How to Secure Your Financial Future: Easy Ways to Improve Financial Wellness

How to Secure Your Financial Future: Easy Ways to Improve Financial Wellness

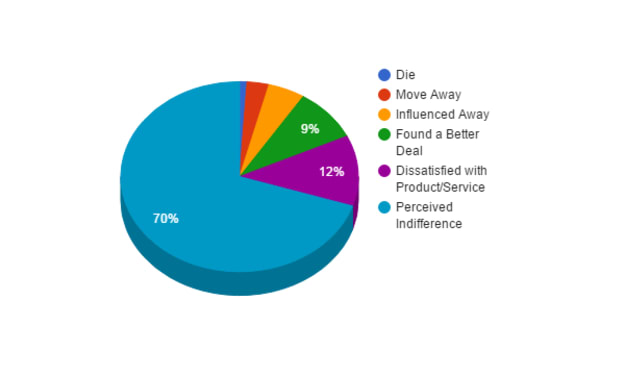

Recent studies show that only 40% of Americans feel confident about their retirement savings - a notable decline from 45% last year.

Managing finances can overwhelm anyone, especially with the constant balance between daily costs and future savings goals. True financial wellness means more than just money in your account - it brings peace of mind through proper emergency planning and smart choices that boost your quality of life.

A solid financial strategy makes all the difference. Simple steps like creating an emergency fund for 3-6 months of expenses or putting aside 15% of your income toward retirement can secure your financial future.

Your journey to financial confidence starts now. Let's discover practical strategies to strengthen your financial wellness and create lasting security for your family.

Know Where You Stand: Check Your Financial Health

You need a clear picture of your financial standing to make money improvements. Think of a financial health check as a medical exam for your money that spots strengths and areas that need work.

Start by calculating your net worth. Add what you own (savings, investments, property) and subtract what you owe (mortgage, credit cards, loans). This number shows your current financial position at a glance. You can measure your wealth-building progress by tracking this number over time.

Your debt-to-income ratio comes next. Divide your monthly debt payments by your monthly gross income. Lenders use this ratio to check your borrowing risk, which affects your credit score. A lower ratio shows better financial health.

Look at your spending patterns by recording every purchase for 30 days. This practice quickly reveals where your money goes and shows ways to reduce spending. Set up a monthly budget with these categories:

Monthly income (all sources)

Fixed expenses (rent, utilities)

Variable expenses (food, entertainment)

Savings contributions

Debt payments

Your actual spending compared to budgeted amounts will show areas that need improvement. The U.S. personal saving rate shows what percentage of disposable income Americans save - use this to benchmark your savings.

Make sure your Emergency fund covers 3-6 months of simple expenses. This safety net protects you when unexpected costs hit, like job loss or car repairs.

The final step checks your progress on other savings goals: home down payment, college funds, vehicle replacement, and vacation savings.

This financial health check gives you a complete understanding of your money situation. You can create a plan that works for your financial wellness with this foundation.

Create Your Money Plan: Financial Wellness Tips

Your financial plan starts with clear money goals. A solid plan shows you exactly where your money should go and helps you take control of your finances.

Setting Financial Goals

List your money goals by priority. Put them into these categories:

Short-term goals (0-12 months): build an emergency fund, pay off credit card debt

Medium-term goals (1-3 years): save for a vacation, buy a car

Long-term goals (3+ years): save for retirement, set up college funds

Your goals need to be SMART: Specific, Measurable, Achievable, Relevant, and Time-Bound. Each goal should have a specific dollar amount and deadline so you can track your progress.

Build a Budget That Works

Your budget acts as a money roadmap. Here's how to start:

Calculate your net income (what you take home after taxes)

Track everything you spend for 30 days

Split your expenses between fixed (rent, utilities) and variable (groceries, entertainment)

Use the 50/30/20 rule: 50% goes to needs, 30% to wants, 20% to savings and paying off debt

Make savings your top budget priority. Look at your spending often to stay on track.

Create Your Emergency Fund

Emergency funds protect you from unexpected costs. Start with $1,000, then work up to 3-6 months of expenses. People with irregular income should save enough for 6+ months.

Keep emergency money in a savings or money market account where you can get it quickly. This money helps with real emergencies like medical bills, car repairs, or job loss.

Make Saving Automatic

Set up regular transfers from your checking to savings accounts. Ask your employer to send part of your paycheck straight to savings through direct deposit. Whenever you get extra money from bonuses, tax refunds, or gifts, save some or all of it to reach your goals faster.

Remember, budgeting gives you freedom to spend on what matters most to you.

Take Action: Steps to Improve Financial Wellness

A solid financial plan and awareness of your money situation matter greatly, but action drives real financial wellness.

Automate Your Savings

You can make saving simple by setting up automatic transfers between your checking and savings accounts. This helps you avoid becoming "your own worst enemy" with saving. Here are some smart automation tactics:

Split your paycheck deposit to send money directly into a high-yield savings account

Time your transfers to match payday before the money disappears

Keep the money hidden from view to reduce spending temptation

This "set and forget" system builds your savings without draining your willpower.

Build Your Emergency Fund

Your first goal should be saving $1,000 for unexpected costs. Next, aim to cover 3-6 months of living expenses. This money should stay in an easily accessible savings, checking, or money market account for emergencies.

Manage Your Debt Effectively

The avalanche method helps you tackle high-interest debt first. Put extra money toward your highest-interest accounts while paying minimums on others. A single, lower-interest loan might help you simplify payments and save money by consolidating multiple debts.

Boost Your Retirement Savings

Make the most of your employer's 401(k) matching program or similar plan. You should aim for 15% in retirement savings, but at minimum, contribute enough to get the full match. Many workplace plans let you automatically increase contributions by 1-2% yearly. This step-by-step approach makes saving easier.

Cut Unnecessary Expenses

Look at your subscriptions and ask yourself: "How much do I use this? Do I really need this? Can I live without this?". Small cuts add up quickly. Financial experts suggest spending no more than 30% of your income on housing. Lower expenses mean more money for debt payment and savings goals.

Financial wellness takes time. Small, consistent actions create big results over time.

Small steps build lasting financial security. Money management becomes less daunting when you tackle one goal at a time.

A quick assessment of your financial health starts with net worth calculations and spending analysis. Your budget should balance saving priorities with life's pleasures.

The path to financial stability becomes clearer when you:

Track your expenses and savings goals regularly

Build an emergency fund for unexpected costs

Set up automatic savings deposits

Manage your debt wisely

Maximize your retirement contributions

Today's financial choices shape your future security. Pick one action - calculate your net worth or set up automatic savings. Every step brings you closer to lasting financial wellness.

Financial health grows through consistent habits rather than perfect decisions. Take control of your financial future by making your money work harder.

About the Creator

Barriers to NLP Adoption in Healthcare Organizations

Natural Language Processing (NLP) has the potential to unlock enormous value in healthcare from improving documentation quality to streamlining revenue cycle operations and strengthening data governance. Yet despite years of promise, NLP adoption across healthcare organizations remains uneven and slow.

By Lilly Scott4 days ago in Writers

🅼🅸🅳🅽🅸🅶🅷🆃 🆂🅽🅰🅲🅺🆂

"It's 10 in Tuscon! We all know what that means... It's Time for Midnight Snacks with your man, Gerald Gee! Ready to spend the night together? Me too! I'm full of snacks and can't wait to regurgitate them all back into your hungry ears. Crack a brew! Pop some corn! Anything to get ready for one hell of a show where the talk maybe cheap but the words cut deep...

By Lamar Wigginsa day ago in Fiction

Comments

There are no comments for this story

Be the first to respond and start the conversation.