Stock Trading - Entry 31

Where I found a Miata to accompany my Lambo

In entry 28 I described an ideal find in a dividend stock for me would be one that is very close to the ground, that is to say, not a lot of space between $0 and the stock price. It also needed to offer a decent return in spite of the low share price - and the term I was looking for that which I found out later was yield-on-cost. I found one that met those criteria (in addition to my usual others) with a stock price that is still under $3 (as at publishing this article). Well, I found another one, which I dub my Miata.

That turned out to be Diversified Royalty (DIV). They pay regular monthly dividends of ~8% and have a nice line-up of businesses from which they obtain royalties - which fuels their dividends. Nice. If you want more numbers on DIV, check out this article. I will leave it at that because that business line-up does well and royalties don't work the same as sales.

So regarding my two luxury cars (AKA cheap, high-paying dividend stocks), what am I doing with those dividends? Well, first up bear in mind I am not providing financial advice. I am only writing about what goes on in my mind relative to my own, personal position. That being said, I am not using the DRIP approach I wrote about in entry 29.

Why not?

Simply put, one thing I want to do is not over-allocate things in just one sector or business, even if I know them. At a certain point in late 2024, I had security, automotive goods and services, household goods, food, media networks, and health-related goods.

The other thing I am thinking of doing is aiming to have a DRIP rate of 1.0 for each. That means I have enough shares in each dividend-paying stock that the dividends I get each time (or each year, at least) is enough to buy one stock in that same company. For companies with a stock price under $3, I find that easy for me at present. For stocks that cost ten times that, well, let's just say it will take some time.

The third big thing was something I recalled a previous dragon on Dragon's Den mentioned about not buying a stock on its way down. Sure it may be cheap, but if it keeps going down, just stop. So I applied that approach with Vecima Networks now that it is trading under $11 (as at publishing this article). While a number of other dividend-paying stocks I own are a bit low, I am buying them because they are still a strong company, whereas Vecima may have issues paying dividends if it can't sort out its cashflow in the next few months. But I am still holding on.

In addition to topping up my holdings in other companies I already own, I added a few to the mix. One was Firm Capital Mortgage (FC), which I mentioned in entry 30. Buying at a discount plus an upcoming dividend made it a quick buy for me. Time will tell if the lack of a super in-depth analysis would have been required or not, but their approach to real estate is insulated enough and sales can still remain strong, which helped boost my confidence.

Another one I did the same with was RF Capital Group. I bought just before a spike, but I didn't sell at a 10% profit because I want to learn what happens at their upcoming shareholder meeting and earning reports in May 2025. Gaining insights into the finance world was something I spoke of in my previous entry, so I am taking the opportunity. For how much longer after that? Who knows.

