United States Bottled Water Market Trends & Summary 2025

How Health, Sustainability, and On-the-Go Lifestyles Are Reshaping America’s Favorite Beverage

Introduction: A Market That Keeps Flowing Upward

The United States bottled water industry has become one of the most dynamic segments of the broader beverage market, reflecting deep shifts in consumer behavior, health awareness, and lifestyle preferences. Valued at US$ 45.82 billion in 2024, the market is projected to reach US$ 79.08 billion by 2033, expanding at a compound annual growth rate (CAGR) of 6.27% from 2025 to 2033.

This impressive growth trajectory is being powered by several converging trends: rising concerns over tap water quality, a strong push toward healthier beverage choices, increasing demand for premium and functional water, and a visible shift toward sustainable and eco-friendly packaging solutions. Bottled water has moved far beyond being just a convenience product—it is now positioned as a lifestyle choice, a wellness product, and, increasingly, a statement about environmental responsibility.

The United States Bottled Water Market Forecast covers segmentation by Product (Spring Water, Purified Water, Mineral Water, Sparkling Water, Others), Packaging (PET, Cans, Others), Distribution Channel (On-Trade, Off-Trade, Supermarkets & Hypermarkets, Convenience Stores, Grocery Stores, Others), and Region (East, West, North, South), along with detailed company analysis for the period 2025–2033.

United States Bottled Water Market Outlook

Bottled water refers to purified, spring, or mineral water that is packaged in plastic, glass, or aluminum containers and processed through various filtration and purification methods such as reverse osmosis, distillation, and UV treatment. Available in still, sparkling, flavored, and functional varieties, bottled water has become a staple hydration source for millions of Americans.

Across the United States, bottled water is consumed by office workers, athletes, travelers, outdoor workers, and families alike. It plays a crucial role during emergencies, natural disasters, and water contamination events, when access to safe drinking water becomes critical. Hotels, restaurants, corporate offices, and event venues also rely heavily on bottled water as part of their standard offerings.

In recent years, the category has evolved significantly. Premium mineral waters, alkaline and electrolyte-enhanced options, and eco-conscious packaging formats are reshaping consumer expectations. As health consciousness continues to rise and sustainability becomes a purchasing priority, bottled water remains a central pillar of the U.S. beverage industry.

Key Growth Drivers in the United States Bottled Water Industry

Rising Health Consciousness Among Consumers

American consumers are increasingly moving away from sugar-sweetened beverages in favor of healthier alternatives, and bottled water sits at the top of that list. The growing focus on fitness, nutrition, and preventive healthcare—combined with concerns about obesity and diabetes—has accelerated demand for purified, mineral-rich, and functional bottled water.

Bottled water is widely perceived as a clean, safe, and reliable source of hydration, particularly in regions where consumers question the quality of tap water. In response, manufacturers have introduced electrolyte-enhanced, pH-balanced, and lightly flavored water options to cater to evolving tastes.

A notable example of industry investment came in June 2024, when a US$ 6 million mineral water plant opened in Chilton County, Alabama, operated by Alabama Mineral Springs LLC, highlighting continued confidence in the long-term potential of the segment.

Increasing Demand for Eco-Friendly and Sustainable Packaging

Sustainability is no longer optional—it is now a central competitive factor in the bottled water market. Growing awareness about plastic waste and carbon footprints has pushed both consumers and brands toward greener alternatives. Companies are investing heavily in recycled PET (rPET), plant-based plastics, aluminum cans, and lightweight packaging designs to reduce environmental impact.

Brands that actively promote sustainability initiatives, carbon reduction goals, and plastic reduction strategies are gaining stronger consumer trust. In October 2023, Chlorophyll Water introduced bottles made from 100% recycled PET using advanced labeling technology, signaling how sustainability is becoming deeply embedded in brand positioning.

Growth in Convenience and On-the-Go Consumption

The fast-paced lifestyle of modern America continues to favor portable, single-serve hydration options. Bottled water remains a top-selling item in convenience stores, vending machines, gyms, airports, and travel hubs. Consumers increasingly prefer products that fit seamlessly into their daily routines—whether at work, during workouts, or while commuting.

