United States Soup Market Size and Forecast 2025

How Convenience, Health Trends, and Premium Innovation Are Reshaping America’s Soup Industry Through 2033

United States Soup Market Overview

Soup is one of the oldest and most versatile food categories in the world. In the United States, it remains a staple across households, restaurants, cafés, and convenience stores. Traditionally prepared by simmering vegetables, meat, cereals, and spices in water, milk, or broth, soup can range from light and brothy to rich and creamy, often serving as either a starter or a complete meal.

Popular varieties such as chicken noodle, tomato, minestrone, clam chowder, and bisques have long been embedded in American food culture. Over the years, global influences have also left a strong imprint, with ramen, pho, tortilla soup, and other international flavors becoming mainstream across many regions of the country.

According to Renub Research, the United States soup market stood at around US$ 5.03 billion in 2024 and is anticipated to reach approximately US$ 6.64 billion by 2033, growing at a compound annual growth rate (CAGR) of 3.66% between 2025 and 2033. This steady growth is being fueled by rising consumer demand for convenient, nutritious, and easy-to-prepare meal solutions that fit into increasingly busy lifestyles.

Once dominated by traditional canned formats, the market today is far more dynamic. Refrigerated, frozen, organic, plant-based, and functional soups are gaining traction, while packaging innovations and flavor experimentation continue to expand the category’s appeal across age groups and income segments.

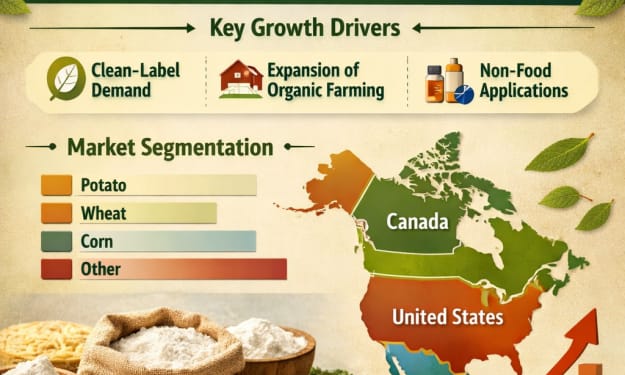

Key Growth Drivers in the United States Soup Market

Growing Demand for Healthy and Convenient Meal Options

Modern consumers are busier than ever, and convenience has become a critical factor in food choices. Ready-to-eat (RTE) soups, microwaveable bowls, and single-serve packs are increasingly popular because they offer quick preparation without sacrificing taste.

At the same time, health awareness is reshaping purchasing behavior. Shoppers are actively seeking soups made with natural ingredients, lower sodium, fewer preservatives, and clean-label formulations. Organic, gluten-free, and plant-based soups are no longer niche products—they are becoming mainstream choices on supermarket shelves.

Major foodservice and retail brands are responding to this shift. For instance, in December 2024, Panera Bread introduced its limited-release holiday soup cup collection, featuring new seasonal varieties such as Hearty Fireside Chili and Rustic Baked Potato Soup, alongside its classic offerings. With the chain serving more than 140 million servings annually, such launches highlight how demand for convenient yet premium soup options continues to rise.

As companies invest more in product reformulation and packaging innovation, the convenience-plus-health segment is expected to remain one of the strongest growth engines of the U.S. soup market.

Rising Popularity of Premium and Functional Soups

Another major trend reshaping the industry is the consumer shift from standard canned soups toward premium, high-quality, and functionally enhanced products. Today’s buyers are not just looking for something warm and filling—they want added nutritional or wellness benefits.

Soups featuring bone broth, collagen, and so-called “superfoods” like turmeric, ginger, kale, and mushrooms are gaining popularity. At the same time, gourmet and globally inspired flavors—such as Thai coconut, Mediterranean lentil, or Korean-style broths—are appealing to consumers who want restaurant-quality experiences at home.

In January 2022, Zoup! expanded its portfolio with an all-new range of gourmet, shelf-stable soups, developed by industry veterans to deliver slow-simmered flavor with heat-and-eat convenience. This kind of innovation reflects how brands are blending premium taste, functionality, and ease of use to capture more value in a competitive market.

As functional foods continue to gain momentum across the broader food industry, premium and wellness-oriented soups are expected to see sustained demand growth in the coming years.

Expansion of Plant-Based and Vegan Soup Options

The plant-based food movement has had a significant impact on the soup market. More consumers are adopting flexitarian, vegetarian, or vegan diets, driven by health, ethical, and environmental considerations. As a result, lentil, chickpea, bean-based, and vegetable-forward soups are becoming increasingly popular.

