United States Wound Care Market Size and Forecast 2025–2033

Advanced Therapies, Aging Demographics, and Home Healthcare Trends Shape a Rapidly Evolving Market

United States Wound Care Market Outlook

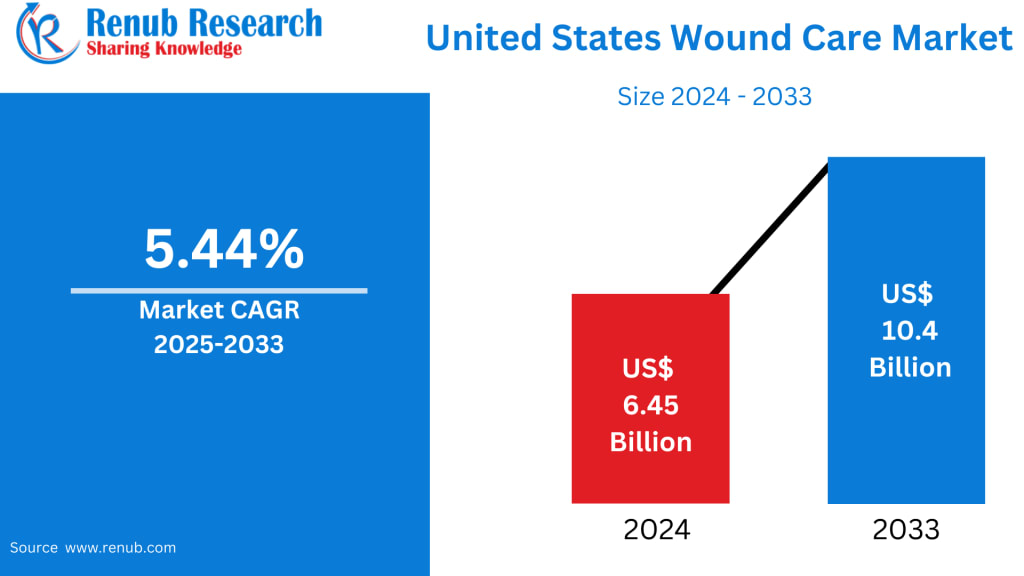

The United States wound care market is entering a sustained phase of expansion as healthcare systems respond to the growing burden of chronic diseases, an aging population, and increasing surgical procedures nationwide. According to Renub Research, the market is expected to grow from US$ 6.45 billion in 2024 to US$ 10.4 billion by 2033, registering a compound annual growth rate (CAGR) of 5.44% from 2025 to 2033.

This steady growth reflects rising adoption of advanced wound care solutions, increasing awareness of infection prevention, and continuous innovation in wound healing technologies. From hospitals and specialty clinics to home healthcare environments, wound care has become an essential component of modern medical practice in the United States.

United States Wound Care Industry Overview

The U.S. wound care industry plays a critical role in healthcare delivery by addressing acute, chronic, and surgical wounds through a wide range of treatment solutions. These include advanced wound dressings, biologics, negative pressure wound therapy (NPWT), and wound therapy devices designed to accelerate healing while reducing infection risks.

Healthcare providers are increasingly shifting away from traditional wound care methods toward advanced and bioactive therapies that offer improved outcomes and faster recovery. This transition is driven by rising clinical evidence, patient demand for effective treatments, and the need to minimize hospital stays and complications.

Demographic trends are also reshaping the market. An aging population, coupled with increasing rates of diabetes, obesity, and cardiovascular disorders, has significantly raised the incidence of chronic wounds such as diabetic foot ulcers, pressure ulcers, and venous leg ulcers. These conditions require long-term management, making wound care a recurring and high-value segment of healthcare expenditure.

According to the Centers for Disease Control and Prevention, nearly 37.3 million Americans live with diabetes, while 96 million adults have prediabetes, highlighting a major patient pool that is particularly vulnerable to chronic wound complications. These factors are expected to support continued market growth throughout the forecast period.

Technological Advancements Driving Market Evolution

Technological innovation remains one of the strongest catalysts in the U.S. wound care market. Manufacturers are introducing advanced foam dressings, antimicrobial materials, bioengineered skin substitutes, and negative pressure wound therapy devices to address complex wound conditions.