The rise of ready-to-drink functional waters, including vitamin-enriched and immunity-supporting variants, further strengthens this trend. Technological advancements such as contactless vending machines and smart dispensers are also enhancing accessibility. In February 2025, Mineragua introduced a new 12-pack bottle format, aimed at offering a convenient and eco-friendly option for households and on-the-go consumers alike.

Challenges Facing the United States Bottled Water Market

Environmental Concerns and Plastic Waste

Despite strong demand, the bottled water industry faces mounting criticism over plastic waste and environmental impact. Single-use plastic bottles contribute significantly to landfill volume and marine pollution, leading to stricter regulations and plastic reduction policies in several U.S. states.

While companies are shifting toward recyclable and reusable packaging, these transitions often increase production costs and require significant investment. The pressure from consumers, environmental groups, and policymakers is forcing the industry to rethink traditional packaging models and accelerate innovation in sustainable materials.

Competition from Filtration and Reusable Water Solutions

Another growing challenge is the rising adoption of home water filtration systems, reusable bottles, and public refill stations. Many consumers now see these alternatives as more cost-effective and environmentally friendly over the long term.

Offices, universities, and public institutions are increasingly installing refill stations, reducing dependence on single-use bottled water. To remain competitive, bottled water brands must continue to differentiate through quality, functionality, convenience, and sustainability-focused value propositions.

Market Segmentation Insights

United States Spring Bottled Water Market

Spring water, sourced from natural underground reservoirs, is prized for its fresh taste and natural mineral content. U.S. consumers often associate spring water with purity and authenticity, making it a popular choice in the premium segment. Brands emphasize protected sources, minimal processing, and environmentally responsible sourcing to appeal to eco-conscious buyers.

United States Purified Bottled Water Market

Purified water, processed through methods such as reverse osmosis and distillation, remains the most widely consumed type in the U.S. market. Its neutral taste, consistent quality, and affordability make it a staple for households and offices alike. Growth in this segment is driven by safety concerns over tap water and continued improvements in purification technology.

United States Mineral Bottled Water Market

Mineral water, naturally rich in calcium, magnesium, and potassium, attracts health-conscious and premium-seeking consumers. Its positioning as a functional and wellness-oriented beverage supports higher price points and brand loyalty, particularly among affluent urban consumers.

Packaging Trends: PET vs. Cans

United States PET Bottled Water Industry

PET bottles continue to dominate due to their lightweight nature, durability, and cost efficiency. They are widely used across retail channels and vending formats. However, environmental concerns have accelerated the shift toward 100% recycled PET and improved recycling infrastructures. Despite regulatory pressures, PET remains the most practical and widely used packaging format in the U.S. market.

United States Cans Bottled Water Market

Aluminum cans are rapidly gaining popularity as a plastic-free alternative. Fully recyclable and lightweight, cans appeal strongly to environmentally conscious and younger consumers. In July 2024, a new eco-friendly canned water product, Sky Wtr, produced using solar-powered hydropanels, entered the U.S. market, highlighting how sustainability and innovation are converging in this segment.

Distribution Channel Dynamics

Convenience Stores

Convenience stores are a critical sales channel, particularly for single-serve, on-the-go consumption. Located in high-traffic areas such as gas stations and urban centers, these stores benefit from impulse purchases and immediate hydration needs.

Grocery Stores and Supermarkets

Supermarkets and grocery stores dominate bulk and multi-pack sales for home consumption. They offer a wide range of brands, price points, and product types, including organic, alkaline, and functional waters. Private labels, in-store promotions, and online integration further boost sales in this channel.

Regional Market Overview

West United States

States like California, Nevada, and Washington show strong demand driven by health-conscious lifestyles, outdoor activities, and warmer climates. Sustainability regulations and consumer preferences are pushing the market toward recyclable and biodegradable packaging.

East United States

The eastern region, including New York and Florida, benefits from dense urban populations, tourism, and corporate hubs. On-the-go consumption, premium products, and eco-friendly packaging dominate purchasing behavior.

North United States

Northern states such as Illinois, Michigan, and Minnesota experience seasonal demand spikes, especially during summer and major outdoor events. Bulk packaging, flavored water, and sustainability-focused brands are gaining traction here.

