Europe Breast Cancer Screening Market Set for Strong Growth Through 2033

Rising awareness, AI-powered imaging, and government-backed screening programs are reshaping early cancer detection across Europe

Europe Breast Cancer Screening Market Overview

Breast cancer screening plays a crucial role in modern healthcare by enabling early detection of cancer, often before symptoms appear. The most commonly used screening methods include mammography, ultrasound, and magnetic resonance imaging (MRI), with genetic testing increasingly supporting risk-based screening strategies for high-risk populations. Early diagnosis significantly improves survival rates, reduces treatment costs, and allows patients to access less invasive treatment options.

Across Europe, breast cancer screening has become a central pillar of public health policy. Many countries operate nationwide screening programs that invite women—typically between the ages of 50 and 74—for regular mammograms. These initiatives are supported by rising public awareness, improving healthcare infrastructure, and rapid technological advancements in medical imaging.

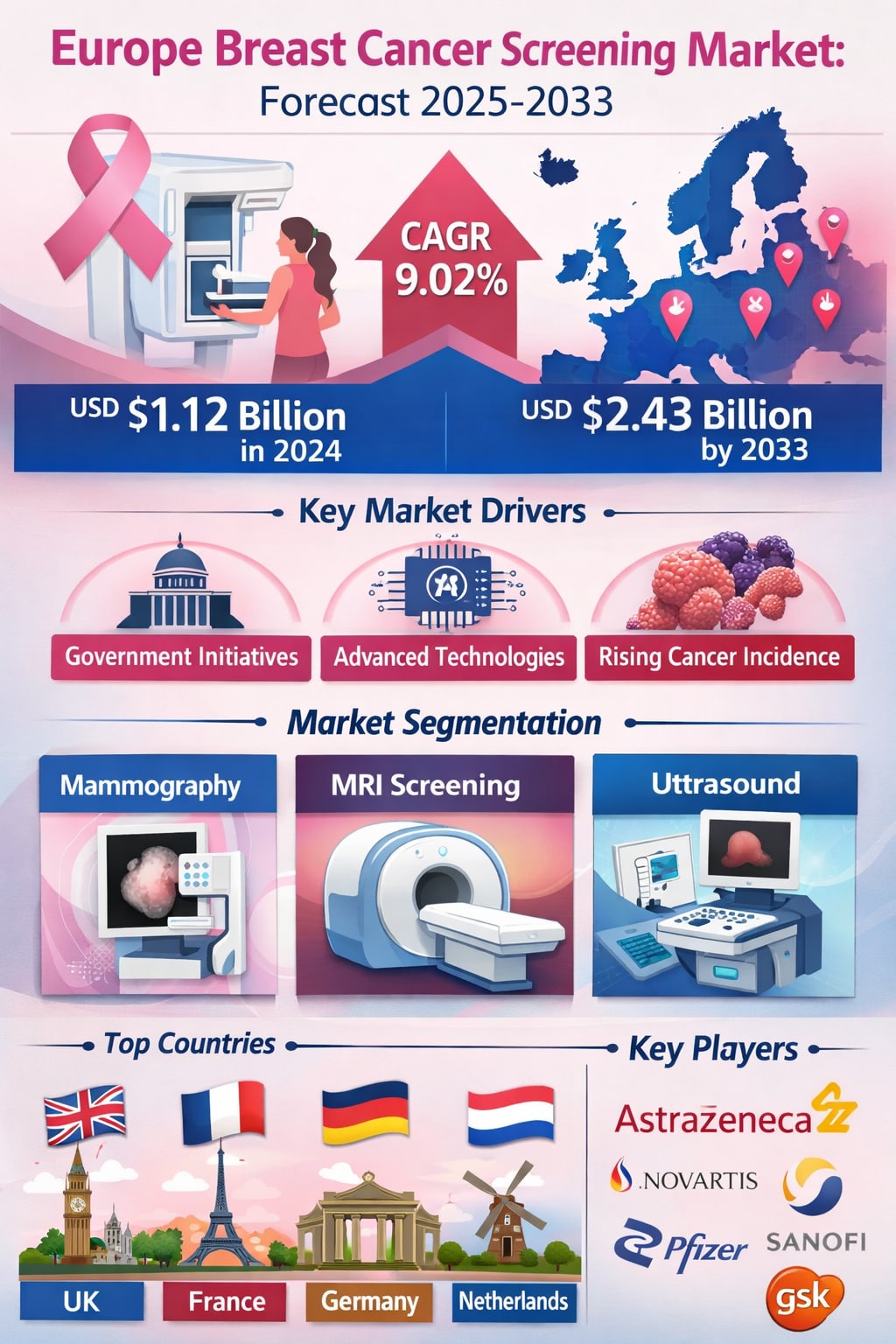

According to Renub Research, the Europe Breast Cancer Screening Market was valued at USD 1.12 billion in 2024 and is predicted to reach USD 2.43 billion by 2033, growing at a CAGR of 9.02% from 2025 to 2033. This strong growth trajectory reflects the increasing prevalence of breast cancer, wider access to screening services, and the integration of advanced technologies such as artificial intelligence (AI) and 3D imaging into routine diagnostics.

