United States Automotive Aftermarket Industry Size and Forecast 2025–2033

United States Automotive Aftermarket Industry Size and Forecast 2025–2033

United States Automotive Aftermarket Industry

The United States Automotive Aftermarket Industry is expected to reach US$ 191.07 billion by 2033, up from US$ 137.66 billion in 2024, growing at a CAGR of 3.71% during 2025–2033. Demand for customization, the rapid expansion of e-commerce, rising vehicle ownership, and the increasing average age of vehicles are collectively lowering the cost and increasing the accessibility of parts for maintenance, repair, and performance upgrades nationwide. These forces are reshaping how Americans care for, personalize, and extend the life of their vehicles—positioning the aftermarket as one of the most resilient segments of the broader automotive economy.

United States Automotive Aftermarket Industry Overview

The automotive aftermarket is the secondary market that supports vehicles after their initial sale by the original equipment manufacturer (OEM). It encompasses the production, distribution, retailing, and installation of parts, accessories, equipment, and services used for maintenance, repair, replacement, and enhancement. This includes everything from routine items such as tires, batteries, filters, and brake components to advanced electronics, lighting, exhaust systems, turbochargers, and aesthetic upgrades.

In the United States, the aftermarket plays a pivotal role in vehicle longevity, affordability, and consumer choice. For vehicles beyond warranty coverage, it provides cost-effective alternatives to OEM parts while fostering competition and innovation. It serves both professional repair networks and a robust community of do-it-yourself (DIY) enthusiasts. Increasingly, it also integrates digital diagnostics, telematics, and software-enabled service solutions that improve accuracy, speed, and transparency.

With the average vehicle age now exceeding 12 years, demand for replacement parts and professional repair services remains structurally strong. At the same time, the cultural shift toward vehicle personalization and the convenience of online parts marketplaces are expanding the customer base and lowering friction in purchasing. Coupled with rising disposable incomes and a sustainability mindset that favors repair over replacement, the U.S. automotive aftermarket continues to expand as a critical pillar of the mobility ecosystem.

Growth Drivers for the United States Automotive Aftermarket Industry

1) Aging Vehicle Fleet

One of the most powerful and enduring growth drivers is the aging profile of America’s vehicle parc. As consumers keep cars longer—often due to the high cost of new vehicles and economic uncertainty—maintenance cycles lengthen and intensify. Older vehicles require more frequent service to maintain safety, reliability, and performance, sustaining demand for core categories such as tires, brakes, batteries, filters, suspension components, and engine parts.

This dynamic supports a wide spectrum of businesses: independent repair shops, national service chains, parts distributors, and retailers. Importantly, prolonged ownership encourages preventive maintenance and component replacement rather than full vehicle replacement, delivering steady, repeat demand. The result is long-term market stability and predictable revenue streams across both passenger and light commercial segments.

2) Digitalization and E-Commerce Expansion

The aftermarket has undergone a structural transformation through digital catalogs, mobile apps, and online marketplaces. Consumers can now identify compatible parts, compare prices, read reviews, and arrange installation from home. For businesses, e-commerce unlocks broader geographic reach, improved inventory visibility, and data-driven logistics.

Service providers are also adopting software-based maintenance tools and advanced diagnostics, reducing misdiagnosis, cutting turnaround times, and improving customer satisfaction. Digitalization enhances transparency and trust—two attributes that historically constrained aftermarket purchases. As platforms mature and last-mile delivery improves, online channels will continue to capture share, particularly among younger buyers and DIY customers.

3) Customization and Lifestyle Influence

For many Americans, vehicles are expressions of identity. This has elevated customization—from aesthetic upgrades like lighting, wraps, wheels, and interior trims to performance modifications such as exhaust systems, suspension kits, and turbochargers—into a major growth engine.

Automotive culture amplified by social media, online forums, and motorsports communities fuels experimentation and innovation. Younger drivers, in particular, invest in personalization that reflects lifestyle trends. In response, manufacturers and retailers continuously introduce new designs, materials, and technology-enabled accessories. This blend of creativity and engineering sustains demand across niche categories and supports premium pricing for differentiated products.

Challenges in the United States Automotive Aftermarket Industry

1) Labor Shortages and Skill Gaps

As vehicles become more software-driven and electrified, the need for highly skilled technicians has intensified. Diagnostics, advanced electronics, and emerging EV systems require specialized training that many shops struggle to staff. A declining pipeline of young workers entering technical trades exacerbates the issue.

