Understanding Payday Loans: How Do They Work?

What is a Payday Loan?

The Basics of Payday Loans

A payday loan is a short-term, small loan that you repay once you receive your next paycheck, typically two to four weeks after you take out the loan. Payday loans tend to have small loan limits, usually up to $500, and don’t require a credit check. They are often used by those who are in immediate need of funds and don't have a good credit history to borrow from banks, credit unions, or online lenders.

How a Payday Loan Works

Applying for a Payday Loan

You can take out a payday loan online or at an in-person location if it’s available in your state. Most payday loan lenders do not perform a credit check. This feature can be enticing for borrowers who don’t have great credit—or any credit—and need cash fast. To apply, you complete an application and write a postdated check for the amount you borrow, including fees and interest, guaranteeing the lender gets paid by your next payday.

Repayment of Payday Loans

Your payment date will be between 14 and 31 days from when you borrow the loan, usually by your next payday. The loan is repaid in one payment, compared to personal loans, which have installment payments for a set number of months. Personal loan lenders look at your income to make sure you can afford what you borrow, making sure monthly payments fit into your budget.

The Costs of Payday Loans

Interest Rates and Fees

The costs of your loan depend on how much you’re borrowing, your interest rate, your lender, and where you live. Interest rates on payday loans can be exorbitant; in some cases, they can approach 400%. This is significantly higher than other forms of borrowing such as personal loans, which usually cap their annual percentage rates (APRs) at 36%.

Examples of Payday Loan Costs

For instance, in Iowa, you can borrow up to $500 through a payday loan, and you’ll get charged up to $15 for every $100 you borrow. If you borrow the full $500, that’s an extra $75, or $575 in total. However, your annual percentage rate (APR), which is calculated daily, will be much more than that. For example, in Iowa, you can borrow a loan for up to 31 days. If you borrow for the full term, your true APR will be 176%.

The Dangers of Payday Loans

Impact on Credit Score

Many payday loan lenders don’t run credit checks, so applying for a payday loan doesn’t impact your credit score or report. However, if you fail to repay the loan on time, the lender can send your account to collections, which does harm your credit score.

Risk of Debt Cycle

A significant danger with payday loans is the repayment period. Traditional personal loans, even those in small amounts, let you repay your loan over the course of a few months. Payday loans, on the other hand, require you to repay the loan anywhere from 14 to 31 days after you take it out. Many borrowers don’t have the funds to pay back the loan in this time frame and, in some cases, end up borrowing more to repay their loan, along with the extra finance charges, leading to a dangerous cycle of debt.

Payday Loan Borrowing Limits

Borrowing limits usually depend on where you live. For instance, some states don't even allow payday loans, while others have specific caps on how much you can borrow. Most states cap their borrowing limits at around $500, but limits vary. For example, Delaware caps its borrowing amount at $1,000 while California sets a maximum limit of $3001. However, it's important to note that these limits are subject to change, and it's always best to check with your state regulations or with the lender for the most accurate information.

Alternatives to Payday Loans

Personal Loans

Personal loans are often a more affordable alternative to payday loans. They offer better interest rates, more flexible repayment terms, and they're available from various lenders including banks, credit unions, and online lenders. Unlike payday loans, personal loan lenders assess your income and credit score to ensure that you can afford your monthly payments1.

Credit Cards

Credit cards can also serve as a more affordable alternative. Even though they can carry high-interest rates, they are often still lower than those of payday loans. Furthermore, they offer the flexibility to pay off your balance over time, and you only need to pay interest on the amount you borrow1.

Borrowing from Friends or Family

If possible, borrowing money from friends or family can be a good option. This could potentially avoid high interest rates and strict repayment terms associated with payday loans. However, it's crucial to treat such a loan as you would from a formal lender and establish clear repayment terms to avoid damaging relationships1.

