Local vs Global Players: Competitive Dynamics in Europe LED Lighting Market

The immediate future is defined by a clash between rising energy costs and supply chain volatility.

The European lighting industry currently navigates one of its most significant transformative periods since the invention of the electric bulb. The recent EU-wide ban on fluorescent lighting has not just opened a door; it has completely blown the roof off the market. Consequently, the Local vs Global players: competitive dynamics in Europe LED lighting market are no longer defined solely by who can manufacture the cheapest bulb. Instead, the battleground has shifted to intelligent ecosystems, sustainability compliance, and supply chain resilience.

As of 2024, the market has reached a substantial valuation of US24.7 billion. However, the path forward is not linear. European giants like Signify and Osramnow pivot towards "Light as a Service"(LaaS). Simultaneously, global challengers from Asia aggressively acquire heritage brands to gain a regional foothold. Therefore, the lines between "local" and "global" blur more every day. With the market projected to grow at a robust CAGR of 8.87%, understanding who holds the power is essential for investors and stakeholders.

What Do the Numbers Say About the Market's Future?

The market is entering a "Golden Age" of high growth, driven by legislation and technological replacement.

According to the latest data from the IMARC Group, the forecast remains aggressive. They predict the market will more than double in value over the next decade. A CAGR of 8.87% is exceptionally high for a mature industrial sector. This signals that the industry is experiencing a structural revolution rather than a passing trend.

Furthermore, the segmentation data reveals a crucial shift. While "Retrofit" projects (replacing old bulbs with LEDs) provided the initial revenue boom, the future lies in "New Installation." This segment includes integrated smart lighting systems built directly into the infrastructure of smart cities and modern homes. Geographically, Germany remains the dominant force. It acts as both the primary manufacturing hub and the largest consumer base for high-end industrial lighting solutions.

How Are EU Regulations Acting as a Defensive Moat?

Stringent environmental policies effectively filter out low-quality global competition, which favors local players.

The European Union’s Eco-design for Sustainable Products Regulation (ESPR) and the RoHS (Restriction of Hazardous Substances) directive have set the highest barriers to entry in the world. These laws create a "regulatory moat" for local European manufacturers. While global players often compete on volume and price, they frequently struggle to meet the EU's rigorous requirements for "repairability" and energy efficiency labeling.

For instance, the "Right to Repair" initiative mandates that lighting fixtures must allow for component replacement rather than requiring total disposal. European brands have baked sustainability into their corporate DNA. They use this as a competitive advantage. They market not just a light, but a compliant, future-proof asset that aligns with the EU's Green Deal. This strategy effectively pushes non-compliant, cheap imports out of the professional and industrial sectors.

What Is the "Smart" Strategy of Local European Giants?

Local players are abandoning the "commodity" war to dominate the high-margin "Internet of Things" (IoT) sector.

Companies like Signify (Philips) and Zumtobel realized years ago that they cannot beat Asian manufacturing on price alone. Their answer? Stop selling bulbs and start selling systems. They now pioneer concepts like Human Centric Lighting (HCL). These systems adjust color temperature to match circadian rhythms, which boosts productivity in offices and schools.

Moreover, by integrating Li-Fi (internet connectivity through light waves) and sensor-based data collection, they transform lighting fixtures into intelligent data nodes. In this context, the physical LED serves merely as a Trojan horse for selling software and service contracts. This is a domain where European data privacy and security standards give local players a massive trust advantage over international competitors.

How Are Global Players Disrupting the Supply Chain?

Global challengers currently counter with a strategy of "Glocalization" - merging global scale with local identity.

The dichotomy of "East vs. West" becomes increasingly complex. Major Asian manufacturers, such as MLS Co., Ltd. (China), have moved beyond simple exporting. The acquisition of LEDVANCE (formerly Osram’s general lighting business) by MLS stands as the prime example of this hybrid model.

By combining the cost-efficiency of Chinese manufacturing with the trusted brand heritage and distribution network of a German giant, they created a formidable competitor. These global players are particularly dominant in the Residential application segment. As IMARC notes, this segment holds the largest market share. In the residential space, price sensitivity often outweighs the need for advanced IoT features, giving the volume advantage to global manufacturers.

