Australia Commercial Vehicle Market Size and Forecast 2025–2033

How Infrastructure Growth, Electrification, and Booming Logistics Are Steering Australia’s Commercial Vehicle Future

The Australia Commercial Vehicle Market is positioned for substantial expansion over the next decade. According to Renub Research, the market is projected to rise from US$ 15.79 billion in 2024 to US$ 24.14 billion by 2033, growing at a CAGR of 4.83% during 2025–2033. This momentum is largely attributed to rising freight movement, reinforced infrastructure development, technological transformation, and a gradual shift toward electric and low-emission fleets.

Australia's vast geography, dispersed population centers, booming e-commerce industry, and heavy dependence on mining and construction collectively sustain strong demand for commercial vehicles. From heavy-duty trucks powering large-scale mining operations to light commercial vans supporting fast-expanding last-mile delivery, commercial vehicles remain a backbone of the Australian economy.

Australia Commercial Vehicle Market Overview

Commercial vehicles serve vital functions across Australia’s economic landscape. These include trucks, vans, buses, pick-up trucks, and utility vehicles used for logistics, construction, public transport, agriculture, and mining. The importance of these vehicles is deeply entrenched across the country's transport networks as road freight remains the primary mode of inland cargo movement.

Australia’s logistics ecosystem leans heavily on long-haul trucks that traverse desert routes, regional highways, and cross-border corridors. Meanwhile, light commercial vehicles (LCVs) play a pivotal role in dense urban centers, supporting courier services, grocery delivery, and e-commerce order fulfillment.

Economic growth, population expansion in major cities, expanding retail channels, and government-led infrastructure projects are stimulating market demand. Additionally, the country’s gradual transition toward electric commercial vehicles (ECVs)—driven by sustainability targets and fleet cost-optimization strategies—is reshaping investment priorities across industries.

As businesses push toward higher productivity and operational efficiency, commercial vehicles are increasingly being equipped with telematics, ADAS safety systems, fuel-efficient engines, and alternative propulsion technologies.

Key Growth Drivers in the Australia Commercial Vehicle Market

1. Infrastructure Development and Urban Expansion

Government investment in highways, bridges, rail corridors, and urban logistics networks is significantly stimulating demand for commercial vehicles. Large-scale developments such as the Inland Rail project, Western Sydney Airport infrastructure, and city-expansion initiatives in regions like Melbourne and Brisbane are expanding the requirement for construction trucks, heavy-duty haulers, and specialized machinery.

Australia currently hosts:

5 cities with populations exceeding 1 million

14 cities with 100,000–1 million inhabitants

375 cities with 10,000–100,000 residents

This geographic distribution increases reliance on transport networks and fuels consistent demand for both heavy trucks and light vans. As urban density grows and inter-city commerce rises, fleet operators are expanding and modernizing their vehicle portfolios.

2. E-commerce and Last-Mile Delivery Boom

The accelerated shift toward online shopping has dramatically increased parcel volumes, compelling logistics companies to invest heavily in medium-duty trucks and LCVs. The post-pandemic surge in courier shipments has reshaped delivery expectations—retailers now prioritize same-day and next-day delivery.

This has made delivery vans, pick-up trucks, and small cargo vehicles indispensable for:

Courier companies

Retail distribution centers

Food delivery services

Postal operations

The LCV market is witnessing sustained growth, supported by demand for fuel-efficient models and electric delivery fleets for urban routes.

3. Shift Toward Green Mobility and Fleet Electrification

Sustainability pressures, national emissions-reduction goals, and corporate ESG commitments are accelerating Australia's adoption of electric commercial vehicles.

Government incentives—tax rebates, stamp duty exemptions, and procurement mandates—are enabling this transition. Fleet operators are increasingly exploring battery electric vehicles (BEVs) and alternative fuel vehicles such as CNG, LPG, and hydrogen fuel cell electric vehicles (FCEVs).