The consequences include longer service times, higher labor costs, and constrained capacity, particularly for small and independent operators. While certification programs, apprenticeships, and digital tools can help bridge the gap, they require sustained investment. Addressing workforce development is critical to maintaining service quality and competitiveness.

2) Supply Chain and Inventory Pressures

The aftermarket continues to face supply chain volatility—from raw material constraints and transportation delays to reliance on international suppliers. These disruptions create unpredictable availability and pricing for key components. Inflationary pressures and rising logistics costs further compress margins.

Companies are responding with localized sourcing, diversified supplier networks, and digital inventory management, but implementation takes time. Ensuring consistent product availability while protecting profitability remains a central operational challenge in an increasingly competitive environment.

State-Level Dynamics: Where Growth Takes Shape

California Automotive Aftermarket Industry

California is among the largest and most dynamic aftermarket markets in the U.S. Its massive vehicle base, strict emissions standards, and technology-forward consumers drive demand for eco-friendly replacement parts, hybrid and EV services, and digital diagnostics. A strong car culture in cities such as Los Angeles and San Francisco sustains customization, performance tuning, and aesthetic upgrades. The rapid adoption of electric vehicles also encourages innovation in battery systems, thermal management, and charging infrastructure. With environmental policy and consumer sophistication reinforcing one another, California remains a leading hub for aftermarket innovation.

Texas Automotive Aftermarket Industry

Texas combines scale, practicality, and enthusiasm. High vehicle ownership, an extensive road network, and an economy rooted in logistics, energy, and agriculture generate robust demand for fleet maintenance and heavy-duty components. Pickup trucks and SUVs dominate, boosting sales of performance parts, off-road accessories, and durability-focused components. Major distribution centers in Dallas-Fort Worth and Houston enhance supply-chain efficiency. A strong DIY culture further supports retail channels, making Texas a cornerstone of national aftermarket growth.

New York Automotive Aftermarket Industry

New York’s aftermarket is shaped by urban density, harsh winters, and an aging vehicle base. Seasonal services—tire changes, battery replacements, corrosion protection—drive recurring demand. While New York City’s public transit reduces per-capita car ownership, suburban and upstate regions generate significant volume. Environmental regulations accelerate the adoption of eco-friendly parts and hybrid service offerings. The state’s unique blend of weather challenges and regulatory rigor ensures steady, adaptive growth.

Florida Automotive Aftermarket Industry

Florida benefits from year-round driving conditions, a tourism-driven economy, and rapid population growth. The warm climate increases demand for cooling systems, tires, and cosmetic enhancements, while coastal conditions boost sales of anti-corrosion treatments and detailing services. A growing retiree population tends to keep vehicles longer, supporting replacement part demand. Vibrant car culture in Miami and Orlando sustains customization and performance trends. Florida remains one of the fastest-growing regional markets.

Recent Developments in the United States Automotive Aftermarket Industry

June 2025: PHINIA Inc. acquired Electromagnet Invest AB for US$ 47 million, strengthening its electromagnetic components portfolio and enhancing innovation capacity.

November 2024: Standard Motor Products completed the US$ 390 million acquisition of Nissens Automotive, significantly expanding its thermal-management solutions.

August 2023: ZF Aftermarket added 74 new listings to its TRW and SACHS brands across the U.S. and Canada, broadening coverage for vehicles in operation.

April 2023: Robert Bosch, LLC introduced 52 new parts for nearly 22 million vehicles, spanning braking, pumps, ignition, sensors, and injectors.

April 2022: 3M acquired the technological assets of LeanTec, advancing its “Connected Bodyshop” initiative with data-driven inventory and workflow solutions.

These moves highlight a sector focused on portfolio expansion, technology integration, and scale, as leading players invest to meet evolving vehicle complexity and customer expectations.

United States Automotive Aftermarket Industry Segmentation

By Type

Tire

Battery

Brake parts

Filters

Body parts

Lighting & Electronic components

Wheels

Exhaust components

Turbochargers

Others

By Distribution Channel

Retail

W&D (Wholesale & Distribution)

By Service Channel

DIY (Do-It-Yourself)

DIFM (Do-It-For-Me)

OE (Original Equipment)

By Certification

Genuine

Certified Parts

Uncertified Parts

By State (29 Viewpoints)

California, Texas, New York, Florida, Illinois, Pennsylvania, Ohio, Georgia, New Jersey, Washington, North Carolina, Massachusetts, Virginia, Michigan, Maryland, Colorado, Tennessee, Indiana, Arizona, Minnesota, Wisconsin, Missouri, Connecticut, South Carolina, Oregon, Louisiana, Alabama, Kentucky, and Rest of United States.

