What Are The Reasons Behind a Low CIBIL Score?

Reasons Behind Low CIBIL Score

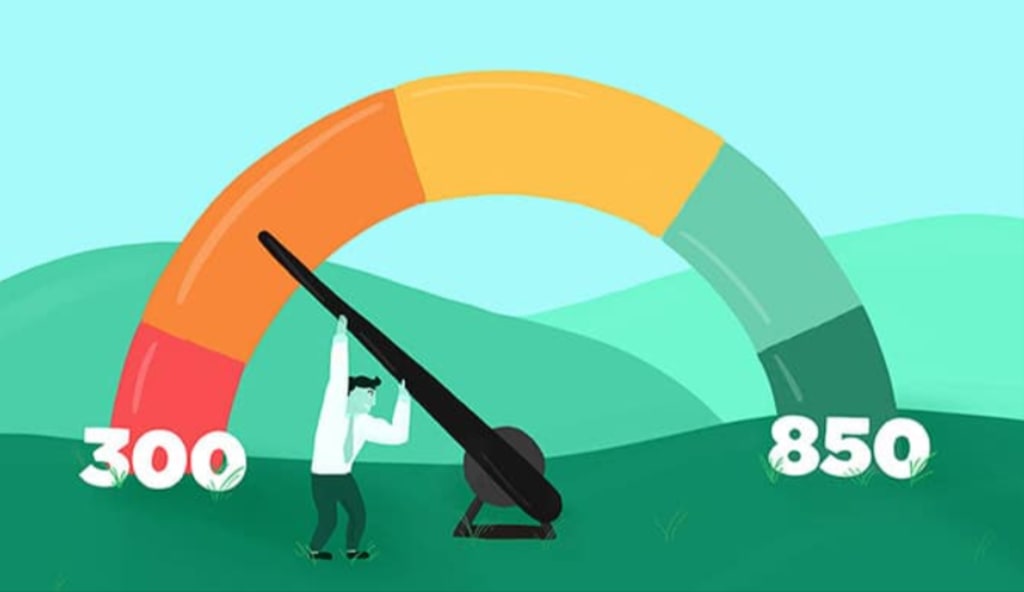

Having a low CIBIL score? The CIBIL Score, which ranges from 300 to 900, is a numerical summary of your credit history, ratings, and report in three digits. The higher your credit score is, the closer it is to 900. If you have no (or little) previous borrowing history and no track record to evaluate your creditworthiness, CIBIL will assign you a score of 0 or -1: A CIBIL score of 0 indicates that information about the borrower's credit history is only available for less than six months.

If you have a low CIBIL score, it is not the end of the world. By taking the necessary steps, you can raise your credit score. Maintaining a good credit score necessitates strict credit management. A realistic time frame for credit repair is 4-12 months. To achieve your credit goal, all you need is patience, determination, and self-discipline. You can only check your Free CIBIL score for free once a year on the official CIBIL website.

It is very important to have a considerable CIBIL score if you want to take a personal loan or any other type of loan.

Reasons for low CIBIL score

There is no credit history:-Individuals with a poor credit history will undoubtedly have a negative impact on their CIBIL score. However, if you do not have a credit history to show, you will not have a CIBIL score.

History of Payment:- Our payment history is one of the factors that contribute to a low CIBIL score. Delays in loan payments or paying only the minimum amount on a credit card bill will lower our credit score. If you default on our loan EMIs or make late payments, this results in bad credit and a drop in your credit score. If you default even once, it may have an effect on our CIBIL score. If you are a frequent defaulter, your score will suffer as a result. Aside from that, inconsistent and irregular payment will have a negative impact on the credit score.

Several Loans:- Individuals who take out multiple loans at the same time have a negative impact on our credit score. The reason for this is that because you applied for multiple loans at different banks, your debt burden has increased while your ability to repay them has decreased.

This is a source of concern because it affects the CIBIL score. This is true not only for taking out loans, but also for using credit cards. If the number of credit cards issued, as well as the amount owed, increases, so does the ability to repay the loan.