A notable development took place in May 2025, when Linfox, a leading logistics company, placed Australia’s largest-ever order of 30 heavy-duty electric trucks from Volvo. This signals rising confidence in heavy electric transport solutions for long-haul and metro applications.

The green commercial vehicle segment is expected to accelerate as:

Charging/refueling infrastructure expands

Battery costs decline

Urban emissions regulations tighten

Key Challenges in the Australia Commercial Vehicle Market

1. High Operational and Ownership Costs

Fleet operators face elevated costs across:

Fuel expenditure

Maintenance and repairs

Insurance premiums

Skilled driver salaries

Australia’s extensive distances and challenging terrain contribute to faster wear and tear. High upfront prices for technologically advanced or electric commercial vehicles remain a financial barrier, particularly for SMEs.

2. Limited Alternative Fuel Infrastructure

While the nation is progressing toward low-emission mobility, infrastructure gaps continue to slow adoption.

Challenges include:

Sparse charging stations in rural and remote regions

Limited CNG and LPG refueling networks

Slow rollout of hydrogen facilities

Range anxiety and operational constraints inhibit widespread transition from diesel fleets to greener technologies.

Segment Analysis of the Australia Commercial Vehicle Market

Australia Heavy-duty Commercial Truck Market

Heavy-duty trucks are indispensable for industries such as mining, agriculture, and inter-city freight. Demand is particularly strong in New South Wales, Queensland, and Western Australia—regions central to mining and agricultural exports.

Key trends include:

Adoption of cleaner diesel engines

Telematics integration for real-time monitoring

Gradual trials of electric and hydrogen-powered heavy-duty trucks

Australia BEV Commercial Vehicle Market

Australia’s electric commercial vehicle sector is small but rapidly emerging.

Key adoption areas include:

Urban logistics

Public transport

Council fleet operations

With rising corporate sustainability demands and reduced long-term operating costs, more fleet operators are piloting BEVs. Local councils and corporations are investing in electric buses, vans, and pick-up trucks to cut emissions and improve efficiency. Market expansion is expected to accelerate as incentives strengthen and charging networks expand.

Australia CNG Commercial Vehicle Market

CNG vehicles present a cleaner and more cost-effective alternative to diesel, especially within metropolitan public transport and waste collection sectors. Cities like Sydney and Brisbane have adopted CNG buses, though broader adoption is constrained by:

Limited refueling points

Sparse supply infrastructure

Despite challenges, sustainability mandates will support moderate growth.

Australia LPG Commercial Vehicle Market

LPG remains popular among:

Taxi fleets

Courier services

Budget-focused fleet operators

While LPG offers cost advantages and lower emissions compared to petrol/diesel, the segment faces decline as electric mobility gains momentum. A modernized LPG ecosystem is needed to maintain competitiveness.

Australia Logistics Commercial Vehicle Market

Logistics fuels the nation’s economy, relying heavily on commercial vehicles for domestic and international freight operations. The industry continues to adopt:

LCVs for warehouse distribution

Medium-duty trucks for metro logistics

Heavy-duty trucks for inter-state movement

Technology, including fleet telematics and route optimization, is boosting efficiency. However, driver shortages and fluctuating fuel prices remain pressing challenges. As urban congestion rises, electric delivery vans are expected to become more prevalent.

Australia Mining & Construction Commercial Vehicle Market

Mining and construction represent two of Australia’s largest vehicle-consuming industries. Demand includes:

Heavy-duty haulage trucks

Off-road mining trucks

Workforce transportation buses

Utility trucks

Western Australia and Queensland remain key regions. With safety and emissions evolving, companies are shifting toward fuel-efficient vehicles and autonomous mining trucks.

In 2024, BHP initiated a 12-month trial of a battery-electric Toyota HiLux as part of efforts to electrify its 5,000-vehicle fleet and reduce emissions by 30% by 2030.

Commercial Vehicle Market by State

New South Wales (NSW)

NSW represents the largest and most diversified market. Sydney’s dense urban logistics network and rural agricultural operations create dual demand for vans and heavy-duty trucks. The state is also a frontrunner in electric bus procurement and low-emission mobility transitions.

