Saudi Arabia Entertainment and Amusement Market Set for a Golden Decade of Growth (2025–2033)

How Vision 2030, Youthful Consumers, and Immersive Technologies Are Reshaping the Kingdom’s Leisure Economy

Introduction: A New Era of Entertainment in the Kingdom

Entertainment and amusement have always been central to human life. They offer relaxation, inspiration, emotional connection, and moments of joy that break the routine of daily responsibilities. From storytelling and cinema to theme parks, sports, and digital gaming, the global entertainment industry reflects how societies evolve, spend, and express themselves.

In Saudi Arabia, this evolution is happening at an unprecedented pace. The Kingdom is undergoing a historic economic and cultural transformation under Vision 2030, and the entertainment and amusement sector has emerged as one of its most dynamic pillars. What was once a relatively limited market is now turning into a diversified, technology-driven, and investment-heavy ecosystem that caters to both local residents and international visitors.

According to Renub Research, the Saudi Arabia Entertainment and Amusement Market is expected to grow from US$ 2.46 billion in 2024 to US$ 6.10 billion by 2033, registering a strong CAGR of 10.61% from 2025 to 2033. This impressive expansion is being fueled by rapid infrastructure development, rising consumer spending, a young and digitally connected population, and the increasing adoption of immersive technologies such as virtual reality (VR) and augmented reality (AR).

More importantly, entertainment in Saudi Arabia is no longer just about leisure—it is becoming a strategic economic sector that supports tourism, job creation, urban development, and global brand positioning.

Saudi Arabia Entertainment and Amusement Industry Overview

The entertainment and amusement industry encompasses a wide range of activities designed to inform, inspire, and delight audiences. Entertainment includes creative and cultural expressions such as films, music, theatre, and live performances, while amusement focuses more on recreational and thrill-based experiences such as theme parks, gaming centers, sports activities, and family entertainment venues.

Together, these segments contribute not only to economic growth but also to social well-being. They encourage social interaction, promote creativity, reduce stress, and strengthen bonds among families and communities. In modern societies, entertainment is increasingly viewed as a necessity rather than a luxury—and Saudi Arabia is no exception.

Over the past decade, the Kingdom has witnessed a dramatic shift in how entertainment is produced, consumed, and regulated. High-speed internet, smartphone penetration, and digital platforms have transformed consumer behavior. At the same time, large-scale investments in physical venues such as cinemas, theme parks, cultural centers, and mixed-use entertainment districts have expanded the offline experience as well.

Technological innovation plays a crucial role in this transformation. The growing use of VR, AR, and high-definition interactive displays has introduced immersive entertainment formats that were previously unavailable in the local market. These technologies are not only enhancing user experiences but also opening new revenue streams for operators across cinemas, gaming centers, and amusement parks.

Another major driver is the steady rise in disposable income. As living standards improve, Saudi consumers are increasingly willing to spend on premium and memorable leisure experiences. This shift in spending priorities is encouraging entertainment providers to continuously innovate, diversify offerings, and raise service quality to international standards.

Market Size and Growth Outlook (Renub Research)

Renub Research estimates that the Saudi Arabia Entertainment and Amusement Market will grow from US$ 2.46 billion in 2024 to US$ 6.10 billion by 2033, reflecting a CAGR of 10.61% during the forecast period from 2025 to 2033.

This growth trajectory highlights several important trends:

Entertainment is becoming a core part of the Kingdom’s non-oil economy.

Consumer demand is shifting from basic leisure activities to more immersive and experience-driven offerings.

Large-scale government-backed projects are accelerating private sector participation and foreign investment.

The sector is benefiting from strong linkages with tourism, hospitality, retail, and real estate development.

Unlike short-term booms, this expansion is supported by long-term structural changes in demographics, policy, and infrastructure—making the outlook for the industry both strong and sustainable.

