Wood and Timber Products Market Size and Forecast 2025–2033: Sustainable Growth Shapes a Trillion-Dollar Industry

Rising demand from construction, furniture, and packaging industries positions wood as the material of the future

Global Wood and Timber Products Market Outlook

The global Wood and Timber Products Market is undergoing a steady transformation as sustainability, urbanization, and infrastructure development reshape material choices worldwide. According to Renub Research, the market is expected to grow from US$ 981.33 billion in 2024 to US$ 1,463.38 billion by 2033, expanding at a CAGR of 4.54% from 2025 to 2033.

This growth reflects more than just rising demand—it represents a shift in how industries view natural resources. Wood, once seen as a traditional construction input, is now emerging as a strategic, low-carbon alternative to steel, plastic, and concrete. Its renewability, versatility, and compatibility with modern engineering make it a cornerstone of sustainable development.

From high-rise timber buildings to modular furniture and biodegradable packaging, wood and timber products are at the heart of a global transition toward eco-friendly materials.

Understanding the Wood and Timber Products Market

The wood and timber products industry includes a wide array of processed and semi-processed materials such as lumber, plywood, veneer, particleboard, MDF, OSB, and engineered wood products like CLT and LVL. These materials serve critical roles in:

Residential and commercial construction

Furniture manufacturing

Packaging and pallets

Interior design and flooring

Paper and pulp production

Textile and biochemical applications

What distinguishes wood from many competing materials is its renewability and carbon storage capacity. When sourced responsibly, timber products reduce overall emissions, support circular economies, and contribute to climate mitigation goals.

Why the Market Is Expanding Steadily

1. Construction Industry Driving Consistent Demand

The construction sector remains the largest consumer of wood and timber products. With global urban populations rising and governments investing heavily in housing and infrastructure, demand for structural lumber, plywood, and engineered wood continues to climb.

Modern construction technologies have significantly expanded wood’s potential. Cross-laminated timber (CLT) and mass timber construction now allow wood to be used in mid-rise and even high-rise buildings, something previously dominated by concrete and steel. Builders increasingly choose timber for its lightweight nature, fast installation, thermal insulation, and aesthetic appeal.

In regions facing housing shortages—such as Asia-Pacific and parts of North America—wood-based modular construction is becoming a fast and cost-effective solution.

2. Technological Innovations in Wood Processing

Advances in processing and engineering are redefining what wood can do. Products like oriented strand board (OSB), laminated veneer lumber (LVL), and fire-resistant treated timber now offer superior strength, durability, and moisture resistance.

Automated sawmills, digital cutting, and precision engineering reduce waste and improve efficiency, while new preservation techniques extend product lifespan. These innovations make wood competitive in applications once reserved for synthetic materials, broadening its market reach across commercial, industrial, and residential sectors.

3. Sustainability as a Core Growth Engine

Environmental awareness is no longer optional—it is a purchasing decision driver. Governments, developers, and consumers increasingly prefer materials that support green building standards and carbon neutrality goals.

Wood’s low embodied carbon, biodegradability, and renewability make it a preferred choice in:

Sustainable architecture

Eco-friendly furniture

Biodegradable packaging

Circular economy initiatives

Certification programs such as FSC and PEFC play a vital role in ensuring responsible sourcing and building consumer trust. As sustainability becomes embedded in regulations and corporate ESG goals, demand for certified wood products continues to rise.

Key Challenges Facing the Industry

Environmental Regulations and Deforestation Concerns

Despite its sustainability potential, the industry faces scrutiny over deforestation and illegal logging. Governments and environmental organizations are imposing stricter controls on forest management, sourcing, and traceability.

Compliance requires investments in certification, audits, and supply chain transparency. While this increases costs in the short term, it also creates long-term stability and market credibility. Companies that fail to meet these standards risk losing access to major markets, especially in Europe and North America.

Raw Material Supply and Price Volatility

The wood industry is highly sensitive to climate events, labor shortages, forest policies, and geopolitical disruptions. Wildfires, pests, and floods can quickly reduce timber availability, driving up prices and disrupting production.

To manage this volatility, companies are diversifying sourcing strategies, investing in sustainable plantations, and improving inventory management. Still, balancing supply security with cost efficiency remains a persistent challenge.

Regional Market Insights

North America: Innovation and Sustainable Forestry Leadership

The United States and Canada are among the world’s largest producers and consumers of wood products. Managed forests, advanced processing technologies, and strong construction demand support steady growth.

The U.S. market benefits from the expansion of mass timber construction, green building certifications like LEED, and government-backed forest management programs. While labor shortages and regulatory compliance pose challenges, innovation keeps North America at the forefront of the industry.

Europe: Sustainability-Driven Demand

European markets, particularly Germany, France, the UK, and Scandinavia, prioritize certified and eco-labeled wood products. The region’s strict environmental policies encourage the use of timber in construction, interior design, and energy-efficient buildings.

Engineered wood products are gaining popularity in modern architecture, while recycling and circular material use are increasingly emphasized. Europe’s wood market is shaped more by sustainability policy than by volume expansion.

Asia-Pacific: Fastest-Growing Demand Center

Asia-Pacific represents the largest growth opportunity due to urbanization, population growth, and infrastructure investment.

China dominates production and consumption of wood panels and furniture.

India is witnessing rapid expansion driven by housing, modular furniture, and manufacturing incentives.

Southeast Asia serves as both a production hub and a growing consumption market.

Imports remain crucial, but local processing and engineered wood manufacturing are expanding rapidly.