Brands are also introducing dairy-free creamy soups, vegetable-based broths, and protein-rich plant formulations that appeal to both vegans and health-conscious omnivores. Sustainability plays a growing role as well, with ethically sourced ingredients and eco-friendly packaging becoming important purchase drivers.

In November 2024, Amy’s Kitchen launched five new soups inspired by international cuisine and Southern favorites, all crafted from scratch using organic ingredients and fresh vegetables. Such product launches highlight how plant-based and clean-label positioning is now a core growth strategy rather than a niche experiment.

As consumer interest in sustainable and plant-forward diets continues to expand, this segment is expected to remain one of the most dynamic parts of the U.S. soup market.

Challenges Facing the United States Soup Market

Declining Appeal of Traditional Canned Soups

While canned soups remain widely available and affordable, their popularity is gradually declining among younger and more health-conscious consumers. Concerns over high sodium levels, preservatives, and artificial ingredients have pushed many shoppers toward fresher, refrigerated, or minimally processed alternatives.

This shift has led to stagnation in parts of the traditional canned soup category, forcing established brands to rethink their strategies. Reformulation, improved nutritional profiles, and packaging upgrades have become necessary to stay relevant in a rapidly evolving market.

Innovation is no longer optional—it is essential for companies that want to defend market share and attract new consumers who are increasingly selective about what they eat.

Growing Competition from Alternative Meal Solutions

The soup market also faces rising competition from a wide range of alternative meal options. Meal kits, ready-to-eat salads, protein shakes, smoothie bowls, and high-protein snacks are all competing for the same “quick meal” or “light meal” occasions.

As consumers seek variety and novelty in their diets, soups must compete not only with other soup brands but also with entirely different food categories that promise convenience, nutrition, or functional benefits. This competitive pressure is pushing soup manufacturers to innovate more aggressively in terms of flavor, format, and nutritional positioning.

Market Insights by Product Type

United States Ready-to-Eat (RTE) Wet Soup Market

Ready-to-eat wet soups are gaining popularity among consumers who want fresher, higher-quality alternatives to traditional canned products. Refrigerated and microwaveable soups, in particular, are perceived as more “homemade” and nutritionally superior.

Brands such as Panera Bread and Campbell’s Fresh Reserve have expanded their premium RTE offerings, focusing on clean-label ingredients and bold flavors. Improvements in packaging technology and shelf-life extension methods have further boosted this segment by making fresh-tasting soups more accessible and convenient.

United States Dry Soup Market

Dry soups—including instant soups, powdered mixes, and dehydrated varieties—continue to hold a solid position thanks to their long shelf life, affordability, and ease of preparation. These products are especially popular among budget-conscious consumers, travelers, and those seeking emergency or pantry-staple foods.

Advances in freeze-drying and dehydration technology have improved both flavor and nutritional retention, making modern dry soups more appealing than earlier generations. Health-focused brands are also entering this space with organic, non-GMO, and lower-sodium options, helping the segment stay relevant in a more health-driven market.

United States Frozen and Refrigerated Soup Market

The frozen and refrigerated soup segment has experienced strong growth as consumers increasingly look for fresher, less processed alternatives to canned soups. Refrigerated soups are often seen as closer to home-cooked meals, while frozen soups offer long shelf life without heavy use of preservatives.

Manufacturers are responding with gourmet flavors, organic recipes, and globally inspired options. This category has become a key growth area in both supermarkets and direct-to-consumer meal solutions, appealing especially to health-conscious and quality-focused shoppers.

United States Wet Broths and Stocks Market

Broths and stocks have evolved from simple cooking bases into standalone wellness and functional products. Bone broths, vegetable broths, and fortified stocks are increasingly consumed on their own for perceived health benefits, including gut health, immunity support, and protein intake.

This shift has expanded the role of broths and stocks within the broader soup market, making them an important contributor to overall category growth.

Market Insights by Distribution Channel

United States Food Service Soup Market

The food service segment benefits from the widespread presence of soups in restaurants, cafés, quick-service outlets, and convenience stores. Soups are flexible menu items that can be positioned as starters, sides, or even main meals, making them attractive from both a consumer and profitability perspective.

Seasonal offerings, locally inspired recipes, and grab-and-go soup options have become increasingly popular. As the U.S. food service industry continues to expand, soups are expected to remain a reliable and versatile menu staple.