Competitive Landscape and Key Players

All major companies are evaluated across five viewpoints—Company Overview, Key Persons, Recent Developments & Strategies, SWOT Analysis, and Sales Analysis—providing a comprehensive picture of competitive positioning.

Key Players Include:

3M Company; Continental AG; Cooper Tire & Rubber Company; Delphi Automotive PLC; Denso Corporation; Federal-Mogul Corporation; HELLA KGaA Hueck & Co.; Robert Bosch GmbH; Valeo Group; ZF Friedrichshafen AG.

The competitive environment is defined by brand trust, distribution reach, innovation capacity, and data-enabled operations. Leaders are expanding through acquisitions, introducing advanced product lines, and embedding digital tools across the value chain to improve speed, accuracy, and customer experience.

Outlook: What Will Shape the Next Decade?

Electrification and Advanced Electronics: As EVs and hybrids scale, the aftermarket will diversify into battery management, thermal systems, sensors, and software-driven diagnostics.

Omnichannel Retail: Seamless integration of online discovery, rapid fulfillment, and local installation will become standard.

Sustainability Through Repair: Environmental priorities will favor repair, remanufacturing, and eco-friendly components, reinforcing the aftermarket’s relevance.

Workforce Modernization: Investment in training, certification, and AI-assisted diagnostics will be essential to offset labor shortages.

Personalization at Scale: Customization will remain a premium growth segment, blending design, performance, and digital experiences.

Final Thoughts

From US$ 137.66 billion in 2024 to a projected US$ 191.07 billion by 2033, the United States automotive aftermarket is on a steady, innovation-driven ascent. Its growth is anchored in structural realities—an aging vehicle fleet and sustained mobility needs—while being amplified by digital commerce, customization culture, and a pragmatic shift toward repair and longevity.

Despite challenges in labor and supply chains, the industry’s adaptability is evident in strategic acquisitions, technology adoption, and evolving service models. As electrification accelerates and consumer expectations continue to rise, the aftermarket will not merely support the automotive sector—it will help define how Americans maintain, personalize, and sustain their vehicles in the decades ahead.

About the Creator

Renub Research

Renub Research is a Market Research and Consulting Company. We have more than 15 years of experience especially in international Business-to-Business Researches, Surveys and Consulting. Call Us : +1-478-202-3244

Keep reading

More stories from Renub Research and writers in The Swamp and other communities.

United States Tire Market Size and Forecast 2025–2033

United States Tire Market Overview The United States Tires Market is expected to grow extensively, from US$ 42.11 billion in 2024 to US$ 55.14 billion by 2033, expanding at a Compound Annual Growth Rate (CAGR) of 3.04% between 2025 and 2033, according to Renub Research. This steady expansion reflects the central role tires play in the nation’s vast transportation ecosystem—supporting personal mobility, logistics, public transit, and emerging electric vehicle (EV) infrastructure.

By Renub Researchabout 21 hours ago in The Swamp

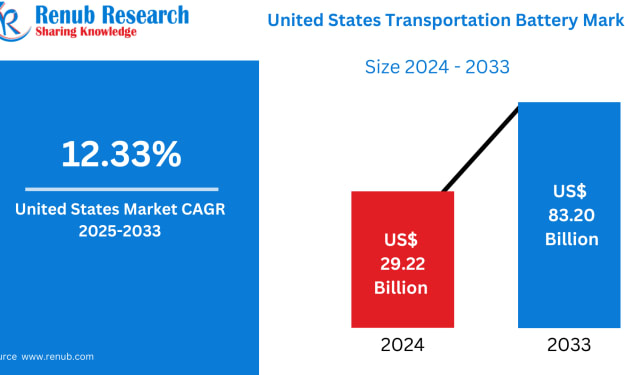

United States Transportation Battery Market Size and Forecast 2025–2033

United States Transportation Battery Market Outlook The United States Transportation Battery Market is undergoing a rapid transformation as the country accelerates its transition toward cleaner, more sustainable mobility solutions. According to Renub Research, the market is expected to grow from US$ 29.22 billion in 2024 to US$ 83.20 billion by 2033, expanding at a robust compound annual growth rate (CAGR) of 12.33% during 2025–2033.

By Janine Root 4 days ago in The Swamp

Comments

There are no comments for this story

Be the first to respond and start the conversation.