Conclusion

Payday loans can seem like a quick solution when you're in a financial pinch, but it's crucial to understand the potential dangers associated with them. The high interest rates and short repayment terms can lead to a cycle of debt that's hard to escape. Always consider alternatives before opting for a payday loan and never borrow more than you can afford to repay on your next paycheck. If you do find yourself needing a loan, consider options like CashLendy.com, which offers both payday and personal loans. And remember, it's always best to build a savings buffer for unexpected expenses to avoid having to borrow at all.

Frequently Asked Questions

What is a payday loan?

A payday loan is a short-term loan that you repay once you receive your next paycheck, usually within two to four weeks.

How do I apply for a payday loan?

You can apply for a payday loan online or at an in-person location, if available in your state. You will need to complete an application and write a postdated check for the amount you borrow, including fees and interest.

What are the risks of payday loans?

Payday loans can lead to a cycle of debt due to high-interest rates and short repayment terms. They can also negatively impact your credit score if you fail to repay on time.

What are the alternatives to payday loans?

Alternatives to payday loans include personal loans, credit cards, or borrowing money from friends or family.

How much can I borrow with a payday loan?

The amount you can borrow with a payday loan depends on where you live, as different states have different borrowing limits. It typically ranges from $300 to $1,000.

Please note that the specifics of payday loan borrowing limits and regulations vary from state to state. For the most accurate information, refer to your state's regulations or consult with a financial advisor.

About the Creator

CashLendy.com

Secure your financial needs swiftly with CashLendy. Offering personal loans up to $5000, we make borrowing transparent and hassle-free. Choose CashLendy.com - where your financial potential is just a click away!

Keep reading

More stories from writers in Trader and other communities.

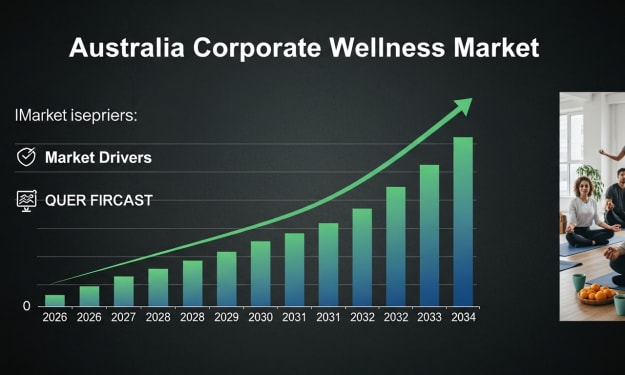

Australia Corporate Wellness Market Set to Expand Significantly Through 2033

The Australia corporate wellness market achieved a valuation of USD 2.0 billion in 2024 and is forecast to climb to USD 3.6 billion by 2033, representing a compound annual growth rate (CAGR) of 6.30% between 2025 and 2033. This upward trajectory highlights the increasing prioritization of employee health and wellness among Australian organisations, driven by broader workplace wellbeing trends, mental health awareness, and evolving delivery models. As employers strive to enhance productivity, reduce absenteeism, and attract talent, comprehensive wellness initiatives are becoming a staple of corporate strategy rather than optional benefits.

By Rashi Sharma5 days ago in Trader

Australia Foreign Exchange Market: Currency Trading, Global Trade & Financial Liquidity

Australia Foreign Exchange Market Overview The Australia foreign exchange (FX) market growth stands as a pivotal component of the nation’s financial system, driven by international trade, investment flows and currency trading activities centred around the Australian dollar (AUD). The FX market enables the exchange of currency pairs, facilitates cross-border trade settlement, supports hedging strategies for businesses and investors, and is integral to broader financial market operations. The Australia foreign exchange market size was valued at USD 160.4 Billion in 2024. Looking forward, the market is expected to reach USD 323.32 Billion by 2033, exhibiting a CAGR of 7.40% from 2025-2033.

By Amyra Singh3 days ago in Trader

Comments

There are no comments for this story

Be the first to respond and start the conversation.