United States AI Server Market Size & Forecast 2026–2034

How America’s race for AI compute is reshaping data centers, enterprise IT, and the digital economy

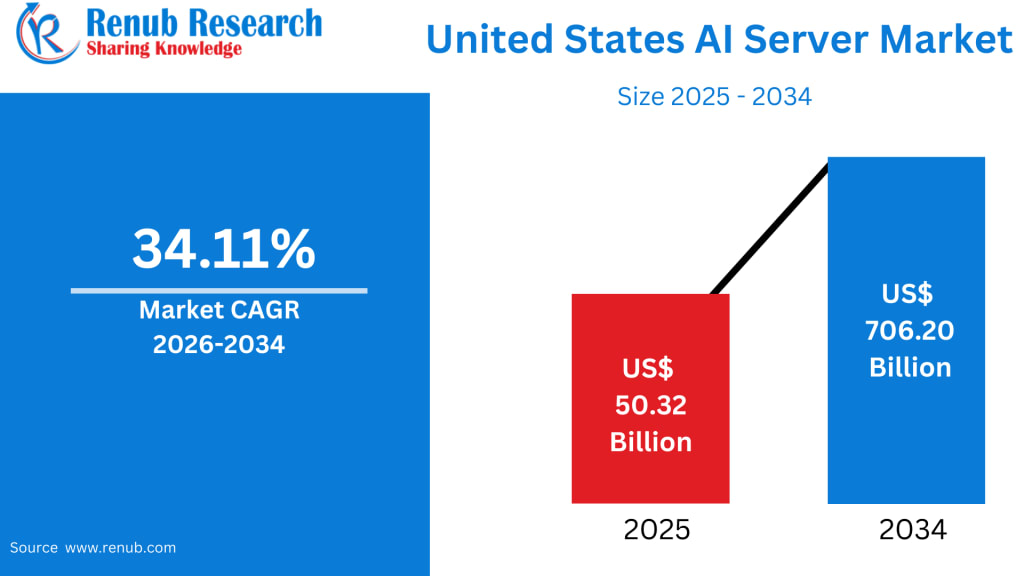

United States AI Server Market at a Glance

The United States AI server market is entering a historic growth phase. According to Renub Research, the market will expand from US$ 50.32 Billion in 2025 to US$ 706.20 Billion by 2034, representing a powerful CAGR of 34.11% from 2026 to 2034. This surge is being driven by the rapid expansion of artificial intelligence workloads across hyperscale data centers, cloud platforms, and enterprise IT environments. From generative AI and high-performance computing (HPC) to big data analytics and automation, demand for advanced GPU- and accelerator-based server infrastructure is transforming how organizations build and operate digital systems.

United States AI Server Market Overview

An AI server is a high-performance computing system purpose-built for artificial intelligence workloads, including machine learning, deep learning, natural language processing, computer vision, and generative AI. Unlike conventional servers, AI servers integrate powerful GPUs, TPUs, FPGAs, or application-specific integrated circuits (ASICs) that enable massive parallel processing of data at extraordinary speeds. These systems are also equipped with high-bandwidth memory, ultra-fast storage, and advanced networking fabrics to support data-intensive training and real-time inference at scale.

The United States has become the global epicenter of AI server adoption due to its leadership in artificial intelligence research, cloud computing, and digital infrastructure. Major technology companies, cloud service providers, startups, government agencies, and research laboratories rely on AI servers to train large language models (LLMs), analyze massive datasets, and automate operations across industries. As AI use cases expand in healthcare, finance, retail, defense, manufacturing, and autonomous systems, AI servers are becoming a foundational layer of the U.S. digital economy.

Growth Drivers in the United States AI Server Market

Explosion of AI Adoption Across Industries

AI has moved rapidly from experimentation to production in the United States. Enterprises are deploying AI for fraud detection, customer personalization, predictive maintenance, recommendation engines, and real-time analytics. These workloads require scalable, resilient infrastructure that far exceeds the capabilities of traditional servers. The proliferation of data from IoT devices, mobile applications, and enterprise systems is further accelerating the need for in-house and private-cloud AI computing.

GPU-accelerated servers dominate this transition. In 2023, NVIDIA shipped approximately 3.76 million data center GPUs, capturing the majority of the market. The architectural suitability of GPUs for AI workloads and their mature software ecosystem have made them the backbone of the U.S. AI server industry.

Generative AI and Large Language Models (LLMs)

The breakout of generative AI and LLMs has become a defining catalyst. Training and fine-tuning large models demand enormous parallel compute, high-bandwidth memory, and ultra-low-latency interconnects—capabilities best delivered by specialized AI servers. Enterprises are increasingly customizing foundation models with proprietary data, shifting workloads from purely public clouds to dedicated, hybrid, or on-premises environments.