In January 2023, ConvaTec Group PLC launched ConvaFoam, a next-generation foam dressing range designed to improve patient comfort while addressing clinical performance requirements. Similarly, MediWound Ltd. received approval from the U.S. Food and Drug Administration in December 2022 for NexoBrid, a biologic treatment used to remove eschar in severe burn wounds.

Beyond product launches, significant investments in research and development by academic institutions and medical device manufacturers are accelerating innovation. Emerging technologies such as smart wound dressings, capable of monitoring healing progress and delivering medications in response to wound conditions, are gradually reshaping the future of wound management.

Key Factors Driving the United States Wound Care Market Growth

Growing Chronic Illnesses and Aging Population

One of the primary growth drivers of the U.S. wound care market is the increasing prevalence of chronic illnesses alongside a rapidly aging population. Conditions such as diabetes, vascular disease, and obesity significantly raise the risk of chronic wounds, which often require prolonged and specialized treatment.

Older adults are particularly susceptible to pressure ulcers and slow-healing wounds, prompting healthcare providers to prioritize advanced wound care solutions that reduce infection risk and improve quality of life. As life expectancy continues to rise, demand for effective wound management is expected to increase across hospitals, long-term care facilities, and home care settings.

Technological Developments and Product Innovation

Innovation is redefining wound care practices in the United States. Advanced dressings made from hydrocolloids, hydrogels, alginates, and antimicrobial materials are gaining preference over traditional gauze due to their superior healing performance.

Manufacturers are also focusing on sustainability and biocompatibility, aligning product development with environmental and patient safety goals. These advancements not only enhance clinical outcomes but also support broader adoption among healthcare professionals seeking evidence-based solutions.

Expansion of Outpatient and Home Healthcare Services

The shift toward outpatient care and home healthcare has significantly influenced the U.S. wound care market. Rising healthcare costs and hospital capacity constraints have encouraged treatment outside traditional inpatient settings.

Portable wound therapy devices, telemedicine-enabled monitoring, and easy-to-use advanced dressings allow patients to manage chronic wounds at home under professional supervision. This approach improves convenience, reduces hospital readmissions, and lowers overall treatment costs. Growing insurance coverage for home healthcare services further strengthens this trend.

Challenges in the United States Wound Care Market

High Cost of Advanced Wound Care Products

Despite their clinical benefits, advanced wound care products often come at a premium cost. Negative pressure wound therapy systems, bioengineered dressings, and biologics may be inaccessible to patients without adequate insurance coverage.

This cost barrier can limit adoption in smaller healthcare facilities and rural areas, creating disparities in care. Manufacturers face increasing pressure to balance innovation with affordability to expand market reach.

Regulatory and Reimbursement Barriers

Strict regulatory requirements and inconsistent reimbursement policies pose additional challenges. While regulation ensures patient safety, lengthy approval processes can delay product launches and increase development costs.

Variations in reimbursement policies across states and payers may discourage healthcare providers from adopting newer therapies. Improving reimbursement clarity and streamlining regulatory pathways remain critical to sustaining market growth.

United States Wound Care Market Overview by States

California Wound Care Market

California leads in innovation and adoption of advanced wound care technologies. Its robust healthcare infrastructure, large patient base, and strong research ecosystem support rapid integration of modern wound management solutions across hospitals and home care settings.

Texas Wound Care Market

Texas benefits from expanding healthcare facilities and a diverse population. Demand spans both advanced therapies in urban centers and cost-effective solutions in rural areas, creating balanced growth opportunities.

New York Wound Care Market

New York’s advanced hospitals and academic institutions drive strong demand for high-quality wound care solutions. The state’s focus on clinical excellence and patient outcomes accelerates adoption of advanced therapies.

Florida Wound Care Market

Florida’s aging population significantly boosts demand for chronic wound management. The market emphasizes accessible, effective, and home-based wound care solutions tailored to elderly patients.