Key Growth Drivers of the Saudi Arabia Entertainment and Amusement Market

1. Massive Investment and Infrastructure Development

Saudi Arabia is witnessing one of the largest entertainment infrastructure build-outs in the world. Mega-projects such as NEOM, the Red Sea Project, and Qiddiya are redefining the scale and ambition of leisure development in the region.

NEOM alone represents an investment of around USD 500 billion, designed to create a futuristic city that integrates entertainment, media production, technology, and tourism. The Red Sea Project, spanning 28,000 square kilometers and including more than 90 islands, is positioning the Kingdom as a global luxury tourism and entertainment destination.

Qiddiya, often described as the “capital of entertainment, sports, and the arts,” is another landmark project. Spread over 334 square kilometers, it will feature theme parks, motorsport tracks, sports arenas, cultural venues, and family entertainment zones. Once completed, it is expected to generate tens of thousands of jobs and attract millions of visitors annually.

Beyond these mega-projects, the government and private sector are also investing heavily in cinemas, family entertainment centers, malls, and cultural spaces across major cities—creating a nationwide ecosystem for leisure and amusement.

2. Young Population and Rising Consumer Spending

Saudi Arabia has one of the youngest populations in the region, with over 60% of citizens under the age of 34. This demographic profile is a powerful engine for entertainment demand, as younger consumers are typically more open to new experiences, digital platforms, and lifestyle-oriented spending.

Saudi households allocate a higher share of their income to leisure and entertainment compared to several developed markets. On average, Saudi consumers spend around 6.2% of their income on entertainment and leisure, compared to about 4.2% in the UK. Annual entertainment spending in Saudi Arabia is estimated at around USD 1.6 billion, significantly higher than in some neighboring GCC countries.

This strong appetite for entertainment is encouraging developers and operators to expand offerings across cinemas, gaming centers, theme parks, live events, and cultural festivals. It also provides a solid foundation for long-term market growth.

3. Vision 2030 and Government Support

Vision 2030 is the single most important policy driver behind the transformation of Saudi Arabia’s entertainment sector. The strategy aims to diversify the economy away from oil, enhance quality of life, and position the Kingdom as a global tourism and cultural hub.

One of the most symbolic milestones was the lifting of the 35-year cinema ban in 2017, which opened the door to rapid expansion in the film and cinema segment. Since then, institutions such as the General Entertainment Authority (GEA) have been established to regulate, promote, and support entertainment activities across the country.

The Public Investment Fund (PIF) has also played a key role through strategic investments and partnerships. Collaborations with international cinema operators and entertainment brands have accelerated the rollout of modern venues and experiences. These initiatives are not only boosting supply but also raising industry standards and global competitiveness.

Challenges Facing the Market

Regulatory and Bureaucratic Hurdles

Despite significant progress, the entertainment industry in Saudi Arabia still faces regulatory complexities. Licensing procedures, approval timelines, and content regulations can be time-consuming and require careful compliance. While these measures are designed to ensure cultural alignment and public safety, they can slow down project implementation and increase operational costs for both local and foreign investors.

Dependence on Tourism

A substantial portion of high-end entertainment and amusement projects rely on tourist inflows. Geopolitical tensions, global travel disruptions, or changes in international travel preferences can affect visitor numbers and, in turn, revenue performance. To ensure long-term stability, the industry must continue to strengthen domestic demand alongside international tourism.

City-Level Market Insights

Riyadh

Riyadh stands at the center of Saudi Arabia’s entertainment transformation. Flagship initiatives such as Riyadh Season and the development of Qiddiya are turning the capital into a regional entertainment powerhouse. The city is seeing rapid growth in cinemas, live events, family entertainment centers, and cultural venues. While regulatory and cultural considerations remain important, Riyadh’s young population, rising incomes, and strong government backing provide a robust platform for sustained growth.

Jeddah

Jeddah’s strategic location on the Red Sea and its role as a gateway for international visitors make it a natural hub for entertainment and tourism. Projects linked to the Red Sea development and seasonal festivals such as Jeddah Season are boosting demand for theme parks, resorts, and cultural events. However, competition from neighboring destinations and reliance on tourism require careful long-term planning.

