Health Insurance Market: Preventive Care Focus, Value-Based Models & Industry Trends

How aging populations, chronic disease prevalence, and preventive care models are influencing policy demand

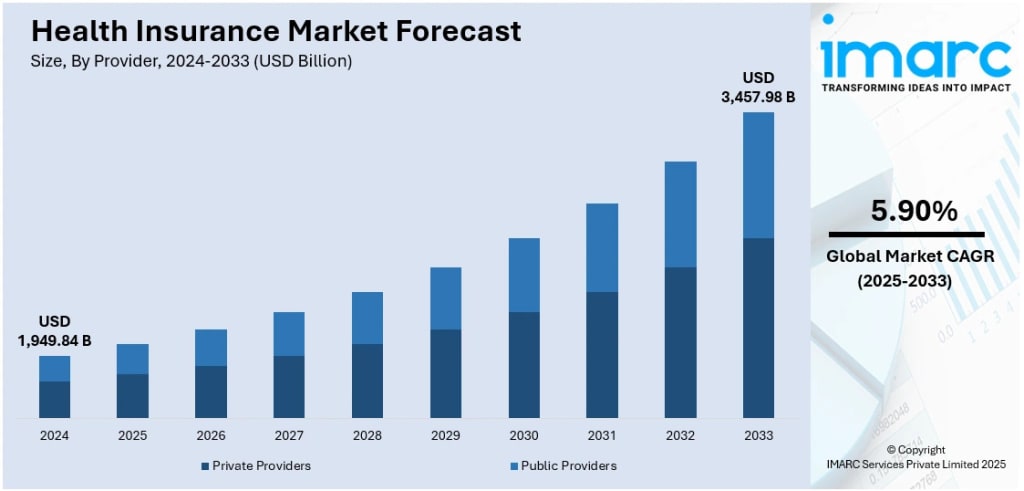

According to IMARC Group's latest research publication, global health insurance market size reached USD 1,949.84 Billion in 2024. Looking forward, IMARC Group expects the market to reach USD 3,457.98 Billion by 2033, exhibiting a growth rate (CAGR) of 5.90% during 2025-2033.

How AI is Reshaping the Future of Health Insurance Market

- Automated Claims Processing and Instant Approvals: AI processes 84% of health insurance claims automatically, reducing approval times from weeks to hours. UnitedHealth expects AI to direct over 50% of customer calls by end of 2025, drastically improving operational efficiency.

- Fraud Detection and Risk Management: Machine learning identifies fraudulent claims patterns with 95% accuracy, saving insurers millions annually. Aviva's 80 AI models cut liability assessment time by 23 days while reducing customer complaints by 65%.

- Personalized Underwriting and Pricing: AI analyzes patient data to create tailored coverage plans and dynamic pricing. Earnix's explainable AI enables real-time pricing adjustments, while ensuring transparency in underwriting decisions for regulatory compliance.

- Predictive Healthcare and Preventive Care: AI predicts patient health risks before conditions worsen, enabling proactive interventions. By 2030, insurance shifts from detect-and-repair to predict-and-prevent models, leveraging smart contracts and adaptive AI for dynamic coverage.

- Enhanced Customer Experience Through Chatbots: AI-powered virtual assistants provide 24/7 support with natural language processing. Elevance Health's 50,000 employees use generative AI, while Cigna's Smart Claim Submission auto-fills details, improving member satisfaction scores by 36 percentage points.

Health Insurance Industry Overview:

The health insurance landscape is experiencing unprecedented transformation driven by chronic disease prevalence, aging demographics, and technological revolution. Chronic diseases account for USD 47 Trillion globally, while diabetes alone affects 537 Million adults worldwide and is projected to reach 783 Million by 2045. The geriatric population aged 60 and above represents 1.2 Billion people—12% of the global population—and will double to 2.1 Billion by 2050. Healthcare AI spending tripled to 1.4 Billion dollars, with 22% of healthcare organizations implementing domain-specific AI tools, a 7-fold increase over previous years. The industry processes 83% of claims digitally, while 92% of US health insurers have adopted AI governance principles. Private insurers control 51.7% of the market, and PPOs dominate with 60.9% market share, reflecting consumer preference for flexible provider networks and coordinated care delivery.