Middle East & Africa: Import-Driven Expansion

In the United Arab Emirates and Saudi Arabia, demand is fueled by construction, hospitality, and luxury interior projects. With limited forest resources, the region relies heavily on imports from Europe, Asia, and North America.

Dubai and Abu Dhabi serve as major regional distribution hubs, while green building regulations are encouraging the use of certified wood products.

Latin America: Resource-Rich Production Hub

Countries like Brazil and Chile play a key role in supplying raw timber and processed products to global markets. Sustainable forestry investments and export-oriented production make Latin America an important player in the global supply chain.

Recent Industry Developments

In July 2024, Georgia-Pacific began production at its advanced Dixie facility, designed to improve energy efficiency and sustainability while producing premium paper-based products. This reflects a broader industry trend toward modernizing manufacturing and reducing environmental impact through technology investments.

Market Segmentation Snapshot

By Application

Furniture

Paper & Pulp

Lumber

Textiles

Bio-chemicals

Others

By Region

North America: United States, Canada

Europe: Germany, France, Italy, UK, Spain, Netherlands, Belgium, Turkey

Asia-Pacific: China, Japan, India, South Korea, ASEAN, Australia, New Zealand

Latin America: Brazil, Mexico, Argentina

Middle East & Africa: Saudi Arabia, UAE, South Africa

Competitive Landscape and Key Players

The global wood and timber products market is moderately fragmented, with both multinational corporations and regional specialists shaping competition. Key players covered include:

Stora Enso Oyj

West Fraser Timber Co. Ltd.

PotlatchDeltic Corporation

Resolute Forest Products

Timber Products Co. Limited Partnership

Sierra Forest Products, Inc.

Southern Pine Timber Products, Inc.

Ogonek Custom Hardwoods, Inc.

RSG Forest Products, Inc.

Timbeck Architecture

These companies focus on sustainable sourcing, value-added products, digitalization, and engineered wood innovations to strengthen their market positions.

Final Thoughts: A Market Built for the Future

The Wood and Timber Products Market is no longer defined by tradition alone—it is defined by innovation, sustainability, and strategic value. As climate policies tighten and industries seek greener alternatives, wood’s role as a renewable, carbon-storing, and versatile material will only grow stronger.

With the market projected to reach US$ 1.46 trillion by 2033, companies that invest in sustainable forestry, advanced processing, and certified supply chains will be best positioned to lead the next phase of growth.

In a world increasingly shaped by environmental responsibility, wood is not just a material—it is a solution.

About the Creator

Janine Root

Janine Root is a skilled content writer with a passion for creating engaging, informative, and SEO-optimized content. She excels in crafting compelling narratives that resonate with audiences and drive results.

Keep reading

More stories from Janine Root and writers in Futurism and other communities.

DIY Furniture Market Size and Forecast 2025–2033

Introduction: The Rise of Hands-On Home Design Furniture is no longer just something we buy—it is increasingly something we build, customize, and take pride in creating. Across the world, consumers are embracing a hands-on approach to home décor, driven by a desire for personalization, affordability, and sustainable living. This shift has given rise to the fast-growing DIY (Do-It-Yourself) furniture market, where flat-pack kits, modular designs, and ready-to-assemble products empower individuals to become co-creators of their living spaces.

By Janine Root 5 days ago in Futurism

About Binding Prometheus

I want to start actively advocating on behalf of my own work, and the most valuable part of my canon is, without a doubt, Binding Prometheus, the play I have been working on since 2019 and only finished in 2023 as part of my MA. The play itself is an amalgamation of a million different inspirations. On one end, it evokes the Ancient Greek myth-play, deriving its own title from the earliest extant work of Western drama we have, Aeschylus’s Prometheus Bound. On the other end, it borrows significantly from the sci-fi bulwarks from over the years, namely Mary Shelley’s Frankenstein and Karel Capek’s Rossum’s Universal Robots. The play could be an episode of Black Mirror, I fear. I don’t know. I’ve only ever seen one episode of Black Mirror.

By Steven Christopher McKnight19 days ago in Futurism

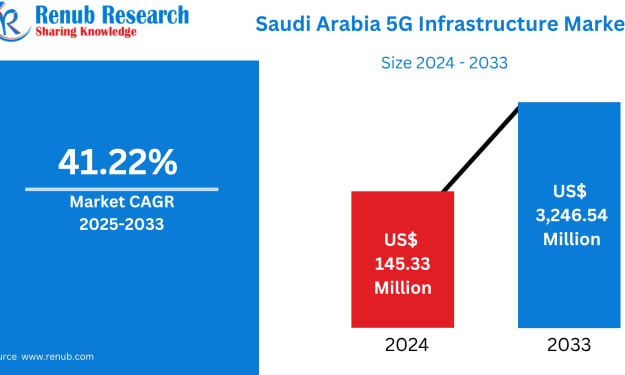

Saudi Arabia 5G Infrastructure Market Size and Forecast 2025–2033

Saudi Arabia 5G Infrastructure Market Outlook The Saudi Arabia 5G Infrastructure Market is poised for extraordinary expansion, projected to grow from US$ 145.33 million in 2024 to US$ 3,246.54 million by 2033, registering a remarkable CAGR of 41.22% during 2025–2033. This explosive growth reflects the Kingdom’s ambitious digital transformation agenda, driven by Vision 2030, large-scale smart city investments, and accelerating demand for ultra-high-speed, low-latency connectivity across critical sectors such as healthcare, energy, manufacturing, and telecommunications.

By jaiklin Fanandish5 days ago in Futurism

Comments

There are no comments for this story

Be the first to respond and start the conversation.