Inference demand is also exploding as LLMs are embedded in productivity tools, customer service platforms, software development, and content creation. These real-time applications require dense clusters of AI servers in data centers and at the edge. In September 2022, NVIDIA introduced its NeMo and BioNeMo LLM cloud services, enabling developers to adapt and deploy customized AI for use cases ranging from chatbots and code generation to biomolecular research—further expanding infrastructure demand.

Government, Regulation, and Security Considerations

Public policy and national security concerns are indirectly boosting AI server adoption. Sensitive workloads involving healthcare records, financial data, defense systems, and intellectual property often cannot rely exclusively on multi-tenant public clouds. As data residency, AI governance, and transparency regulations tighten, organizations are investing in on-premises and sovereign AI infrastructure.

Cybersecurity mandates are also driving adoption of AI-powered analytics and threat detection systems, which require high-performance compute backends. In December 2025, the U.S. government and allied nations released new guidance on the safe use of AI in critical infrastructure, highlighting the importance of risk assessment, model governance, and operational fail-safes—reinforcing the need for controlled, high-performance AI environments.

Challenges in the United States AI Server Market

High Capital and Operating Costs

AI servers remain capital-intensive. GPU-based and accelerator-based systems are expensive, and large-scale deployments require significant investments in networking, storage, power, and cooling. Many enterprises struggle to justify upfront costs, particularly when AI use cases are still evolving.

Operational expenses also pose challenges. AI servers consume far more electricity and generate significantly more heat than traditional systems, increasing energy bills and requiring advanced cooling solutions. Upgrades to power distribution, backup systems, and thermal management often extend deployment timelines.

Skills Gaps and Integration Complexity

The shortage of AI infrastructure expertise is another limiting factor. Managing AI servers demands specialized skills in distributed training, container orchestration, GPU scheduling, and high-performance networking. Integrating these systems into legacy IT environments is often complex, with challenges around data pipelines, storage throughput, security controls, and software compatibility. These issues can lead to underutilized infrastructure or delayed returns on investment.

Market Segmentation Insights

United States GPU-based AI Server Market

GPU-based servers dominate the U.S. market, serving as the workhorses for deep learning and generative AI. Hyperscalers, SaaS providers, and enterprises standardize on GPU platforms to support frameworks like PyTorch and TensorFlow. Their massive parallelism and broad developer ecosystem make GPUs the default choice for both training and inference at scale.

United States ASIC-based AI Server Market

ASIC-based AI servers are emerging as high-efficiency alternatives for specialized workloads such as recommendation systems, video analytics, and large-scale inference. Designed for specific tasks, ASICs deliver superior performance-per-watt and lower total cost of ownership in predictable, high-volume environments. Cloud providers and internet giants are leading adoption through custom silicon initiatives.

Cooling Technologies: Air, Hybrid, and Liquid

Air Cooling: Remains the most widely deployed approach due to compatibility with existing data centers and lower upfront costs.

Hybrid Cooling: Combines air and liquid methods, enabling higher rack densities (30–80 kW and beyond) without full facility overhauls.

Liquid Cooling: Increasingly necessary for next-generation AI clusters, offering superior thermal efficiency for ultra-dense compute environments.

Form Factors: Blade and Tower Servers

AI Blade Servers: Provide dense, modular compute in chassis-based systems, ideal for centralized enterprise data centers with space constraints.

AI Tower Servers: Address edge, branch, and SMB needs, enabling localized AI for applications such as video analytics, quality inspection, and retail intelligence.

End-Use Industry Analysis

BFSI (Banking, Financial Services, and Insurance)

AI servers power fraud detection, algorithmic trading, credit scoring, risk modeling, and customer personalization. Given regulatory scrutiny and data sensitivity, financial institutions increasingly deploy on-premises AI infrastructure for low-latency, secure analytics.

Healthcare & Pharmaceuticals

Hospitals, research centers, and pharmaceutical firms use AI servers for imaging diagnostics, genomics, drug discovery, and clinical decision support. These workloads require both massive compute capacity and strict compliance with healthcare regulations, driving adoption of private-cloud and on-premises AI clusters.

Automotive

From autonomous driving and ADAS development to manufacturing automation and connected vehicle services, AI servers are central to the automotive industry. Training perception and planning models demands large GPU clusters, while backend servers process telematics data and enable predictive maintenance and in-car digital experiences.

State-Level Market Dynamics

California

California remains the epicenter of the U.S. AI server market. Home to hyperscalers, semiconductor leaders, and AI startups, the state hosts massive data centers and innovation hubs. In October 2025, Super Micro Computer launched a subsidiary in San Jose to provide AI server solutions for U.S. federal agencies, reinforcing California’s leadership in advanced compute.

New York

New York’s AI server market is anchored in finance, media, and advertising. Banks, hedge funds, and insurers deploy AI servers for real-time analytics, trading, and compliance. Low-latency data centers around financial exchanges make local AI clusters critical for competitive advantage.

