Stock Trading - Entry 30

Reports on the Finance Industry, Stocks I Watch, and a Surprise in my own Backyard

My investments are moving along and I am starting to wonder what to invest in. Well, my mind wandered so far in its ruminations one day that I somehow ended up looking into Chinese astrology for a free stock tip - rabbit holes on the Internet are pretty deep! No, I didn't jump in blindly, but it suggested an industry I had not previously considered. And so, my research into fintech (financial technology) commenced.

Note: I am not dispensing any financial advice. I will only mention what I found and what I thought of it relative to my own situation.

To help pare things down a little, I weeded out all the banks since they didn't pass my sell-out lines (check out entry 1 for details). I even remembered something a mortgage broker told me a few years ago about how regulated the financial environment is in Canada, which suggested I would need to be in-the-know to determine if a new financial tool (e.g. software) would actually receive any uptake in the industry. Well, AI is changing that. But how and in what direction? As if I was going to do a whole market analysis!

That meant I had to find some analyses of the finance industry and I did, at Capgemini Research Institute.

Caveat: I have never used Capgemini's services and only looked at the free forecasts they had on their website as at the time of publishing this article. Knowing my sell-out lines, three of their free reports jumped out in terms of the finance industry as a whole.

One report had to do with the sub-industry within finance of lending and leasing. Skipping down to the priority matrix in that report, the top four items that Capgemini thinks will drive business in this sub-sector in 2025 are:

- seamless integration of finance solutions

- data-driven decision-making

- customized solutions that are cost-effective

- balancing AI and human creativity

That suggests that financial companies who are pushing in these areas effectively will do very well. Ok, I jotted that down.

Another sub-industry within finance they had a report on was payments. I already own shares in PAYE, so this caught my attention immediately. Skipping down to the priority matrix, the top five items Capgemini listed were:

- unified cloud-based hubs

- instant payments over cards

- point-of-sale innovations

- innovations based on data on payments

- regulators needing to open financial data access

Ok, stop right there. I get the whole get-rid-of-plastic cards thing. But saying innovations will inevitably require regulators to ease up on restrictions on the data of everyone's payment types? Sounds like a slippery slope when it comes to reducing the privacy of one's financial data, but ok, if it's just payment types, maybe. This is, however, going to be a tough sell in Canada, especially since the Bank of Canada has given up on a digital currency!

In my opinion, all of this suggests innovations will (a) pop up outside of Canada (not be invented in Canada), (b) that Canadian companies who develop solutions will be bought out, or (c) that Canadian companies will develop solutions yet only be able to sell them elsewhere. Needing to rely on foreign sources to drive stock price doesn't strike me as lucrative for me as a Canadian investor. This might work for penny stocks, but like I have said many times before, I don't want to be glued to my screen all day stock-watching.

The third report on a sub-industry within finance I looked at was wealth management. For the cynics out there who are wondering who buys those services, think trust fund babies. Anyway. Skipping down to the priority matrix, the top five items seemed fairly similar:

- AI providing solutions

- consolidating services

- using the cloud to generate savings

- using generative AI

- not using humans to get clients

What this list strikes me as relative to their target audience is using computers to deal with rich idiots in order to save money. Hmmmm. While it is difficult for people to know where and how to invest, not spending tons of time to make investment decisions is a goal of mine. I mean, this really gets me to wonder what impact robo-advisors and ETFs are going to have. What will my analysis reveal in a year? I don't have a crystal ball, so I don't know yet, but I am happy with my understanding and application of my fundamental analysis approach. Anyway, with a focus on cost savings, I will look at mergers, buyouts and heavy use of technologies as indicators on whether the share price of a wealth management company may increase a bit - but I am not expecting leaps and bounds.

Alrighty, stock pick time!

Versabank (VBNK) seems to check a lot of the boxes in the above list for wealth management companies and payments. Less human integration, solutions for risk aversion, and recent expansion into the US with some hints of setting up shop in Florida. that said, I am curious as to why they issued so many new shares in December. All I know from what's available online is this: they have all their i's dotted and t's crossed, making them an obviously strong company. But I have no idea how to know what their stock price means. It isn't close to any floor I can see and I don't know how investors would make money via share price alone, especially if they want to issue more shares to buy more banks or integrative solutions. I'll add it to my watchlist out of curiosity.

RF Capital Group (RCG) doesn't seem to check a lot of boxes for a wealth management company, although it seems to be packaging its offerings according to the above-mentioned priority matrix. The stock price is at a floor and their assets under management (how much wealth has been entrusted for them to invest) seem to have risen a couple billion dollars worth in the past couple years. I don't know if that's good or not because I don't throw billions around and I don't know anyone who does. I will keep tabs on them.

Then there is Firm Capital Mortgage Group (FC), which seems to get around the whole AI thing for the moment given the types of investments they get into - not something AI can fish/phish for them. The Bank of Canada has been lowering its key interest rate and this could happen again in 2025, but we will have to wait for the announcement of their intentions on January 29th to see. I do know that lower rates mean more business in the lending world, particularly in the Canadian housing market. All of this said, I refuse to do a deep dive in all of their stuff because that takes time and AI isn't going to do that for me today. So, I will wait until I find other indicators that suggest a buy, but I find them very interesting.

Another company I found that I would like to buy, but I am skittish to do so, is Alaris Equity Partners (AD.UN). They seem to align somewhere between Decisive Dividend Corp. (who seeks ownership) and Versabank (that simply provides loans at point-of-sale). All three of these companies have different business models and Alaris gets my attention based on the above list for lending is they offer customized solutions, are data-driven, and have a lot of partnerships (seamless integration from a client's point of view). Their stock price is near a floor to boot, but I said I was skittish.