Market Segmentation Overview

By Wound Type

Advanced Wound Dressings

Traditional Wound Care Products

Negative Pressure Wound Therapy

Bioactive

Others

By Product Type

Foam

Antimicrobial

Alginate

Hydrocolloid

Hydrogel

Film

Traditional Gauze

Traditional Non-Adherent

Others

By Application

Chronic Wounds

Acute Wounds

By End User

Hospitals & Clinics

Long-Term Care Facilities

Home Care Settings

By States

Includes California, Texas, New York, Florida, Illinois, Pennsylvania, Ohio, Georgia, New Jersey, Washington, and the Rest of the United States.

Competitive Landscape and Company Analysis

The U.S. wound care market is moderately consolidated, with global and regional players competing on innovation, product effectiveness, and pricing strategies. Key companies covered include:

Mölnlycke Healthcare

Smith & Nephew

Ethicon Inc (Johnson & Johnson)

Coloplast Corp

Derma Sciences Inc. (Integra LifeSciences)

These companies focus on product innovation, strategic partnerships, and geographic expansion to strengthen their market positions.

Final Thoughts

The United States wound care market is poised for sustained growth through 2033, supported by demographic shifts, technological advancements, and evolving care delivery models. As chronic diseases continue to rise and healthcare increasingly moves toward outpatient and home-based settings, demand for advanced, cost-effective wound care solutions will remain strong.

While challenges such as high product costs and reimbursement complexities persist, continued innovation and supportive healthcare policies are expected to unlock new opportunities. With strong participation from established players and ongoing research investments, the U.S. wound care industry is well-positioned to improve patient outcomes while delivering long-term market value.

About the Creator

Renub Research

Renub Research is a Market Research and Consulting Company. We have more than 15 years of experience especially in international Business-to-Business Researches, Surveys and Consulting. Call Us : +1-478-202-3244

Keep reading

More stories from Renub Research and writers in Longevity and other communities.

United States Radiation Dose Management Market Size and Forecast 2025–2033

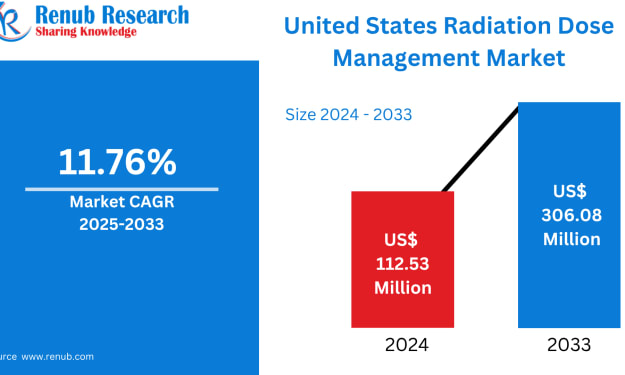

United States Radiation Dose Management Market Overview The United States Radiation Dose Management Market is undergoing rapid expansion as patient safety becomes a central pillar of modern healthcare delivery. According to Renub Research, the market is expected to reach US$ 306.08 million by 2033, growing from US$ 112.53 million in 2024, at a strong CAGR of 11.76% from 2025 to 2033. This growth trajectory highlights the increasing importance of monitoring, analyzing, and optimizing radiation exposure across diagnostic and interventional imaging procedures.

By Renub Research16 days ago in Longevity

Day 4 of Quitting

If this is how sobriety feels, maybe it’s better to go through life a little buzzed… this, along with other hits like, I want to kill myself, I wish I was dead, and I’m going to throw myself off a bridge have been the only thoughts on rotation these past few days. I promise myself that if, in a month, I still feel like this (‘this’ meaning despondent, full of rage, and simultaneously numb) I can go back to smoking. Until mid-February though? Nicotine is off the table.

By sleepy drafts4 days ago in Longevity

How Natural Feeling Light Helped Me Move Through the Day With Ease

For a long time, I thought daily fatigue was just part of modern life. You push through the morning, slow down after lunch, fight restlessness in the evening, and hope sleep resets everything overnight. I assumed that was normal. What I did not question was the environment guiding me through those hours.

By illumipure6 days ago in Longevity

Comments

There are no comments for this story

Be the first to respond and start the conversation.