Texas

Texas is rapidly emerging as a major AI server hub due to favorable energy economics, abundant land, and expanding technology ecosystems in Dallas-Fort Worth, Austin, and Houston. Hyperscale data centers designed for AI workloads are proliferating, supported by demand from energy, manufacturing, logistics, and healthcare sectors.

Market Segmentation (As Covered)

Type: GPU-based, FPGA-based, ASIC-based

Cooling Technology: Air, Liquid, Hybrid

Form Factor: Rack-mounted, Blade, Tower

End Use: IT & Telecommunications, BFSI, Retail & E-commerce, Healthcare & Pharmaceutical, Automotive, Others

Top States: California, Texas, New York, Florida, Illinois, Pennsylvania, Ohio, Georgia, New Jersey, Washington, North Carolina, Massachusetts, Virginia, Michigan, Maryland, Colorado, Tennessee, Indiana, Arizona, Minnesota, Wisconsin, Missouri, Connecticut, South Carolina, Oregon, Louisiana, Alabama, Kentucky, Rest of United States

Competitive Landscape

Renub Research evaluates major players using five viewpoints: Overview, Key Personnel, Recent Developments, SWOT Analysis, and Revenue Analysis. Key companies shaping the U.S. AI server ecosystem include:

Dell Inc.

Cisco Systems, Inc.

IBM Corporation

HP Development Company, L.P.

Huawei Technologies Co., Ltd.

NVIDIA Corporation

Fujitsu Limited

ADLINK Technology Inc.

Lenovo Group Limited

Super Micro Computer, Inc.

These firms are competing on performance, energy efficiency, system integration, and specialized AI workloads, while forming partnerships with cloud providers and enterprise customers.

Final Thoughts: The Infrastructure Race Behind America’s AI Boom

The United States AI server market is not merely growing—it is redefining the foundation of the digital economy. With market size projected to surge from US$ 50.32 Billion in 2025 to US$ 706.20 Billion by 2034, AI servers are becoming as essential to modern organizations as networking and storage once were.

Generative AI, automation, cybersecurity, healthcare innovation, and autonomous systems all depend on scalable, high-performance compute. While high costs, energy demands, and skills shortages present challenges, ongoing advances in hardware design, cooling technologies, and software orchestration are steadily lowering barriers to adoption.

As enterprises, governments, and cloud providers continue to invest in next-generation AI infrastructure, the AI server market will remain one of the most strategic and transformative segments of the U.S. technology landscape. For businesses positioning themselves for the next decade of digital growth, AI servers are no longer optional—they are the engine powering the future.

About the Creator

Keep reading

More stories from Aaina Oberoi and writers in Futurism and other communities.

Saudi Arabia E-commerce Apparel Market Size and Forecast 2026–2034

Introduction Saudi Arabia is rapidly reshaping its retail landscape, and nowhere is this transformation more visible than in the e-commerce apparel segment. What was once a largely mall-centric and brand-store-driven fashion economy is now becoming mobile-first, influencer-led, and digitally personalized. Driven by a tech-savvy population, expanding logistics infrastructure, and sweeping economic reforms under Vision 2030, online apparel shopping is emerging as a cornerstone of the Kingdom’s consumer economy.

By Aaina Oberoi3 days ago in Futurism

About Binding Prometheus

I want to start actively advocating on behalf of my own work, and the most valuable part of my canon is, without a doubt, Binding Prometheus, the play I have been working on since 2019 and only finished in 2023 as part of my MA. The play itself is an amalgamation of a million different inspirations. On one end, it evokes the Ancient Greek myth-play, deriving its own title from the earliest extant work of Western drama we have, Aeschylus’s Prometheus Bound. On the other end, it borrows significantly from the sci-fi bulwarks from over the years, namely Mary Shelley’s Frankenstein and Karel Capek’s Rossum’s Universal Robots. The play could be an episode of Black Mirror, I fear. I don’t know. I’ve only ever seen one episode of Black Mirror.

By Steven Christopher McKnight11 days ago in Futurism

10 App Developers in the UAE Advancing Secure Mobile Platforms

As mobile applications become central to daily life, security has emerged as a defining factor in app development. In the UAE, where digital adoption is accelerating across sectors such as finance, healthcare, government services, and eCommerce, mobile platforms are expected to meet high standards of data protection, privacy, and reliability.

By Apptunix usa5 days ago in Futurism

Standing While Falling

Quotation from Friedrich Nietzsche "He who wrestles long with monsters should beware lest he himself become a monster. And if you gaze long into an abyss, the abyss also gazes into you. Man is not destroyed by suffering, but by the meaning he makes of it."

By LUCCIAN LAYTH5 days ago in Critique

Comments

There are no comments for this story

Be the first to respond and start the conversation.