Alaris Equity Partners has issued an NCIB to buy back up to 10% of its shares this year. While this means the company is confident in itself, it also means they can forcibly move the share price a little through a few bulk buys. What I want to know is, what price do they consider a good deal - or more specifically, what is their interpretation of where the floor should be? I will wait a couple months to see before making a final decision on whether or not to buy.

One last company I looked into was First National Financial (FN). They tick a lot of boxes (I particularly like their myMortgage tool), but its the numbers that concern me. Sure, the CEO has been buying a lot of stocks recently, but the dividend is lacklustre (relative to the stock price), some analysts are predicting a slump mid-year, and the stock price is high (for me) even though many say it is undervalued. I will keep tabs on them, but to be honest, the share price is discouragingly high for me at present (in terms of buying a stack of shares to make it easy for share price increases to make it worth my while).

Speaking of coming back down to Earth, Canadian micro-investors should subscribe to the free Dollarwise email newsletter. They send daily examples of ways to save money, compare various things from rent vs buy to managing credit cards, ways to get out of various types of debt, and a slew of other personal finance tips. Check it out!

Ok, so what did I find in my backyard that was so surprising?

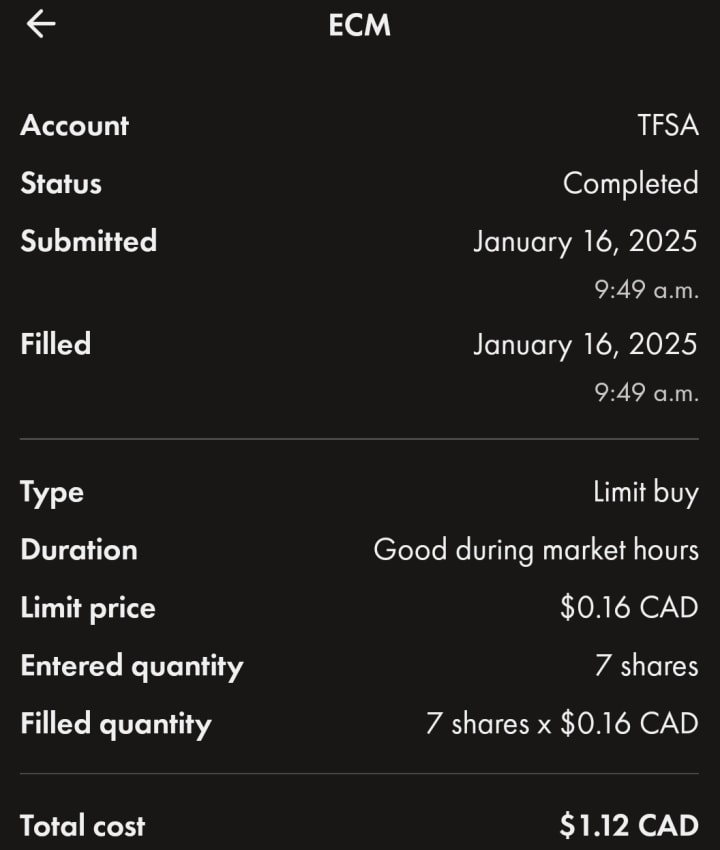

A way to spend my remaining dimes is what! A business called Ecolomondo (ECM) has setup shop nearby. They have also already undergone trials and tribulations by building their factory, securing funding, and ironing out kinks in their production line as well as signing deals. With it being early in the process and they have IP that tons of municipal governments around the world are in need of, I don't mind getting in on the ground floor now that the main hurdles have been dealt with. Plenty of opportunities and I am curious what specific business lines they get into in the future. Do I find it risky? Yes. With share price under twenty cents and the opportunities that abound, I don't care. I bought some.

Subscribe for free below to become notified right when I publish more articles and to see what I do or don't consider investing in next. Alternatively, you can bookmark this page that contains a list of all my entries in my stock trading journey I publish on Vocal Media.

About the Creator

Richard Soulliere

Bursting with ideas, honing them to peek your interest.

Enjoyes blending non-fiction into whatever I am writing.

Keep reading

More stories from Richard Soulliere and writers in Trader and other communities.

Stock Trading - Entry 29

Alright, so it's time to kick off 2025. What follows are some tips from real estate investors, a company that didn't make my cut, a rounding out of my ETF comparison, a couple stocks that did make it into my portfolio, and DRIPs. Note: I am not dispensing financial advice; these are only my thoughts pertaining to my own financial position and my own investment goals.

By Richard Soulliereabout a year ago in Trader

Petroleum Coke Market 2026: Trends, Applications, and Technological Innovations

Petroleum Coke Market Overview: Petroleum coke (petcoke) is a carbon-rich solid material derived from oil refining. It is primarily used as a fuel in power plants, cement kilns, and steel production due to its high calorific value and cost-effectiveness compared to coal. The market growth is closely tied to the global energy sector, industrialization, and infrastructure development. Geographically, North America and Asia-Pacific are major markets, while emerging economies in Latin America and the Middle East are showing increasing demand.

By James Smitha day ago in Trader

IT Training Market Accelerates as Digital Transformation and AI Adoption Reshape Global Workforce Development

IT Training Market Overview The global IT Training Market has emerged as a critical component of the modern digital economy. As enterprises adopt advanced technologies such as cloud computing, big data analytics, artificial intelligence (AI), blockchain, and cybersecurity frameworks, the need for skilled IT professionals continues to intensify.

By James Smith6 days ago in Trader

When the Shelter Closes

Across the street from my house, a man slept under a tree, his dog by his side. My first, naive thought: he must be traveling through. But he kept coming back, often sleeping there during the day. Then it hit me—that person might not have a home.

By Bride of Sound6 days ago in Humans

Comments (1)

Great stock trading tips! Good work