Saudi Arabia Generic Drugs Market Size & Forecast 2025–2033

Affordable Medicines Powering the Kingdom’s Healthcare Transformation

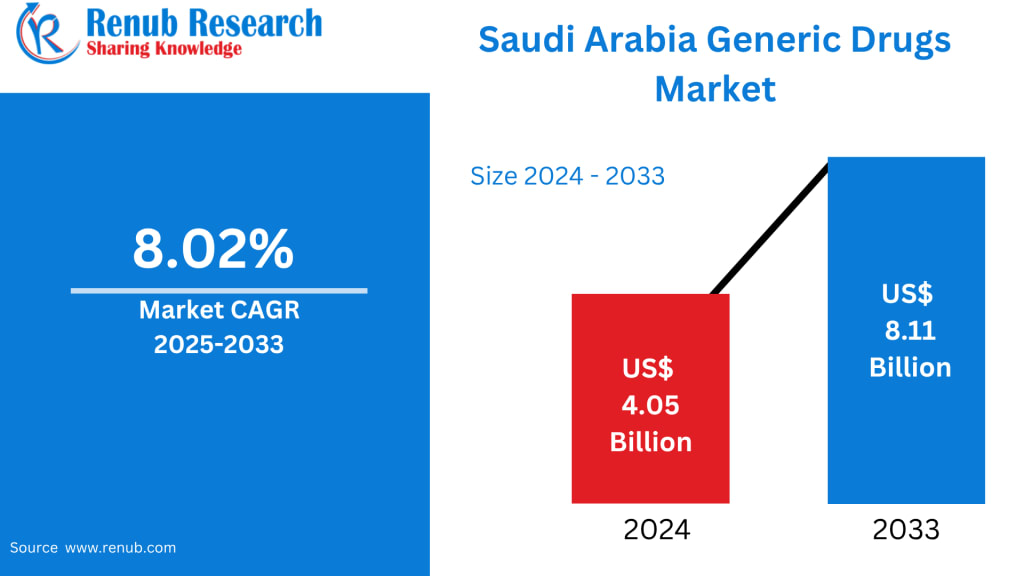

Market Snapshot (Renub Research)

The Saudi Arabia Generic Drugs Market is projected to expand from US$ 4.05 billion in 2024 to US$ 8.11 billion by 2033, registering a strong CAGR of 8.02% during 2025–2033. This growth trajectory is driven by rising healthcare demand, government-led cost-containment policies, increasing chronic disease prevalence, and sustained support for local pharmaceutical manufacturing.

Saudi Arabia Generic Drugs Market Overview

Generic drugs are bioequivalent versions of branded medicines, offering the same active ingredients, dosage strength, safety, quality, and therapeutic efficacy, but at significantly lower prices. These medicines undergo stringent bioequivalence testing and regulatory approval before entering the market, ensuring patient confidence and clinical effectiveness.

In Saudi Arabia, generic drugs are becoming a cornerstone of the healthcare system. Policymakers and healthcare providers increasingly recognize generics as an effective solution to reduce pharmaceutical expenditure, expand patient access, and ensure long-term system sustainability. Regulatory facilitation by the Saudi Food and Drug Authority (SFDA) has accelerated generic approvals, encouraging both domestic and international manufacturers to strengthen their presence in the Kingdom.

Combined with population growth, rising healthcare awareness, and the government’s focus on preventive care, generics are steadily gaining acceptance among physicians, pharmacists, insurers, and patients alike.

Key Growth Drivers

Government Support and Cost-Containment Initiatives

Saudi Arabia’s healthcare policy strongly favors affordable treatment options. The government actively promotes generic drug adoption across public hospitals and insurance programs to curb escalating healthcare costs. Streamlined approval pathways, pricing regulations, and incentives for domestic production have significantly boosted market momentum.

