. By refracting light onto the retina, IOLs restore clear vision and, in many cases, significantly reduce dependence on glasses or contact lenses.

While cataract surgery remains the primary application, IOLs are also used in refractive lens exchange procedures to correct conditions such as myopia, hyperopia, and presbyopia. Over time, the market has evolved far beyond simple monofocal lenses. Today, patients and surgeons can choose from monofocal, multifocal, toric, extended depth-of-focus, and accommodative IOLs, each designed to address specific visual needs.

Globally, demand has risen sharply due to the growing burden of cataracts and other age-related eye conditions. At the same time, advances in surgical techniques and lens materials have made procedures safer, quicker, and more predictable. Rising awareness about eye health, improving healthcare infrastructure in emerging economies, and a growing preference for premium vision correction solutions are all contributing to the market’s expanding footprint.

Key Growth Drivers of the Intraocular Lens Market

Rising Prevalence of Cataracts and an Aging Population

The most powerful driver of the intraocular lens market is the global rise in cataract cases, closely linked to aging populations. As life expectancy increases worldwide, the number of people requiring cataract surgery continues to climb. Cataract surgery is already one of the most commonly performed surgical procedures globally, and its volume is expected to grow further in the coming decade.

Worldwide, billions of people live with some form of vision impairment, and a significant share of this burden is either preventable or treatable. Cataracts remain one of the leading causes of blindness and moderate-to-severe visual impairment, especially among older age groups. The prevalence of cataracts increases sharply with age, making demographic aging a long-term, structural growth driver for the IOL industry.

Developing countries are also expanding access to eye care through government programs and public–private partnerships aimed at reducing preventable blindness. These initiatives are increasing the number of cataract surgeries performed each year, directly boosting demand for intraocular lenses.

Technological Advancements and Premium IOL Adoption

Another major growth engine is innovation in lens design and materials. Modern intraocular lenses now include multifocal, toric, extended depth-of-focus, and accommodative designs, offering better visual outcomes and greater independence from spectacles. These advanced lenses can correct astigmatism, improve near and intermediate vision, and provide smoother visual transitions across distances.

Newer materials are more biocompatible, durable, and optically precise, leading to better long-term outcomes and higher patient satisfaction. Surgeons also benefit from improved predictability and consistency in results, further encouraging the adoption of advanced IOL technologies.

Patients today are far more informed about their options and increasingly willing to pay for premium lenses that enhance their quality of life. For example, in February 2025, Johnson & Johnson launched the TECNIS PureSee™ purely refractive IOL in India, designed to treat presbyopia while offering a visual experience similar to a monofocal lens. Such launches highlight how innovation continues to reshape the competitive landscape.

Increasing Access to Ophthalmic Surgical Care

Improved access to surgical care is another critical factor supporting market growth. Governments and healthcare organizations are investing heavily in healthcare infrastructure, particularly in emerging markets. Charitable organizations and non-profits also play a key role by organizing large-scale cataract surgery programs aimed at underserved populations.

Better training for ophthalmologists, wider availability of modern surgical equipment, and the growth of specialized eye-care centers are all increasing surgical volumes. In October 2024, ZEISS Medical Technology showcased new digital enhancements and surgical solutions at the American Academy of Ophthalmology (AAO) conference, underlining how digital and workflow innovations are helping surgeons deliver more personalized and efficient care.

Challenges Facing the Intraocular Lens Market

High Cost of Premium Intraocular Lenses

Despite strong growth prospects, cost remains a significant barrier, especially for premium IOLs. In many healthcare systems, advanced lenses are only partially reimbursed or not covered at all, forcing patients to pay out of pocket. This limits adoption in price-sensitive markets and among lower-income patient groups, particularly in developing countries.

Post-Surgical Complications and Regulatory Requirements

Although cataract surgery is generally safe, complications such as lens dislocation, glare, halos, or posterior capsule opacification can affect patient satisfaction. Managing these risks requires skilled surgeons and proper patient selection.

In addition, IOL manufacturers must navigate strict regulatory approval processes to demonstrate safety and efficacy, which can increase development costs and slow down product launches.

Segment Insights

Monofocal Intraocular Lens Market

Monofocal IOLs remain the largest and most widely used segment. They provide clear vision at a single focal point—usually distance—and are known for their reliability, affordability, and strong insurance coverage. Their consistent visual outcomes and low risk of visual disturbances make them the preferred choice in high-volume cataract surgeries worldwide, especially in public healthcare systems.

Multifocal Intraocular Lens Market

The multifocal IOL segment is growing rapidly as more patients seek freedom from glasses. These lenses offer vision correction at multiple distances, making them attractive to individuals who want greater convenience after surgery. Although higher costs limit universal adoption, rising awareness and willingness to invest in premium eye care are supporting strong growth in this segment.

