Credit Score vs CIBIL Score

What’s the Difference and Why It Matters

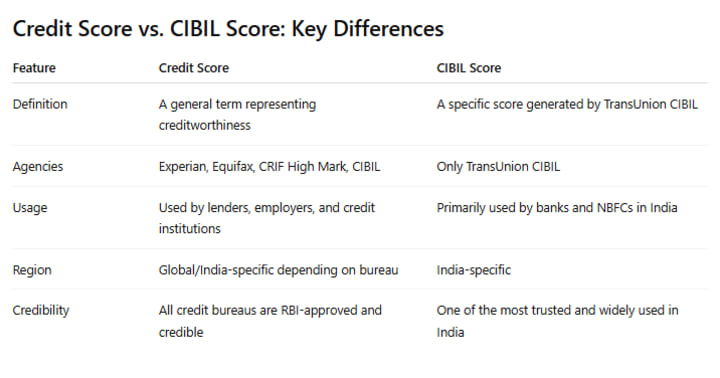

When it comes to personal finance in India, two terms often come up — Credit Score and CIBIL Score. While many people use these terms interchangeably, they’re not exactly the same. Understanding their differences is essential, especially if you're planning to apply for a loan or credit card. So, what do these terms really mean, and how do they affect your financial life? Let’s explore the distinctions, similarities, and everything in between.

What is a Credit Score?

A credit score is a three-digit numerical representation of an individual's creditworthiness. It’s based on a person’s credit history, repayment patterns, credit utilization, and other financial behavior. In essence, it helps lenders assess how likely you are to repay borrowed money on time.

In India, there are four primary credit bureaus authorized by the Reserve Bank of India (RBI) that generate credit scores:

CIBIL (Credit Information Bureau India Limited)

- Experian

- Equifax

- CRIF High Mark

Each bureau may calculate your score slightly differently based on its algorithm, but the general score range remains the same — from 300 to 900. A higher score indicates a better credit profile, which can lead to lower interest rates, higher loan approval chances, and better credit card offers.

Understanding Your Credit Report

A typical credit report includes the following key components:

1. Personal Identification Details

This section includes your full name, date of birth, gender, contact information, PAN number, and address history. These details help confirm your identity and link all credit activity to the correct individual.

2. Credit Account Summary

Also known as the accounts section, this part shows active and closed credit accounts such as loans and credit cards. It includes account numbers, types of credit, credit limits, outstanding balances, and repayment timelines.

3. Credit Inquiries

Credit inquiries are recorded every time someone checks your credit report. These are classified into:

- Hard Inquiries: Triggered when you apply for a loan or credit card. These can slightly lower your score.

- Soft Inquiries: Performed by you or companies for pre-approved offers; these don’t impact your score.

4. Credit Utilization Ratio

This is the ratio of your current outstanding credit to your total credit limit. A lower ratio (ideally under 30%) is seen as a sign of responsible credit usage.

5. Public Records

Details of any defaults, bankruptcies, or legal judgments related to your financial activities are listed here.

6. Age of Credit Accounts

The average age of your credit history. A longer credit history with consistent repayment behavior boosts your credit profile.

7. Credit Mix

Diversity in credit types — such as credit cards, personal loans, home loans, etc. — shows your ability to manage various forms of credit.

8. Score Analysis

This segment provides a summary of your credit score along with influencing factors like missed payments, high utilization, or too many hard inquiries.

9. Improvement Tips

Your report may offer suggestions to enhance your score, such as reducing your credit card balance or paying EMIs on time.

10. Dispute Resolution Section

In case you find incorrect information, this section allows you to raise disputes and get errors corrected, ensuring your report reflects accurate data.

What is a CIBIL Score?

The CIBIL Score is a specific type of credit score issued by TransUnion CIBIL, India’s first and one of the most prominent credit information companies. It functions just like a regular credit score but is calculated using CIBIL’s proprietary scoring model.

The CIBIL Score also ranges between 300 and 900, and a score above 750 is typically considered excellent by most banks and non-banking financial companies (NBFCs).

Components of the CIBIL Report

CIBIL credit reports are divided into six major sections:

1. CIBIL Score

A summary of your credit score based on credit activity and behavior captured over time.

2. Personal Information

Includes your full name, date of birth, gender, and identification numbers such as PAN or Aadhaar.

3. Contact Details

Your registered phone numbers, email addresses, and residential or official addresses are listed here.

4. Employment and Income Information

This section reflects the employment status and income data reported by your lenders at the time of application.

5. Account Information

Details of all active and closed credit accounts, including credit cards and loans, are covered here. It provides insights into payment history, current balances, overdue amounts, and EMI schedules, covering a history of at least 36 months.

6. Enquiry Information

Every time a lender requests your CIBIL report during a credit application, it is logged here with the name of the lender and the date.

Conclusion

Both Credit Score and CIBIL Score play a critical role in shaping your financial profile. While the CIBIL Score is a specific brand of credit score used primarily in India, the term credit score itself refers to the broader concept of measuring financial trustworthiness.

Understanding the difference helps you manage your finances better, avoid surprises during credit applications, and take informed steps to build or improve your credit profile. Whether you're applying for a home loan, a car loan, or even a premium credit card, maintaining a high credit or CIBIL score is key to unlocking the best financial opportunities.

About the Creator

Loan Resolve Services

Loan Settlement Agency in Delhi and all over India. We offer sevral services like - Debt, Personal Loan, Credit Card Loan And Business Loan Setllement.

For more info -

Keep reading

More stories from Loan Resolve Services and writers in Journal and other communities.

Struggling With Axis Bank Credit Card Dues?

In today’s unpredictable financial climate, managing credit card debt can be particularly challenging, especially when unforeseen events arise. These may include sudden job loss, medical emergencies, economic downturns, family crises, divorce or separation, and fluctuations in interest rates.

By Loan Resolve Services8 months ago in Journal

Regulatory Throughput as a Determinant of Aircraft Operational Availability

Aircraft operational availability is commonly attributed to fleet size, technological reliability, and market demand. This perspective underestimates the structural influence of regulatory compliance on aviation systems. This paper examines how regulatory throughput defined as the speed and capacity at which compliance processes are executed functions as a primary determinant of aircraft availability. By analyzing maintenance workflows, parts certification, and operational approvals, the study argues that aviation availability is governed more by regulatory process alignment than by technical capability or demand intensity.

By Beckett Dowhan4 days ago in Journal

Comments

There are no comments for this story

Be the first to respond and start the conversation.