Asia Pacific In Vitro Diagnostics Market Poised for Sustained Expansion, Projected to Reach USD 45.11 Billion by 2031

Rising chronic disease burden, aging populations, and accelerated healthcare infrastructure investments position IVD as a strategic priority across Asia Pacific

The Asia Pacific in vitro diagnostics (IVD) market is entering a decisive growth phase, underscoring its strategic importance for healthcare leaders, diagnostics manufacturers, and investors worldwide. Valued at an estimated USD 29.27 billion in 2026, the market is projected to reach USD 45.11 billion by 2031, expanding at a robust CAGR of 9.0% during the forecast period.

This growth trajectory reflects a critical question facing regional healthcare systems today: How can providers meet rising diagnostic demand while improving efficiency and clinical outcomes? The answer increasingly lies in scalable, technology-driven IVD solutions.

Download PDF Brochure of Asia Pacific In Vitro Diagnostics Market

Market Momentum Driven by Structural Healthcare Shifts

What is fueling this acceleration? Across Asia Pacific, steady improvements in healthcare infrastructure are expanding access to diagnostic services, particularly in emerging economies. Why does this matter now? Governments and healthcare providers are prioritizing early detection, preventive care, and continuous disease management to address escalating healthcare costs and outcomes.

When combined with a rapidly growing older adult population—requiring repeated diagnostic evaluations for diabetes, cardiovascular disorders, kidney disease, and other age-associated conditions—testing volumes continue to rise. This demographic shift is also driving greater reliance on routine health check-ups and long-term monitoring, reinforcing sustained demand for a broad range of IVD products and services.

Where demand is intensifying further is in infectious diseases, oncology, and chronic pathologies, where increasing incidence rates necessitate frequent and follow-up testing. As a result, diagnostic utilization across laboratories, hospitals, and decentralized settings remains on an upward curve.

Key Market Takeaways for Decision-Makers

By Country: China accounted for the largest share of the Asia Pacific IVD market in 2025 and is expected to be the fastest-growing country through the forecast period.

By Product & Service: Reagents and kits are projected to register the highest CAGR of 9.5%, supported by high-volume routine testing and widespread clinical application.

By Technology: Immunoassays held the largest market share in 2025, while molecular diagnostics is expected to grow at the fastest pace, driven by precision medicine and infectious disease testing.

By Specimen: Blood, serum, and plasma specimens dominated due to standardized handling protocols and broad platform compatibility.

By Site of Testing: Laboratory testing remained the leading segment in 2025, reflecting centralized diagnostic networks and high-throughput workflows.

By Application: Infectious diseases emerged as the largest application segment, supported by large-scale screening and continuous monitoring needs.

By End User: Clinical laboratories are expected to grow the fastest, as healthcare systems outsource and centralize diagnostic services to improve efficiency.

Competitive Landscape: Scale, Innovation, and Strategic Positioning

Who is shaping the competitive dynamics? Established global players such as F. Hoffmann-La Roche Ltd., Abbott, Danaher Corporation, Sysmex Corporation, and Shenzhen Mindray Bio-Medical Electronics Co. continue to lead the Asia Pacific IVD market. Their dominance is supported by extensive product portfolios, strong regional distribution networks, and sustained investments in automation and high-throughput diagnostic platforms.

At the same time, why are niche innovators gaining attention? Emerging players such as Devyser (Sweden) and Boster Biological Technology (US) are carving out specialized positions by focusing on targeted assays and differentiated diagnostic niches, highlighting opportunities for innovation-led growth alongside scale-driven competition.

Trends and Disruptions Reshaping Diagnostic Demand

How is the market evolving? Adoption of advanced testing technologies, point-of-care diagnostics, and digital diagnostic tools is reshaping laboratory workflows and care delivery models. Automation, data integration, and decentralized testing are improving turnaround times, expanding access in remote settings, and enabling a more responsive diagnostic ecosystem across Asia Pacific.

These shifts are particularly relevant for healthcare executives navigating rising patient volumes, workforce constraints, and pressure to deliver faster, more accurate diagnostic outcomes.

Market Dynamics: Risks and Opportunities

Drivers: Rising prevalence of chronic diseases is increasing reliance on both laboratory-based and point-of-care diagnostics.

Restraints: High capital costs for advanced analyzers and automation systems continue to limit adoption in resource-constrained settings.

Opportunities: Advances in disease-specific biomarkers and companion diagnostics are opening pathways for precision medicine and targeted therapies.

Challenges: Operational inefficiencies, staffing shortages, and data security concerns underscore the need for workflow optimization and digital resilience.

Why This Market Matters Now

For CEOs, CFOs, and strategic leaders, the Asia Pacific IVD market represents more than growth—it signals a structural shift in how healthcare systems diagnose, monitor, and manage disease at scale. Investments in diagnostics are no longer optional; they are foundational to preventive care strategies, cost containment, and long-term population health outcomes.

About the Creator

Keep reading

More stories from Juan Martinez and writers in Futurism and other communities.

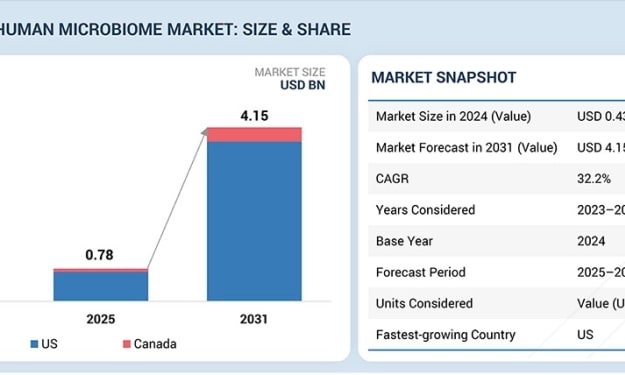

North America Human Microbiome Market Set to Surge at 32.2% CAGR, Reaching USD 4.15 Billion by 2031

The North America human microbiome market is entering a decisive growth phase as healthcare systems, biotechnology leaders, and research institutions accelerate investments in next-generation, microbiome-based solutions. Valued at USD 0.43 billion in 2024 and rising sharply to USD 0.78 billion in 2025, the market is projected to expand at a robust CAGR of 32.2% from 2025 to 2031, reaching an estimated USD 4.15 billion by the end of the forecast period.

By Juan Martinez3 days ago in Futurism

About Binding Prometheus

I want to start actively advocating on behalf of my own work, and the most valuable part of my canon is, without a doubt, Binding Prometheus, the play I have been working on since 2019 and only finished in 2023 as part of my MA. The play itself is an amalgamation of a million different inspirations. On one end, it evokes the Ancient Greek myth-play, deriving its own title from the earliest extant work of Western drama we have, Aeschylus’s Prometheus Bound. On the other end, it borrows significantly from the sci-fi bulwarks from over the years, namely Mary Shelley’s Frankenstein and Karel Capek’s Rossum’s Universal Robots. The play could be an episode of Black Mirror, I fear. I don’t know. I’ve only ever seen one episode of Black Mirror.

By Steven Christopher McKnight25 days ago in Futurism

Comments

There are no comments for this story

Be the first to respond and start the conversation.