As Europe continues to prioritize preventive healthcare, the demand for accurate, accessible, and efficient breast cancer screening solutions is expected to rise steadily over the coming decade.

What Is Driving the Market Forward?

Government Initiatives and Awareness Programs

One of the most powerful growth engines for the European breast cancer screening market is strong government support. Countries such as the United Kingdom, Germany, France, and the Netherlands operate well-established, publicly funded screening programs that offer free or subsidized mammograms to eligible women. These programs not only increase participation rates but also normalize preventive screening as a routine part of women’s healthcare.

At the European Union level, the EU Beating Cancer Plan has further strengthened political commitment to early detection. Updated screening guidelines adopted in 2022 aim to ensure that 90% of eligible populations across the EU have access to screening for breast, colorectal, and cervical cancer. This coordinated approach is expected to significantly boost screening volumes and, in turn, market demand for imaging systems, diagnostic software, and related services.

Public awareness campaigns led by healthcare authorities, NGOs, and patient advocacy groups also play a major role. As more women become aware of the benefits of early detection, participation in screening programs continues to rise—directly supporting market expansion.

Advancements in Screening Technologies

Technology is transforming the way breast cancer is detected and diagnosed. Traditional film-based mammography has largely been replaced by digital mammography, which offers higher image quality, faster processing, and easier data storage. More recently, 3D tomosynthesis has gained traction, allowing radiologists to examine breast tissue layer by layer and improving detection rates, especially in women with dense breast tissue.

Artificial intelligence is another game-changer. AI-powered imaging systems can assist radiologists by highlighting suspicious areas, reducing human error, and improving both sensitivity and specificity. These tools not only enhance diagnostic accuracy but also help address workforce shortages by streamlining image interpretation.

In March 2025, GE HealthCare launched Invenia™ Automated Breast Ultrasound (ABUS) Premium, a 3D ultrasound system featuring advanced AI designed to improve supplemental screening for women with dense breasts. Innovations like these are accelerating the adoption of advanced screening technologies across European hospitals and diagnostic centers, further fueling market growth.

Rising Breast Cancer Incidence Rates

Breast cancer remains the most common cancer among women in Europe. According to data from the WHO Europe region, an estimated 604,900 new cases were reported in 2022. Factors such as an aging population, lifestyle changes, and genetic predispositions continue to push incidence rates higher.

This growing disease burden underscores the importance of early detection. As healthcare systems seek to reduce mortality rates and long-term treatment costs, investments in screening infrastructure and programs are increasing. The result is sustained demand for mammography units, MRI scanners, ultrasound systems, and associated diagnostic solutions across the region.

Key Challenges Facing the Market

High Cost of Advanced Screening Technologies

Despite impressive technological progress, cost remains a significant barrier. MRI systems and 3D mammography units are expensive to purchase, install, and maintain. Not all healthcare facilities—especially in underfunded or resource-constrained regions—can afford these advanced tools.

This creates an uneven landscape where patients in wealthier or urban areas have better access to state-of-the-art screening, while those in less-developed regions may rely on older technologies. Although public funding and EU-level initiatives are helping to close this gap, affordability remains a key challenge for the market.

Screening Coverage Gaps and Accessibility Issues

While Western and Northern Europe generally enjoy high screening coverage, parts of Eastern and Southern Europe still face accessibility issues. Rural and remote areas often lack sufficient diagnostic centers, trained personnel, or modern equipment.

Mobile screening units and tele-radiology solutions are emerging as practical ways to extend coverage, but disparities persist. Bridging these gaps will be essential not only for public health outcomes but also for unlocking the full growth potential of the European breast cancer screening market.

Europe Breast Cancer Screening Population Market

The expanding population of women eligible for screening is a major growth driver. As life expectancy increases and preventive healthcare becomes a policy priority, more women are being included in routine screening programs.

There is also a growing focus on risk-based and personalized screening. Women with a family history of breast cancer or genetic mutations such as BRCA1 and BRCA2 are increasingly being offered earlier and more frequent screening using advanced modalities like MRI and ultrasound. This shift toward personalized prevention is expected to further boost demand for diverse screening technologies across Europe.