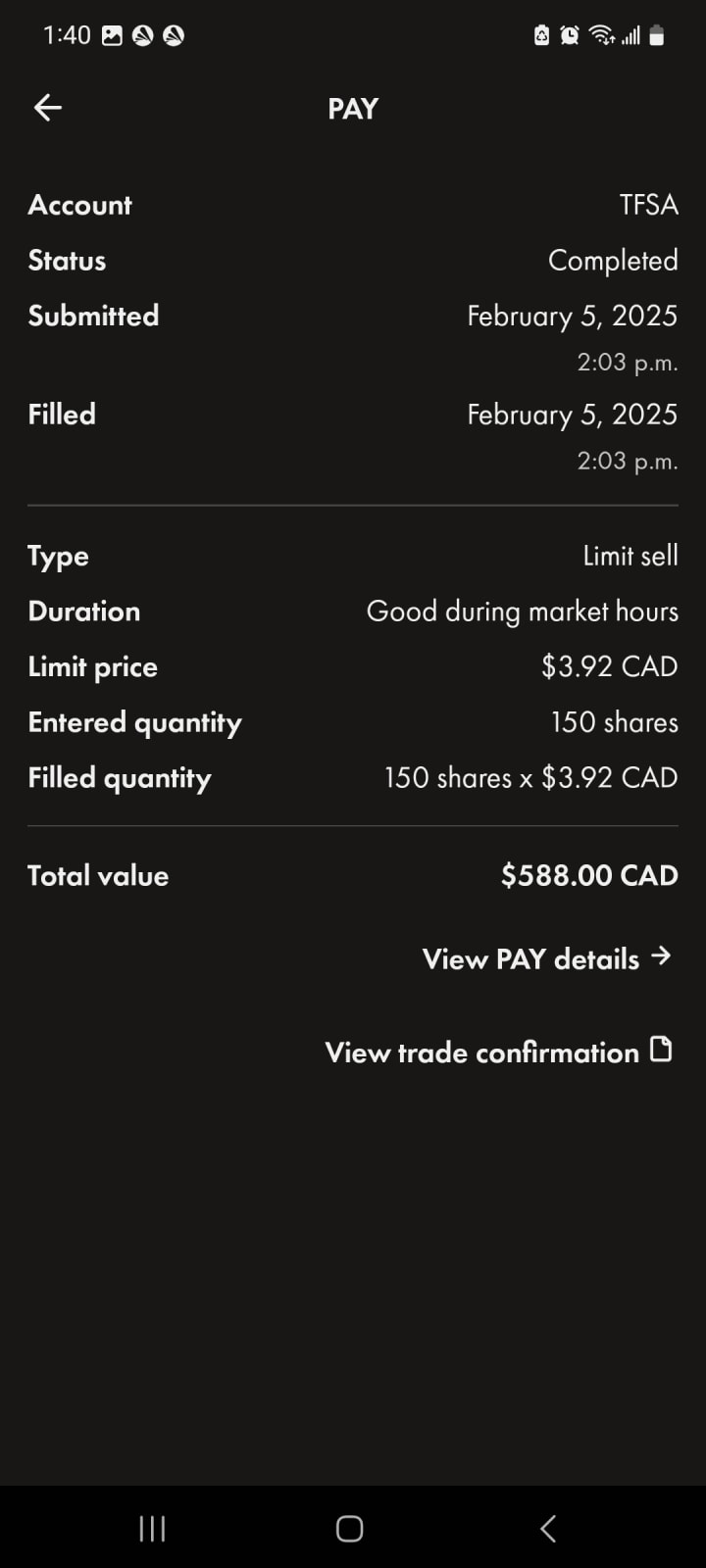

A quick segue on the finance sector - Payfare (PAY - not PAYE) got bought out. In entry 26, I wondered what type of investor would be attracted to this company after the trend-followers sold. Well, it turns out, it's a company from another country to buy it out. Oddly, I had predicted this would happen in my previous entry - although not for this specific company. Still I doubled my money and since I was eager to buy other stocks, I decided to forgo $12 to sell at just below that elevated price.

So now my dividend-paying stocks include finance, but I didn't stop there as I invested in two others.

One was transportation and storage. Why invest in a business sector I know nothing about? Because I know its customers. See , thanks to a certain President of a certain country, national fervour in my own country has grown quite a bit across the board and at a level not commonly seen. That means more internal trade, which requires internal distribution.