Health Insurance Market Trends & Drivers

The chronic disease epidemic is fundamentally reshaping insurance demands and cost structures. Heart disease remains the leading cause of death in developed nations, while diabetes cases continue their alarming trajectory with 537 Million people currently affected and projections reaching 783 Million by 2045. The Middle East and North Africa region alone accounts for 73 Million diabetes cases, expected to grow to 136 Million within two decades. These conditions drive sustained healthcare utilization, pushing insurers to develop specialized coverage products with enhanced benefits for chronic disease management. Insurers are responding with preventive care incentives—fitness monitoring programs, wellness rewards, and regular screening coverage—designed to catch conditions early before they become costly. The Affordable Care Act and similar regulatory frameworks mandate coverage for chronic conditions without discrimination, fundamentally altering underwriting practices and requiring insurers to absorb higher-risk populations while maintaining profitability through volume and preventive strategies.

Demographic shifts are creating unprecedented pressure on healthcare systems and insurance models. The global population aged 60 and above reached 1.2 Billion in 2024—representing 12% of humanity—and will double to 2.1 Billion by 2050, constituting 26% of the world's population. The Asia Pacific region houses 672 Million seniors, 61% of the global elderly population, projected to reach 1.3 Billion by 2050. In Europe, those 65 and older comprise 21.6% of the EU population, growing annually by 0.3%. This demographic reality drives specialized product development, with Medicare serving 65 million Americans and insurers creating long-term care coverage, prescription drug plans, and chronic condition management programs. Older adults generate substantially higher per-capita healthcare costs, requiring more frequent medical interventions, specialist consultations, and prescription medications. Government programs like Medicare face sustainability challenges, creating opportunities for private insurers to offer supplemental coverage and Medicare Advantage plans that now serve millions of seniors seeking enhanced benefits beyond basic government coverage.

Technology adoption and regulatory frameworks are revolutionizing insurance delivery and oversight. Health insurers are deploying AI at 2.2 times the rate of broader economy, with 84% now utilizing artificial intelligence in some capacity according to NAIC surveys covering 93 companies. Healthcare organizations invested 1.4 Billion dollars in AI solutions, nearly tripling previous investments, focusing on claims automation, fraud detection, and customer service enhancement. However, regulatory responses are intensifying—23 states plus Washington DC adopted NAIC's AI Model Bulletin, while Colorado's Artificial Intelligence Act mandates governance procedures to prevent discrimination. Agentic AI systems capable of autonomous decision-making emerged in 2025 for underwriting and claims processing, prompting regulators to develop evaluation frameworks assessing consumer protection and fairness. The dichotomy is striking: while insurers report double-digit efficiency gains and companies like Aviva save 82 million dollars annually through AI implementation, nearly one-third still don't regularly test models for bias despite regulatory recommendations, creating tension between innovation speed and consumer safeguards.

Leading Companies Operating in the Global Health Insurance Industry:

- Aetna Inc

- AIA Group Limited

- Allianz Care

- Aviva India

- AXA Global Healthcare

- Centene Corporation

- Cigna Healthcare

- CVS Health

- International Medical Group, Inc.

- National Insurance Company Limited

- Ping An Insurance (Group) Company of China, Ltd

- United HealthCare Services, Inc.

- Zurich Kotak General Insurance

Health Insurance Market Report Segmentation:

By Provider:

- Private Providers

- Public Providers

Private providers dominate the market in 2024 with 51.7% share, offering diverse and customizable insurance products along with extensive healthcare networks.

By Type:

- Life-Time Coverage

- Term Insurance

Lifetime coverage leads with a 53.5% market share in 2024, providing long-term security and comprehensive benefits at stable premium rates.

By Plan Type:

- Medical Insurance

- Critical Illness Insurance

- Family Floater Health Insurance

- Others

Medical insurance holds a 51.8% market share in 2024, covering essential healthcare services and promoting preventive care to reduce financial burdens.

By Demographics:

- Minor

- Adults

- Senior Citizen

Adults represent 57.5% of the market in 2024, largely due to employer-sponsored plans and policies that cover entire families.