Silicone Material Intraocular Lens Market

Silicone IOLs are valued for their flexibility, biocompatibility, and optical performance. Their foldable nature allows for smaller incisions and faster recovery times. While they may not be suitable for all patients—particularly those who may require certain retinal procedures—they continue to play an important role in cataract and refractive lens exchange surgeries.

Polymethyl Methacrylate (PMMA) Intraocular Lens Market

PMMA lenses represent a more traditional and cost-effective option. Although their rigid structure requires larger incisions, they remain widely used in emerging markets due to their affordability, durability, and optical clarity. PMMA lenses are especially common in government-funded programs and mass cataract surgery camps aimed at reducing preventable blindness.

Ambulatory Surgery Centers (ASC) Segment

The shift of cataract surgeries toward ambulatory surgery centers is another notable trend. ASCs offer efficient, high-quality, and cost-effective surgical care with faster patient turnover. Advances in surgical techniques and anesthesia have made it easier to perform cataract procedures in these settings, boosting demand for both standard and premium intraocular lenses.

Regional Market Highlights

United States

The U.S. intraocular lens market is among the largest and most technologically advanced globally. High surgical volumes, strong adoption of premium lenses, and a well-developed healthcare infrastructure support market growth. Favorable reimbursement for standard procedures and increasing out-of-pocket spending for premium options further strengthen demand. In October 2025, the FDA approved BVI’s FineVision HP trifocal IOL, expanding the range of advanced lens choices available to U.S. patients.

United Kingdom

In the UK, the market is driven by an aging population and a well-structured public healthcare system. While cost constraints within the NHS limit widespread use of premium lenses, private healthcare providers are expanding access to advanced options. In August 2024, Rayner announced the upcoming release of the world’s first spiral-shaped AI-designed IOL, RayOne Galaxy & Galaxy Toric, highlighting the UK’s role in innovation.

India

India represents one of the fastest-growing markets due to its large population and high burden of cataract-related vision impairment. Government programs and non-profit initiatives drive high-volume surgeries, with cost-effective monofocal and PMMA lenses dominating. At the same time, urban private hospitals are increasingly adopting foldable and premium IOLs. In March 2024, Alcon launched its Clareon family of IOLs in India, strengthening the premium segment.

Saudi Arabia

Saudi Arabia’s market is expanding steadily, supported by strong healthcare investment, modern hospital infrastructure, and rising awareness of eye health. Increased access to advanced surgical equipment and specialized eye-care centers is boosting adoption of foldable and premium intraocular lenses.

Market Segmentation Overview

By Product:

Monofocal IOL

Multifocal IOL

Toric IOL

Accommodative IOL

By Material:

Polymethyl Methacrylate (PMMA)

Silicone

Hydrophobic & Hydrophilic Acrylic

Other Materials

By End User:

Hospitals

Ambulatory Surgery Centers

Ophthalmology Clinics

Eye Research Institutes

By Geography:

North America (U.S., Canada), Europe (France, Germany, Italy, Spain, UK, Belgium, Netherlands, Turkey), Asia Pacific (China, Japan, India, Australia, South Korea, Thailand, Malaysia, Indonesia, New Zealand), Latin America (Brazil, Mexico, Argentina), Middle East & Africa (South Africa, Saudi Arabia, UAE).

Key Companies Covered

Alcon Inc.

Bausch Health Companies Inc.

Hoya Corporation

Johnson & Johnson

STAAR Surgical Company

Carl Zeiss Meditec AG (Carl-Zeiss-Stiftung)

Novartis AG

Each company is analyzed across five viewpoints: Overview, Key Persons, Recent Developments & Strategies, Product Portfolio, and Financial Insights.

Final Thoughts

The global intraocular lens market is on a clear upward trajectory, fueled by aging populations, rising cataract surgery volumes, and rapid innovation in lens technology. With the market expected to grow from US$ 6.98 billion in 2025 to US$ 12.58 billion by 2034, the industry is set to play an even more critical role in restoring and enhancing vision worldwide.

While cost barriers and regulatory challenges remain, expanding access to eye care and increasing patient demand for premium visual outcomes will continue to reshape the market. In the years ahead, intraocular lenses will not only be about treating cataracts—they will increasingly be about delivering sharper, more personalized vision and improving quality of life for millions across the globe.

About the Creator

Writing About Writing: The Rainbow Trap

The good thing about living in modern times is that LGBTQ representation in media is increasing. Not just in niche and Independant media, either, but also in mainstream media. Books, movies, TV shows, comics... they're finally catching on that LGBTQ+ people form a significant part of their audience, and deserve to see themselves on screen and in fiction, not just as victims in documentaries and true crime shows.

By Natasja Rose3 days ago in Writers

Comments

There are no comments for this story

Be the first to respond and start the conversation.