A notable regulatory step was the SFDA’s draft initiative titled “Procedure to Deal with Patents When Registering Generic Products”, released for public consultation in 2022. This framework clarified patent-related pathways for generics, reducing uncertainty for manufacturers and enhancing market confidence. Such policy clarity continues to attract foreign pharmaceutical investments into the Kingdom.

Rising Burden of Chronic Diseases

Saudi Arabia faces one of the highest chronic disease burdens in the Middle East. Conditions such as diabetes mellitus, hypertension, cardiovascular disorders, obesity, and respiratory diseases require lifelong medication, significantly increasing treatment costs.

Generic drugs offer a sustainable solution for managing chronic illnesses without compromising quality. As physicians and patients seek cost-effective long-term therapies, generics are becoming the default choice. The growing elderly population and sedentary lifestyles further reinforce consistent demand across therapeutic categories.

Expansion of Local Manufacturing Capacity

Under Saudi Vision 2030, the Kingdom is aggressively expanding its domestic pharmaceutical manufacturing base. Investments in advanced production facilities, technology transfer agreements, and public–private partnerships are strengthening local capabilities.

In January 2024, Saudi Arabia announced a national biotechnology strategy aimed at positioning the country as a global biotech hub within 16 years. This initiative supports not only innovative drugs but also advanced generics and biosimilars, reducing import dependence and improving supply security.

Market Challenges

Public Perception and Brand Loyalty

Despite clinical equivalence, branded medicines still enjoy strong trust among segments of the population. Cultural perceptions, physician prescribing habits, and historical reliance on multinational brands can slow generic adoption. Overcoming this challenge requires continued education campaigns, physician engagement, and transparent quality assurance.

Regulatory and Quality Compliance Complexity

While approvals have become faster, generic manufacturers must still meet rigorous requirements for bioequivalence, Good Manufacturing Practices (GMP), and post-market surveillance. For smaller or new entrants, these compliance costs can be substantial. Maintaining consistent quality and preventing counterfeit medicines also remain ongoing operational challenges.

Market Segmentation Insights

Saudi Arabia Simple Generic Drugs Market

Simple generics—medicines with uncomplicated formulations—dominate the Saudi market. Widely used for pain management, infections, hypertension, and common ailments, they are easy to manufacture and face fewer regulatory complexities. Government price controls and widespread use in public hospitals ensure high volumes, making this segment an attractive entry point for manufacturers.

Saudi Arabia Specialty Generic Drugs Market

Specialty generics address complex and high-cost therapies, including oncology, autoimmune diseases, and rare disorders. As Saudi Arabia seeks to reduce reliance on expensive imported biologics, investment in specialty generics is rising. Though development costs are higher, these products offer substantial savings for healthcare systems and insurers, driving long-term growth.

Saudi Arabia Oral Generic Drugs Market

Oral dosage forms—tablets, capsules, and syrups—remain the most preferred due to ease of administration and patient compliance. Strong manufacturing infrastructure and widespread outpatient usage ensure oral generics maintain the largest market share, particularly for chronic disease management.

Saudi Arabia Respiratory Generic Drugs Market

Environmental factors such as dust exposure and smoking contribute to high asthma and COPD prevalence. Demand for affordable inhalers, MDIs, DPIs, and nebulized formulations is steadily increasing. Although device complexity poses regulatory challenges, supportive reimbursement policies and public health initiatives continue to expand access.

Saudi Arabia Oncology Generic Drugs Market

Cancer treatment costs place heavy pressure on healthcare budgets. Oncology generics, including biosimilars, are gaining traction as hospitals integrate them into treatment protocols. Government funding, insurance coverage, and early diagnosis programs support adoption, enabling equitable cancer care across income groups.

Saudi Arabia Online Generic Drugs Market

Digital healthcare transformation has fueled rapid growth in online pharmacies and e-prescription platforms. Accelerated by COVID-19, consumers now benefit from convenience, price transparency, and home delivery. High smartphone penetration and tech-savvy urban populations in Riyadh and Jeddah are key demand drivers.