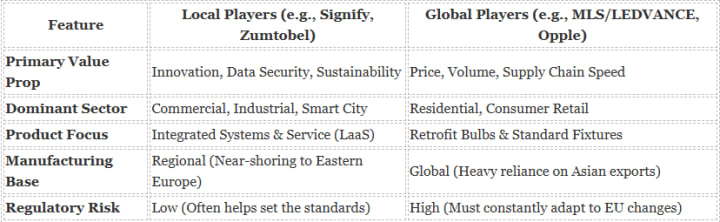

Local Heritage vs. Global Scale: Who Wins Where?

To understand the landscape, we must recognize that different players dominate different battlefields.

The following comparison highlights where local European entities excel versus their global counterparts:

What Technological Frontiers Are Defining the Competition?

Beyond standard illumination, the battle for technical superiority drives the market forward.

Local players currently invest heavily in Micro-LED technology and Horticultural Lighting. As Europe focuses on food security and urban farming, specialized LEDs for indoor greenhouses represent a booming niche. European research institutes and companies lead the charge in optimizing light spectra for plant growth, creating a high-barrier market segment that global commodity players find hard to penetrate.

Additionally, the push for Smart City integration requires lighting that interacts with traffic systems and emergency services. This requires a level of software integration and security clearance that typically excludes non-European vendors from critical infrastructure projects.

What Are the Key Challenges for Brands in 2025?

The immediate future is defined by a clash between rising energy costs and supply chain volatility.

For local European manufacturers, the crisis is internal. Soaring energy prices in Europe make domestic manufacturing expensive, which squeezes margins. Consequently, they must justify higher prices through superior technology and durability.

For global players, the challenge is logistical. Disruptions in global shipping lanes (such as the Red Sea crisis) and increasing freight costs threaten the "low cost" model that their dominance relies on. Furthermore, as the IMARC segmentation shows a shift toward "LED Fixtures" over simple "Lamps," global players must upgrade their capabilities. Shipping bulky, complex units requires a more sophisticated logistics network than shipping small, lightweight bulbs.

Frequently Asked Questions:

What is the size of the European LED lighting market?

According to IMARC Group, the market was valued at US$ 24.7 billion in 2024.

What is the growth forecast for LED lighting in Europe?

The market is expected to grow at a CAGR of 8.87% from 2025 to 2033, reaching US$ 55.1 billion.

Who are the major players in the European LED market?

Key local players include Signify, Osram, and Zumtobel, while major global players include MLS Co., Ltd. (LEDVANCE) and Opple Lighting.

Why is the LED market growing so fast in Europe?

Growth is driven by government bans on fluorescent lighting, the need for energy efficiency, and the rise of smart city infrastructure.

Conclusion: Is Collaboration the New Competition?

The future of the Europe LED market is likely not a "winner takes all" scenario, but a hybrid ecosystem.

With a market destined for US$ 55.1 billion, there is room for both models. However, the overlap is growing. We expect to see more "Glocalization," where global capital funds European innovation. Brands that can navigate the 8.87% CAGR by combining the "Smart" capabilities of the local guard with the "Scale" of the global challengers will define the next decade of illumination.

About the Creator

Joey Moore

I'm Joey Moore, a seasoned Research Analyst with 5+ years of experience in market research. Expert in data analysis, strategic planning, and industry insights. Proven track record in delivering actionable reports.

Keep reading

More stories from Joey Moore and writers in Journal and other communities.

Generation Z's Impact on Europe Footwear Market: What Brands Need to Know

The European fashion landscape is currently experiencing a seismic shift. This change isn't driven by high-end runways in Milan or Paris. Instead, the scrolling habits and ethical demands of a younger demographic drive this transformation. Generation Z’s impact on Europe footwear market reshapes everything from global supply chain logistics to specific marketing hashtags.

By Joey Moorea day ago in Journal

~ Fired ~

— Ai Intrusion ~ Are you Next ~ Is Ai Evolution after your job? — Few workplaces haven't been affected. Ai is in supermarkets, at doctors' offices, and even monitoring farms. I just can't think of anything this machine is not getting into, can you? For instance: Education ~ Law and Tech jobs will one day have a major influence or be taken over by these inanimate machines, with accuracy and vigor. From mechanics' diagnoses to a wide variety of everyday jobs, including fast food workers, with this input having the ability to cut their unnecessary work hours. I'm certain all of us have been touched by this with our short stories and colorful headings, have you? Even comments are very questionable 'Non-Robot' insertions.

By Jay Kantor3 days ago in Journal

Comments

There are no comments for this story

Be the first to respond and start the conversation.