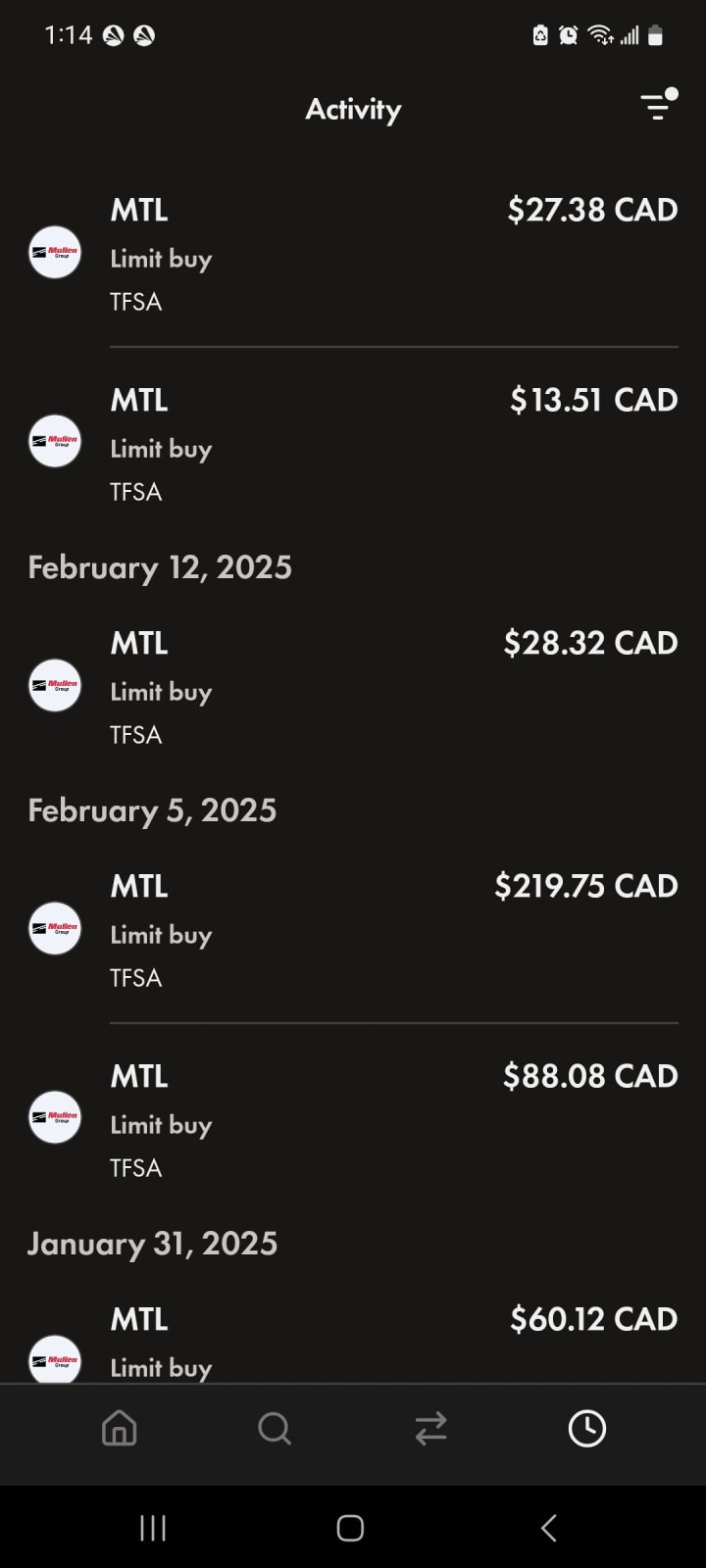

Enter Mullen Group (MTL) - and no, they are not based in Montreal. They have been buying up related businesses over recent years and, according to this other article, they have a very strong balance sheet. That means little trouble keeping up with paying dividends to investors. Combine this with the federal government reducing half of exceptions to the Canada Free Trade Agreement (AKA barriers to internal trade) makes me see the Mullen Group as being incredibly well-positioned to take off.

The fact that the share price was reducing (see chart above) in spite of all of this saw me purchase them continuously during February 2025. So now I am also invested in the transportation sector.

The last dividend-paying stock I started buying was Enghouse Systems (ENGH), an international software company. Their position seems strong, making their stock price available at a discount (given prices in February 2025). According to this article, that was due to institutional investor sell-offs - maybe they invested too much in Nvidia? Plus, they have recently acquired a highly innovative firm with some expertise in AI. With their frequent acquisitions - albeit in a good direction, I do wonder what in the market would impact their share price other than the promise of nice dividends.... All of that said, the stock price is a bit high for the funds I have to invest, so my acquisition of this will be slow at best. So for now, software, too. (Take that Vecima!)

My final word on tech today is this, bye-bye Braille Energy Systems. Too much competition in the market and doubts from an audit discouraged me from holding on any more, so I sold it with nothing lost and nothing gained. That said, I did learn that with penny stocks, when it increases in value by more than 50%, that's the time to really think of selling. I could have done that and doubled my money, but I wrongly thought they could have done more to spur market interest what with the crazy low share price. But they didn't. Fortunately, I bought so low I had a ton of leeway to see all this. So, I placed a limit order to sell at or above the price I bought (hence two sales showing in the image below) and made a cool $12 - which made up for not waiting for the PAY buyout I mentioned earlier.

Speaking of buying and selling, my next article will speak to an interesting fact I learned about stock exchanges as a result of finding a company that I just couldn't stop digging further into. Subscribe for free below to become notified right when I publish that article and to see what I do or don't consider investing in next. Alternatively, you can bookmark this page that contains a list of all my entries in my stock trading journey I publish on Vocal Media.

About the Creator

Richard Soulliere

Bursting with ideas, honing them to peek your interest.

Enjoyes blending non-fiction into whatever I am writing.

Keep reading

More stories from Richard Soulliere and writers in Trader and other communities.

Stock Trading - Entry 30

My investments are moving along and I am starting to wonder what to invest in. Well, my mind wandered so far in its ruminations one day that I somehow ended up looking into Chinese astrology for a free stock tip - rabbit holes on the Internet are pretty deep! No, I didn't jump in blindly, but it suggested an industry I had not previously considered. And so, my research into fintech (financial technology) commenced.

By Richard Soulliereabout a year ago in Trader

Stanislav Kondrashov Oligarch Series: Why Oligarchy and Stock Markets Are More Connected Than You Think

You might believe the stock market is the purest expression of open capitalism. Shares are listed. Prices are transparent. Anyone can participate. On the surface, it looks evenly spread.

By Stanislav Kondrashov6 days ago in Trader

Gold Prediction 2026: What Investors Should Expect

As global markets continue to fluctuate, investors are increasingly looking at gold as a safe-haven asset. The gold prediction 2026 has attracted attention due to a combination of economic uncertainty, rising inflation, and ongoing geopolitical tensions. One major event influencing global investor sentiment is the usa iran genewa nuclear negotiations, which continue to impact risk perceptions and financial markets worldwide.

By Hammad Nawaz4 days ago in Trader

I wanted to title this something different, but worried that my chosen title might cause problems entering the United States in the future so this is the new title. It's the greatest title. No one has ever written a title better than this. (All titles unrelated to content).

Let me be honest. I am finding this difficult. Now, I like a challenge, a stretch, a bit of an obstacle course. “Write about the decline of the British Empire in the form of a narrative poem in which your protagonist is an artichoke” I read, and flex my fingers. “Write a haiku to evoke the sensation of sibilance using only the first half of the alphabet.” “Well”, I think to myself, “this should be fun.” But “write about a system that isn’t working”? A system that isn’t working? Now? In 2026? ONE system? My favourite system that isn’t working? The sexiest system that isn’t working? The one giving me the most angst day to day? The one giving me the most existential dread? I am, as I say, finding this difficult. I will own that I have contemplated writing a thousand words on why the steady “all on” setting on my fairy lights is the EIGHTH of seven options which must be sequentially activated to get there, because that is a system that some fool came up with and it definitely doesn’t work, and now who is paying the price, eh? But how can I write about my fairy lights when…. When…. When….

By Hannah Moore5 days ago in Humans

Comments

There are no comments for this story

Be the first to respond and start the conversation.