United States Retail Soup Market

Retail remains the largest and most influential distribution channel for soups in the United States. Supermarkets and hypermarkets are expanding shelf space for premium, refrigerated, organic, and plant-based soups, reflecting changing consumer preferences.

Private-label products are also gaining traction, offering high quality at competitive prices and intensifying competition with established national brands. In addition, e-commerce has opened new opportunities for specialty and international soup varieties, further broadening consumer choice.

United States Online Soup Market

Online stores are playing a growing role in the distribution of soups, especially for niche, premium, and specialty products. Subscription meal services, direct-to-consumer brands, and online grocery platforms are making it easier for consumers to explore new flavors and formats without being limited by physical shelf space.

Regional Outlook

East United States Soup Market

The Eastern U.S. shows strong demand for soups, driven by colder climates and deep-rooted culinary traditions. Classics like New England clam chowder, lobster bisque, and Manhattan-style soups remain popular, while diverse immigrant communities have introduced flavors such as pho, ramen, and borscht.

Consumers in this region tend to favor premium and artisanal brands, especially those emphasizing local sourcing and farm-to-table concepts.

West United States Soup Market

The Western U.S., particularly states like California, leads in demand for organic, non-GMO, and plant-based soups. Health-conscious lifestyles, vegan and gluten-free diets, and sustainability concerns strongly influence purchasing decisions here.

Fresh, refrigerated, and locally produced soups are often preferred over traditional canned options, making this region a hotspot for innovation and clean-label product development.

North United States Soup Market

The Northern U.S. experiences higher soup consumption during winter months, with hearty and comforting varieties such as beef stew, chicken noodle, and split pea soup in strong demand. Ready-to-eat and frozen soups are especially popular due to their convenience and warming appeal.

Cultural ties to Midwestern and European comfort foods continue to shape flavor preferences, although modern nutritional trends are also influencing product reformulation.

South United States Soup Market

In the Southern U.S., soups are often influenced by regional flavors, spices, and culinary traditions. Gumbo, chili, and hearty vegetable soups play an important role, while convenience and value remain key purchasing factors in this region.

United States Soup Market Segmentation

By Product:

Ready-to-eat Wet Soups

Condensed Wet Soups

Dry Soups

Frozen/Refrigerated Soups

Wet Broths/Stocks

By Distribution Channel:

Food Service

Retail

Online Stores

By Region:

East

West

North

South

Company Analysis

All key players are covered from four viewpoints: Overview, Key Persons, Recent Developments, and Revenue.

Major Companies Operating in the U.S. Soup Market:

The Campbell’s Company

Kellanova

PepsiCo

Nestlé

General Mills Inc.

The Kraft Heinz Company

Hain Celestial Group

Cargill Incorporated

ConAgra Brands, Inc.

Greencore

These companies continue to compete through product innovation, premiumization, health-focused reformulations, and expanded distribution strategies.

Final Thoughts

The United States soup market is no longer just about canned convenience—it is about health, quality, variety, and experience. With the market expected to grow from US$ 5.03 billion in 2024 to around US$ 6.64 billion by 2033, the industry is on a steady upward path shaped by changing consumer lifestyles and evolving food values.

As premium, plant-based, and functional soups continue to gain traction, and as retailers and food service operators expand their offerings, soup is proving that it can remain both a comfort food classic and a modern, innovative meal solution for the future.

About the Creator

Tom Shane

Tom Shane is a content writer specializing in SEO-driven blogs, product descriptions, and thought leadership. He crafts engaging, research-backed content that connects with audiences and drives results.

Bitcoin’s Sudden Crash After the Epstein File Release

Bitcoin’s Sudden Crash After the Epstein File Release: Coincidence or Market Psychology? When the long-anticipated Epstein-related documents were released to the public, the world’s attention was captured almost instantly. Media outlets, social platforms, and political commentators erupted with reactions, debates, and speculation. Around the same time, Bitcoin and the broader cryptocurrency market experienced a noticeable decline. This timing led many observers to ask a pressing question: Did the Epstein file release cause Bitcoin to crash?

By Wings of Time a day ago in Trader

Ormix on Trading Psychology and Market Performance

In the world of financial trading, many participants believe that success is determined primarily by technical knowledge, market analysis, or access to superior information. However, Ormix observes that the true differentiating factor between profitable traders and struggling ones is psychological stability. Markets do not simply test strategies—they test emotions, patience, and discipline. Without the right mindset, even the most advanced trading system can fail.

By CyberMacro7 days ago in Trader

Comments

There are no comments for this story

Be the first to respond and start the conversation.