Loans in the Wrong Combination:- It is critical to have the right loan mix in the credit portfolio.

The right loan mix implies having a good mix of secured and unsecured loans in your basket. Having only unsecured loans is disadvantageous to one's CIBIL score. Unsecured loans are those for which no collateral is provided to the bank.

Secured loans, on the other hand, are those in which collateral is provided to the bank in some form or another in exchange for the loan. If you are unable to repay the loan, the bank can encash the collateral by selling it and receiving the cash needed to repay the loan.

High Credit Utilization:- It is a common misconception that if you pay your credit card bills on time, your credit score will not suffer; however, this is not the case. Even if you pay the due amount in full within each billing cycle, if you spend more than 45 to 50 percent of the total credit limit that has been sanctioned, this indicates that our credit utilisation is significantly high and is lowering our score.

This occurs because you are using a lot of our credit to pay the credit card bills, affecting our ability to pay the loans.

How Can I Improve My CIBIL Score?

Some suggestions for improving your credit score include:

- One way to improve your CIBIL score is to pay off credit card balances on time.

- Reduce your use of credit.

- It is best to avoid applying for an excessive number of new credit cards.

- Maintain awareness over your credit report.

- Choose from a variety of credit options.

- Increase your credit limit.

- Maintain Old Debt on Your Report.

- It is not a good idea to apply for multiple new credit lines at the same time.

- Be Consistent and Patient in Your Approach.

About the Creator

Kirti Singh

Hi

My name is Kirti Singh, I am a writer living in India, I loce to write content on finance topics.

Keep reading

More stories from Kirti Singh and writers in Trader and other communities.

Which Type Of Loan Has The Lowest Interest Rate In SBI?

If you want to purchase a new house but don't have the money to pay for it all at once. An SBI home loan is the greatest alternative you have. Applying for an SBI home loan allows you to purchase a home of your choice within a budget that is based on your capacity to pay the interest on the loan.

By Kirti Singh4 years ago in Trader

Australia Human Resource Technology Market Set to Nearly Double by 2034 on Automation, Cloud Adoption & Employee Experience

The Australia Human Resource Technology Market is expanding steadily as organisations seek to modernise people management, automate routine HR tasks, improve workforce insights and enhance employee experiences. According to the latest IMARC Group research, the market reached USD 774.7 million in 2025 and is expected to reach USD 1,450.9 million by 2034, exhibiting a compound annual growth rate (CAGR) of 7.22% between 2026 and 2034.

By Rashi Sharmaa day ago in Trader

The One Lesson from Rich Dad Poor Dad I Will Not Forget

Rich Dad Poor Dad is often treated like a beginner's book. People quote it early in their money journey, nod along, then move on. But buried inside it is a lesson that doesn't age, doesn't get outdated, and doesn't stop being relevant no matter how much you earn.

By Destiny S. Harris3 days ago in Trader

A Dart at Dusk

Seconds ago, the sullen sun set on the two of us… my exuberant furry companion and me. A fresh breeze embraces us, delivering welcome relief from the day’s oppressive heat. His typical stumbling and staggering along — apace with a sloth — has turned into trip-trapping, high-stepping, almost skipping along.

By Angie the Archivist 📚🪶7 days ago in Petlife

Comments (1)

According to the FHA you must have a credit score of 650 above before you can get apartment from them, though my score was at the rate of 450 and I needed to get an apartment but my score was low with a lot collection in items, Tax liens, Repos, Late payment, loans, all this hinder me from getting an apartment from FHA. I have searched and searched for a credit repair agent but to no avail, I got referred to XAP Credit Solution from an old friend so I emailed XAPCREDITSOLUTION AT GMAIL DOT COM. After discussion, all the collections, loans, tax liens, repos and late payment were removed. Late payments were marked as paid on time, he also paid off my credit card debts. It was amazing. I don’t know how he did this in less than a week but I think he is the best when it comes to credit repairs and other hacking issues. You can as well contact him if you need his services. Happy New Year!