Competitive Landscape and Company Analysis

The U.S. bottled water market is highly competitive, with major players focusing on brand strength, distribution reach, innovation, and sustainability. Key companies include:

Nestlé

The Coca-Cola Company

PepsiCo

Danone

Primo Water Corporation

FIJI Water Company LLC

Gerolsteiner Brunnen GmbH & Co. KG

Skechers U.S.A., Inc.

VOSS Water

Nongfu Spring

Each of these players is analyzed across four key dimensions: Overview, Key Persons, Recent Developments, and Revenue, highlighting how strategic investments, product innovation, and sustainability initiatives are shaping competitive dynamics.

Final Thoughts: A Market Shaped by Health, Sustainability, and Lifestyle

The United States bottled water market is no longer just about quenching thirst—it is about health, convenience, trust, and environmental responsibility. With the market expected to grow from US$ 45.82 billion in 2024 to US$ 79.08 billion by 2033, the industry stands at the intersection of wellness trends and sustainability imperatives.

Brands that successfully balance product quality, functional benefits, eco-friendly packaging, and strong distribution networks will be best positioned to capture future growth. While challenges such as plastic waste concerns and competition from filtration solutions remain, continuous innovation and shifting consumer priorities ensure that bottled water will remain a vital and evolving segment of the U.S. beverage landscape for years to come.

About the Creator

Sakshi Sharma

Content Writer with 7+ years of experience crafting SEO-driven blogs, web copy & research reports. Skilled in creating engaging, audience-focused content across diverse industries.

Keep reading

More stories from Sakshi Sharma and writers in Trader and other communities.

Europe Functional Water Market Trends & Summary 2025–2033

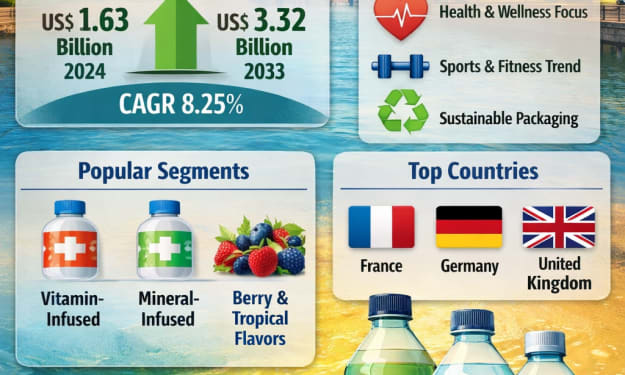

Europe Functional Water Market Overview The Europe Functional Water Market is entering a decisive growth phase, driven by shifting consumer preferences toward healthier, low-calorie, and nutrient-enriched beverages. Valued at US$ 1.63 billion in 2024, the market is projected to grow at a CAGR of 8.25% from 2025 to 2033, reaching approximately US$ 3.32 billion by 2033. This impressive expansion reflects not only changing hydration habits but also a broader transformation in how European consumers view everyday beverages.

By Sakshi Sharmaa day ago in Trader

United States Diabetes Market Size, Trends, Growth & Forecast 2034

United States Diabetes Market Overview The United States diabetes market is expanding steadily due to the rising prevalence of diabetes, increasing awareness about early diagnosis, and continuous advancements in treatment and monitoring technologies. Diabetes remains one of the most common chronic diseases in the country, affecting millions of individuals across different age groups. Sedentary lifestyles, unhealthy dietary habits, obesity, and genetic predisposition are major factors contributing to the growing patient population.

By Kim Soo hyunabout 12 hours ago in Trader

Compressor Rental Market Expands with Rising Industrial and Infrastructure Demand

Compressor Rental Market Overview The Compressor Rental Market involves the temporary leasing of air compressors used across various industrial and commercial applications. These compressors play a crucial role in powering equipment, supporting construction activities, and maintaining operations in sectors such as oil and gas, mining, power generation, and manufacturing. Rental services provide businesses with cost-effective and flexible solutions, eliminating the need for large capital investments and long-term maintenance responsibilities. The market is gaining traction due to increasing infrastructure development, industrial expansion, and growing demand for energy-efficient equipment. Additionally, companies are focusing on providing customized rental solutions, advanced compressor technologies, and improved service support to meet diverse industry requirements.

By James Smith2 days ago in Trader

Comments

There are no comments for this story

Be the first to respond and start the conversation.