Victoria

Victoria, home to Melbourne, benefits from strong manufacturing, retail, and logistics sectors. The Port of Melbourne—one of Australia’s busiest trade gateways—drives substantial demand for heavy trucks.

A key market development includes:

United H2 Limited’s planned acquisition of GoZero Group (2025) for USD 248 million, strengthening Australia’s electric and hydrogen commercial vehicle capabilities.

South Australia

While smaller, South Australia’s market is steadily growing, driven by agriculture, mining, and renewable energy initiatives. Adelaide’s urban areas are adopting electric delivery vans and buses, while rural sectors depend on heavy-duty trucks.

Market Segmentation

By Vehicle Type

Heavy-duty Commercial Trucks

Light Commercial Pick-up Trucks

Light Commercial Vans

Medium-duty Commercial Trucks

By Propulsion Type

Hybrid & Electric (BEV, FCEV, HEV, PHEV)

Internal Combustion Engines (ICE)

Diesel

Gasoline

CNG

LPG

By End User

Industrial

Mining & Construction

Logistics

Passenger Transportation

Others

Top States

New South Wales, Victoria, Queensland, Western Australia, South Australia, ACT, Tasmania, Northern Territory

Key Companies Covered (5-Point View per Company)

AB Volvo

Ford Motor Company

General Motors Company

Hyundai Motor Company

Mahindra & Mahindra Ltd.

Mercedes-Benz Group AG

Mitsubishi Motors Corporation

Robert Bosch GmbH

Tata Motors Limited

Toyota Motor Corporation

(Each analyzed by Overview, Key Person, Recent Developments, SWOT Analysis, Revenue Analysis.)

Final Thoughts

Australia’s Commercial Vehicle Market is heading into a decade of pivotal transformation. Infrastructure expansion, e-commerce growth, the mining and construction resurgence, and a decisive shift toward sustainability are reshaping demand across all vehicle categories. While challenges persist—high operational costs and infrastructure limitations—the momentum behind fleet modernization and electrification is unmistakable.

As investments increase and technology evolves, Australia’s commercial vehicle landscape is set to become cleaner, smarter, and more efficient. For fleet operators, manufacturers, and policymakers, the years leading up to 2033 represent a period of unprecedented opportunity.

About the Creator

Ben Tom

Ben Tom is a seasoned content writer with 12+ years of experience creating SEO-friendly blogs, web copy, and marketing content that boosts visibility, engages audiences, and drives results.

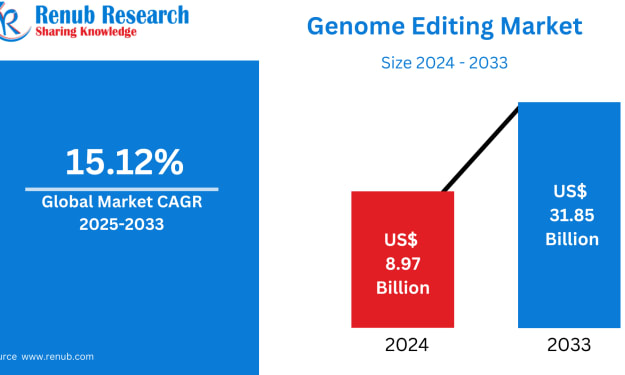

Genome Editing Market Size and Forecast 2025–2033

Introduction: A New Era of Genetic Precision The global biotechnology landscape is undergoing one of the most transformative shifts in modern science, driven by rapid advances in genome editing technologies. Once confined to academic laboratories and experimental research, gene-editing tools have now become central to innovation in healthcare, agriculture, and industrial biotechnology. From treating genetic disorders at their molecular roots to engineering climate-resilient crops and improving industrial bio-manufacturing, genome editing is redefining what is scientifically and commercially possible.

By Renub Research6 days ago in The Swamp

Comments

There are no comments for this story

Be the first to respond and start the conversation.