Segment Insights

Europe Breast Cancer Mammography Screening Market

Mammography remains the cornerstone of breast cancer screening in Europe. It is widely regarded as the gold standard for population-based screening and is the backbone of most national programs.

The market for mammography screening continues to expand due to government investments, equipment upgrades, and the transition to digital and 3D systems. These newer technologies offer better image quality and higher detection rates, driving higher adoption across hospitals and diagnostic centers.

Europe Breast Cancer MRI Screening Market

MRI is primarily used for high-risk patients and women with dense breast tissue, where mammography alone may be less effective. Its superior sensitivity makes it a valuable tool for early detection, particularly in complex cases.

However, the high cost and limited availability of MRI scanners restrict widespread use. As a result, MRI screening is more common in private healthcare settings or specialized centers. Even so, demand is steadily increasing as clinical guidelines increasingly recognize the value of MRI in targeted screening strategies.

Europe Breast Cancer Ultrasound Screening Market

Ultrasound is widely used as a complementary tool to mammography, especially for women with dense breasts. The introduction of Automated Breast Ultrasound Systems (ABUS) has improved consistency, reduced operator dependence, and enhanced diagnostic accuracy.

Ultrasound is also more affordable and accessible than MRI, making it an attractive option for expanding screening coverage. Its growing integration into routine screening protocols is contributing significantly to overall market growth.

Country-Wise Market Highlights

Germany

Germany operates one of the most comprehensive breast cancer screening programs in Europe, offering nationwide mammography screening for women aged 50–69 through statutory health insurance. The country is also at the forefront of adopting AI-driven diagnostics. In February 2023, deep-tech startup Vara appointed renowned radiologist Professor Katja Pinker-Domenig as lead medical advisor, signaling Germany’s strong push toward smarter, more accessible screening solutions.

France

France provides free mammography every two years for women aged 50–74, supported by a strong public healthcare system focused on early detection. The country is actively integrating AI and digital imaging into screening workflows. In March 2024, Lunit announced agreements to provide AI-powered radiology solutions for breast cancer detection, further strengthening France’s position in advanced screening technologies.

United Kingdom

The UK’s NHS Breast Screening Programme is one of the largest in Europe, offering free mammograms to women aged 50–70. The UK is also a leader in evaluating AI for large-scale screening. In February 2025, the government launched a major trial involving nearly 700,000 participants across 30 sites to assess how AI can improve early detection accuracy and efficiency.

Netherlands

The Netherlands boasts one of the highest participation rates in Europe, supported by government-funded programs for women aged 50–75 and extensive use of mobile screening units. In October 2023, Agendia NV announced that MammaPrint® was approved for inclusion in the national health insurance package, marking a major step forward in personalized breast cancer care.

Market Segmentation Overview

By Application:

Mammography Screening

MRI Screening

Ultrasound Screening

By Population:

Mammography Screening Population

MRI & Ultrasound Screening Population

By Country:

United Kingdom

France

Germany

Italy

Spain

Switzerland

Norway

Netherlands

Competitive Landscape

The European breast cancer screening ecosystem includes major pharmaceutical and healthcare companies that contribute through diagnostics, imaging technologies, and oncology solutions. Key players covered in the market include:

AstraZeneca

Novartis

Sanofi

Pfizer

Bayer AG

GlaxoSmithKline plc

These companies are actively investing in research, partnerships, and technology development to strengthen their positions in the broader oncology and diagnostics landscape.

Final Thoughts

The Europe Breast Cancer Screening Market is entering a phase of strong and sustained growth. With the market expected to rise from USD 1.12 billion in 2024 to USD 2.43 billion by 2033 at a CAGR of 9.02%, the outlook reflects more than just financial expansion—it signals a fundamental shift toward preventive, technology-driven healthcare.

Government initiatives, rising awareness, and rapid advances in AI-powered imaging are transforming how breast cancer is detected and managed across the continent. While challenges such as cost barriers and access gaps remain, ongoing policy support and innovation are steadily closing these divides.

In the coming decade, Europe’s commitment to early detection, personalized screening, and digital health solutions will not only drive market growth but also save countless lives—making breast cancer screening one of the most impactful segments of the region’s healthcare landscape.

About the Creator

FridaBaby Faces Backlash Over Alleged Sexualized Marketing of Infant Products

The baby-care brand FridaBaby, known for products such as the NoseFrida nasal aspirator and infant thermometers, is facing a surge of online backlash following the resurfacing of old marketing materials featuring suggestive and sexualized language. Social media users have widely circulated screenshots of posts and product packaging, criticizing the brand for content deemed inappropriate for items designed for infants.

By Story Prism2 days ago in Longevity

Comments

There are no comments for this story

Be the first to respond and start the conversation.