What is Mortgage Insurance? Different Types And Cost 2022

what is mortgage insurance and how it works?

Mortgage insurance is a type of insurance that protects against default on home loans. Because private mortgage insurance (PMI) mitigates risk to the investors who own mortgages, it allows folks with down payments less than 20% to purchase a home.

This, in addition to other measures taken by lenders, such as including a mortgagee clause within your homeowners insurance policy, all help to protect mortgage investors.

Generally, if you put less than 20% down on a home, most conventional lenders will require you to purchase PMI.

A conventional loan is a loan that isn’t backed by the federal government.

Mortgage insurance is an additional monthly expense you’ll need to consider.

How Mortgage Insurance Works

Mortgage insurance protects mortgage lenders by compensating their losses when borrowers fail to repay in certain conditions, such as default or death, depending on the policies.

The premium and coverage of mortgage insurance are determined by the value of the borrowed amount.

The premium is typically a percentage of the loan value. It is integrated into the monthly payments for the loan.

The coverage of mortgage insurance falls as the mortgage does since the principal and interest are gradually repaid by the borrower.

When mortgage insurance is purchased, a master policy is issued to the beneficiary, which is a bank or another mortgage lender entity.

A master policy specifies how the default should be notified when the coverage is applied or denied, and other conditions.

It usually requires the exclusion of misrepresentation, fraud, and negligence.

What’s The Cost Of Mortgage Insurance?

Mortgage insurance costs depend on the type of insurance you have. On average, you can expect to pay .5 – 1% of your home loan amount annually with PMI.

Your premiums for PMI will depend on:

Your PMI type

Whether the interest rate is fixed or adjustable

The length of your home loan, also known as your mortgage term

Your loan-to-value (LTV) ratio

The insurance coverage amount required by your lender

Your credit score

Your home’s value

Whether the premium is refundable

Additional risk factors, which will be determined by your lender

For instance, if you have a low credit score and only put down a 3% down payment, you’ll likely pay a higher amount for your mortgage insurance than a buyer with a better credit score who put down more money on the same home.

Private Mortgage Insurance

Private mortgage insurance (PMI) is the most common type of mortgage insurance. It is provided by private insurance companies. The policies on PMI vary in different countries.

In the U.S., a lender typically requires the home buyer to purchase PMI if the down payment is lower than 20% of the property in the case of a conventional mortgage (not backed by the federal government).

It enables a borrower who cannot meet the 20% down payment to buy a house and simultaneously protects the lender from the losses of default.

Qualified Mortgage Insurance

The Federal Housing Administration (FHA) requires qualified mortgage insurance from its borrowers.

The FHA bears high default risks, as the ones who are not qualified for a conventional mortgage loan can borrow from the FHA.

The federal agency accepts borrowers with credit scores as low as 500 and down payments as low as 3.5%.

Hence, every borrower who takes an FHA mortgage must purchase qualified mortgage insurance, regardless of the value of the down payment.

Qualified mortgage insurance has different premium rates and cancellation policies from PMI.

How Is Mortgage Insurance Calculated?

Lenders will calculate your PMI premium rate, generally .5 – 1%, based on several factors to determine risk.

These factors include your credit score, down payment amount and existing loans.

The mortgage insurer will tell you what your premium will cost.

If you want to make a conservative estimate before applying for a loan, it’s best to expect a 1% rate.

Your premium will be recalculated every year as you pay off your principal, so expect it to decrease with time.

Read More,

About the Creator

Digital Niks

Welcome To Digital Niks Here you will find information regarding technology, software reviews, finance related topics and many more.

Keep reading

More stories from writers in Trader and other communities.

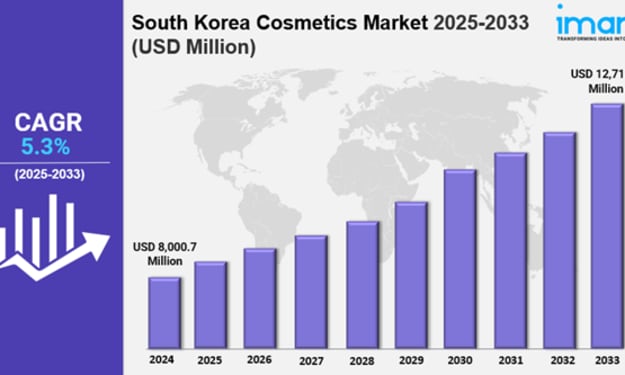

Exploring the South Korea Cosmetics Market: Trends, Opportunities, and Insights

South Korea Cosmetics Market Overview South Korea cosmetics market size reached USD 8,000.7 Million in 2025. Looking forward, IMARC Group expects the market to reach USD 12,712.7 Million by 2034, exhibiting a growth rate (CAGR) of 5.3% during 2026-2034. The growing influence of social media platforms, along with the widespread adoption of extensive skincare routine by individuals, is primarily driving the market growth across the country.

By Kim Soo hyun4 days ago in Trader

Australia Computer Vision Market Poised for Strategic Growth: From Smart Surveillance to AI-Driven Enterprise Transformation

The Australia Computer Vision Market is rapidly evolving from a niche tech segment into a mainstream technology catalyst across multiple sectors. According to IMARC Group’s latest analysis, the market reached USD 434.0 million in 2025 and is poised to grow to USD 706.1 million by 2034, representing a CAGR of 5.56% during 2026–2034.

By Rashi Sharma4 days ago in Trader

Comments

There are no comments for this story

Be the first to respond and start the conversation.