Regional Market Analysis

Western Saudi Arabia

Cities such as Jeddah, Mecca, and Medina form a major consumption hub due to dense populations, advanced healthcare infrastructure, and pilgrimage-related healthcare demand. Public and private hospitals actively support generic usage, aligning with national affordability goals.

Eastern Saudi Arabia

The Eastern region, including Dammam and Khobar, benefits from strong logistics infrastructure and expanding healthcare facilities. Rising insurance coverage and chronic disease prevalence are accelerating generic drug adoption across both public and private sectors.

Market Segmentation Summary

By Type

Simple Generics

Specialty Generics

Biosimilars

By Route of Administration

Oral

Injections

By Therapeutic Area

Infectious Diseases

Respiratory

Musculoskeletal

Oncology

CNS

Cardiovascular

Others

By Distribution Channel

Online Pharmacies

Retail Pharmacies

Hospital Pharmacies

By Region

Northern & Central

Western

Eastern

Southern

Competitive Landscape & Key Players

The Saudi generic drugs market is moderately consolidated, with global and regional leaders competing on quality, pricing, and local partnerships. Each company is analyzed across five viewpoints: Overview, Key Person, Recent Developments, SWOT Analysis, and Revenue Analysis.

Major Companies Operating in Saudi Arabia

Teva Pharmaceutical Industries Ltd.

Viatris Inc.

Sandoz Group AG

Sun Pharmaceutical Industries Ltd.

Cipla Ltd.

Aurobindo Pharma Ltd.

Lupin Ltd.

Hikma Pharmaceuticals PLC

STADA Arzneimittel AG

Dr. Reddy’s Laboratories Ltd.

Final Thoughts

The Saudi Arabia Generic Drugs Market is entering a decisive growth phase. With strong government backing, rising chronic disease prevalence, expanding local manufacturing, and accelerating digital healthcare adoption, generics are becoming indispensable to the Kingdom’s healthcare future.

As Vision 2030 continues to reshape the pharmaceutical ecosystem, generic drugs will play a critical role in improving access, controlling costs, and ensuring long-term sustainability. For manufacturers, investors, and healthcare stakeholders, Saudi Arabia represents one of the most promising generic drug markets in the Middle East through 2033.

About the Creator

Marthan Sir

Educator with 30+ years of teaching experience | Passionate about sharing knowledge, life lessons & insights | Writing to inspire, inform, and empower readers.

Keep reading

More stories from Marthan Sir and writers in Longevity and other communities.

Global Health and Wellness Market Size & Forecast 2025–2033

Global Health and Wellness Market Outlook The Global Health and Wellness Market is entering a powerful growth phase as consumers worldwide redefine health as a long-term lifestyle commitment rather than reactive medical care. According to Renub Research, the market is projected to expand from US$ 3,520.00 billion in 2024 to US$ 4,818.30 billion by 2033, registering a CAGR of 3.55% from 2025 to 2033.

By Marthan Sir20 days ago in Longevity

Day 4 of Quitting

If this is how sobriety feels, maybe it’s better to go through life a little buzzed… this, along with other hits like, I want to kill myself, I wish I was dead, and I’m going to throw myself off a bridge have been the only thoughts on rotation these past few days. I promise myself that if, in a month, I still feel like this (‘this’ meaning despondent, full of rage, and simultaneously numb) I can go back to smoking. Until mid-February though? Nicotine is off the table.

By sleepy drafts4 days ago in Longevity

Seven Health Tips To Promote Longevity

I love chatting with older folks who look better than younger folks and have more energy than younger folks. They're magnetic because they're doing life differently. Most people age out of healthy habits, physiques, and energy. But a small sector of folks defy the odds and maintain pristine health as they age. Here are some tips I received from some older folks who looked better than most of the people at the gym:

By Destiny S. Harris5 days ago in Longevity

Comments

There are no comments for this story

Be the first to respond and start the conversation.