Makkah

Makkah’s entertainment market is unique due to its religious significance. While religious tourism remains dominant, the government is gradually introducing family-friendly and culturally sensitive entertainment options such as shopping malls, recreational areas, and projects like Makkah Boulevard. The key challenge here is balancing tradition, cultural values, and modern leisure development.

Market Segmentation

By Type of Entertainment Destination:

Cinemas and Theatres

Amusement and Theme Parks

Gardens and Zoos

Malls

Gaming Centers

Others

By Source of Revenue:

Tickets

Food and Beverages

Merchandise

Advertising

Others

By City:

Riyadh

Jeddah

Makkah

Dammam

Rest of Saudi Arabia

Competitive Landscape

The Saudi entertainment and amusement market features a mix of local groups and specialized entertainment companies, including:

Al Hokair Group

Fakieh Group

Saudi Aramco Amusement Park

E-PLUS (Event Plus)

Time Entertainment

First Entertainment Company

Belle Gate

The Marvel Experience

These companies compete on the basis of venue quality, experience design, technology adoption, and partnerships with global brands. Continuous innovation and expansion are becoming essential to maintain market relevance.

Final Thoughts: Entertainment as an Economic and Social Catalyst

Saudi Arabia’s entertainment and amusement market is entering a defining decade. With strong support from Vision 2030, massive infrastructure investments, a young and enthusiastic consumer base, and rapid technological adoption, the sector is poised for sustained and transformative growth.

The rise from US$ 2.46 billion in 2024 to US$ 6.10 billion by 2033, as projected by Renub Research, is more than just a statistical milestone—it reflects a broader shift in how the Kingdom envisions quality of life, economic diversification, and global engagement.

While challenges related to regulation and tourism dependency remain, the long-term fundamentals of the market are strong. Entertainment in Saudi Arabia is no longer a peripheral industry; it is becoming a central pillar of the nation’s future economy and social landscape.

About the Creator

Asia Pacific Pediatric Interventional Cardiology Market Size and Forecast 2025–2033

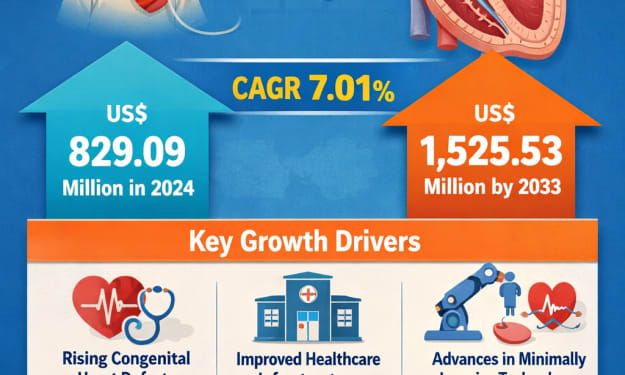

Introduction The Asia Pacific Pediatric Interventional Cardiology Market is entering a period of sustained and meaningful growth as healthcare systems across the region place increasing emphasis on advanced, child-focused cardiac care. According to Renub Research, the market is expected to reach US$ 1,525.53 million by 2033, rising from US$ 829.09 million in 2024, at a compound annual growth rate (CAGR) of 7.01% from 2025 to 2033.

By shibansh kumara day ago in Trader

Australia Lubricants Market 2026: Gears Up for Steady Growth on Automotive, Industrial & Sustainability Trends

Australia Lubricants Market Overview The Australia lubricants market size is on a steady upward trajectory as demand from automotive, industrial, and heavy machinery sectors continues to expand. According to the latest data from IMARC Group, the market was valued at USD 2,961.53 million in 2025 and is forecast to reach USD 4,333.36 million by 2034, growing at a compound annual growth rate (CAGR) of 4.32% during the 2026–2034 period.

By Amyra Singh3 days ago in Trader

Comments

There are no comments for this story

Be the first to respond and start the conversation.