By Provider Type:

- Preferred Provider Organizations (PPOs)

- Point of Service (POS)

- Health Maintenance Organizations (HMOs)

- Exclusive Provider Organizations (EPOs)

Preferred Provider Organizations (PPOs) lead the market with 60.9% share in 2024, offering flexibility in provider choice and coverage for both in-network and out-of-network services.

Region Insights:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

North America captures over 65.4% of the healthcare insurance market in 2024, driven by its affluent population and complex healthcare systems that necessitate private insurance.

Recent News and Developments in Health Insurance Market

- May 2025: Medica launched operations in St. Louis with comprehensive commercial health plans spanning small group ACA, level-funded, fully insured and self-insured large group options. The nonprofit insurer invested 6.8 million dollars in community health initiatives and logged over 9,000 employee volunteer hours, reinforcing its 50-year commitment to patient-centered care over shareholder profits.

- March 2025: Claremont Insurance Services partnered with Health Net to expand access to health insurance solutions for small business brokers across California. The collaboration provides increased access to premium, cost-effective insurance options, demonstrating the trend toward strategic partnerships to enhance market reach and service delivery in competitive insurance markets.

- March 2025: Toothlens partnered with Allied Insurance Company, Vizza Broking Services, and Star Health to introduce India's first cashless Dental OPD insurance service. This groundbreaking launch brings dental care under conventional health insurance coverage for the first time, providing comprehensive access to advanced dental care services previously excluded from standard health policies.

- January 2025: Care Health Insurance launched Ultimate Care, a revolutionary health insurance program offering comprehensive coverage with additional benefits including the MoneyBack feature, which provides incentives to policyholders for maintaining updated health records. The innovation represents the industry's shift toward rewarding proactive health management and preventive care engagement.

- November 2024: Patient Square Capital completed its 2.6 billion dollar acquisition of Premier Inc., marking one of the largest healthcare services deals. The transaction reflects sustained M&A activity in health services, with deal values reaching 46 billion dollars despite regulatory uncertainty, as private equity investors increasingly target software platforms supporting care delivery and operational efficiency.

Note: If you require specific details, data, or insights that are not currently included in the scope of this report, we are happy to accommodate your request. As part of our customization service, we will gather and provide the additional information you need, tailored to your specific requirements. Please let us know your exact needs, and we will ensure the report is updated accordingly to meet your expectations.

About the Creator

Andrew Sullivan

Hello, I’m Andrew Sullivan. I have over 9+ years of experience as a market research specialist.

Keep reading

More stories from Andrew Sullivan and writers in Futurism and other communities.

OSS & BSS Market: API Ecosystems, Microservices & Market Expansion

According to IMARC Group's latest research publication, global OSS & BSS market size reached USD 65.81 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 148.26 Billion by 2034, exhibiting a growth rate (CAGR) of 9.4% during 2026-2034.

By Andrew Sullivan6 days ago in Futurism

About Binding Prometheus

I want to start actively advocating on behalf of my own work, and the most valuable part of my canon is, without a doubt, Binding Prometheus, the play I have been working on since 2019 and only finished in 2023 as part of my MA. The play itself is an amalgamation of a million different inspirations. On one end, it evokes the Ancient Greek myth-play, deriving its own title from the earliest extant work of Western drama we have, Aeschylus’s Prometheus Bound. On the other end, it borrows significantly from the sci-fi bulwarks from over the years, namely Mary Shelley’s Frankenstein and Karel Capek’s Rossum’s Universal Robots. The play could be an episode of Black Mirror, I fear. I don’t know. I’ve only ever seen one episode of Black Mirror.

By Steven Christopher McKnight18 days ago in Futurism

UAE PVC Pipes Market: Residential Construction Growth, Utility Projects & Industry Trends

According to IMARC Group's latest research publication, UAE PVC pipes market size reached USD 280.0 Million in 2024. The market is projected to reach USD 384.0 Million by 2033, exhibiting a growth rate of 3.6% during 2025-2033.

By Abhay Rajput4 days ago in Futurism

Comments

There are no comments for this story

Be the first to respond and start the conversation.