Japan Water Heater Market Size and Forecast 2025–2033: Clean Energy, Smart Homes, and the Hydrogen Future

Driven by carbon neutrality goals, smart technology adoption, and next-generation hydrogen systems, Japan’s water heater industry is entering a decisive decade of innovation and export-led growth.

Japan Water Heater Market Overview

According to Renub Research, the Japan Water Heater Market is expected to reach US$ 2.2 billion by 2033, up from US$ 1.42 billion in 2024, expanding at a compound annual growth rate (CAGR) of 5.01% from 2025 to 2033. This steady and resilient growth reflects Japan’s broader transformation toward energy efficiency, carbon neutrality, and smart home integration.

Water heaters are no longer viewed as simple household appliances in Japan. They have become a critical part of the country’s energy transition strategy, residential infrastructure modernization, and industrial efficiency upgrades. With strong government backing, rising electricity and fuel costs, and increasing environmental awareness among consumers, the Japanese water heater market is shifting rapidly toward high-efficiency, low-emission, and next-generation systems.

A defining characteristic of this market is its focus on eco-friendly refrigerants, heat pump technologies, solar integration, and hydrogen-based systems. Japanese manufacturers are not only responding to domestic policy goals but are also positioning themselves as global exporters of clean and advanced water heating technologies. This dual focus—serving domestic decarbonization needs while building export-ready innovation—makes Japan’s water heater industry one of the most technologically progressive in the world.

Japan Water Heater Industry in Transition

Driven largely by the national push toward carbon neutrality by 2050, Japan’s water heater industry is undergoing a structural shift away from conventional fossil-fuel-dependent systems toward cleaner, smarter, and more efficient technologies. Traditional gas and electric storage heaters are gradually being complemented—and in some segments replaced—by heat pump systems, tankless solutions, solar water heaters, and experimental hydrogen-powered units.

Hydrogen, in particular, has emerged as a strategic area of focus. In December 2024, Noritz, in collaboration with Dux and Australian energy company ATCO, launched a field test of a domestic water heater running entirely on hydrogen at ATCO’s hydrogen house in Western Australia. The system is designed to safely and consistently supply hot water using pure hydrogen and will be tested over a two-year period.

This initiative is more than just a pilot project. It signals Japan’s ambition to become a global leader in hydrogen-compatible household appliances, setting future international benchmarks for safety, performance, and reliability. As hydrogen infrastructure gradually develops worldwide, Japanese manufacturers are positioning themselves early to capture this emerging market.

Beyond hydrogen, the industry is also witnessing strong momentum in heat pump water heaters, hybrid systems, and smart-connected appliances. These technologies align well with Japan’s urban lifestyle, limited living spaces, and strong consumer preference for energy-saving, high-performance products.

Key Factors Driving the Japan Water Heater Market

1. Supportive Government Policies and Incentives

One of the strongest growth engines for the Japan water heater market is government policy support. Japan has introduced multiple initiatives aimed at reducing household and commercial energy consumption while accelerating the adoption of energy-efficient and renewable technologies.

A notable example is the “Housing Energy Saving 2024 Campaign,” which is part of the country’s broader roadmap toward carbon neutrality. This program promotes high-efficiency water heaters, better home insulation, and overall energy-saving renovations. Through subsidies, grants, and low-interest financing, the government has significantly lowered the upfront cost barrier for consumers considering solar water heaters, heat pump systems, and other advanced technologies.

These incentives are especially important in a market where the initial investment for high-efficiency systems can be higher than traditional models. By reducing payback periods and improving affordability, government programs are accelerating adoption across residential, commercial, and even small industrial segments.

2. Technological Advancements and Smart Integration

Japan’s reputation for precision engineering and consumer electronics innovation is clearly reflected in its water heater market. Today’s systems are no longer standalone appliances—they are increasingly becoming part of the smart home ecosystem.

Modern water heaters now offer Wi-Fi connectivity, mobile app control, real-time energy monitoring, and predictive maintenance alerts. Users can adjust temperature settings remotely, track energy usage patterns, and optimize performance based on daily routines. This level of integration is particularly attractive to urban consumers who value convenience, efficiency, and control.

From a technology perspective, tankless water heaters and heat pump systems are leading the shift. Tankless systems provide instant hot water with reduced energy waste, while heat pumps deliver superior efficiency by transferring heat rather than generating it directly. These solutions align perfectly with Japan’s space constraints and energy-saving priorities.

3. Rising Energy Costs and Environmental Awareness

Japan, like many developed economies, has been facing volatile energy prices and long-term concerns about energy security. This has made consumers more conscious of operating costs and more receptive to energy-efficient appliances.

Solar and heat pump water heaters, in particular, are gaining traction because of their long-term cost savings. In some cases, solar water heating systems can reduce energy bills by 70–80%, making them an attractive investment despite higher upfront costs. Combined with long service life and relatively low maintenance requirements, these systems offer strong lifetime value.

At the same time, environmental awareness among Japanese consumers continues to grow. Climate change, carbon reduction targets, and sustainability have become mainstream considerations in purchasing decisions. Water heaters, being among the largest energy-consuming household appliances, are naturally in focus when households look to reduce their carbon footprint.

Challenges in the Japan Water Heater Market

1. Installation and Maintenance Barriers

Despite strong demand, the market faces a practical challenge: a shortage of skilled technicians capable of installing and maintaining advanced systems such as heat pump and solar water heaters. These systems require specialized knowledge, precise installation, and proper configuration to achieve optimal performance.

In many cases, limited availability of trained professionals can lead to higher installation costs, delays, and inconsistent service quality. This issue is more pronounced in rural or less densely populated regions, where access to certified installers is limited. Without adequate after-sales support, some consumers remain hesitant to adopt newer technologies.

Addressing this challenge will require expanded training programs, certification initiatives, and closer collaboration between manufacturers, installers, and technical institutions.

2. Limited Space in Urban Homes

Japan’s dense urban environment presents another unique constraint. Many apartments and houses, especially in cities like Tokyo and Osaka, have limited installation space. Larger storage tank systems or solar setups with external panels can be difficult to accommodate.

Even outdoor units, such as those used in heat pump systems, may face restrictions due to small balconies, limited exterior wall space, or strict building regulations. As a result, some consumers are forced to choose smaller or less efficient models that may not deliver the same level of energy savings.

This challenge is pushing manufacturers to focus on compact, space-saving, and modular designs that can deliver high performance within tight spatial constraints.

Market Segmentation Analysis

By Product

Electric Water Heaters

Solar Water Heaters

Gas Water Heaters

Electric and gas water heaters continue to dominate in terms of installed base, but solar and hybrid systems are gaining share as sustainability becomes a priority.

By Technology

Tankless Water Heaters

Storage Tank Water Heaters

Hybrid Systems

Tankless and hybrid systems are seeing faster adoption due to their efficiency, space-saving design, and compatibility with smart home features.

By Application

Residential

Commercial

Industrial

The residential segment remains the largest, driven by home upgrades and new energy-saving housing projects. However, the commercial sector—including hotels, hospitals, and office buildings—is increasingly investing in high-efficiency systems to reduce operating costs and meet sustainability goals.

By Capacity

Below 30 Liters

30 – 100 Liters

100 – 250 Liters

250 – 400 Liters

Above 400 Liters

Smaller and mid-capacity systems dominate urban households, while larger capacities are more common in commercial and industrial applications.

Competitive Landscape and Company Analysis

The Japan water heater market features a mix of global appliance giants and specialized heating technology companies. Key players covered in the market include:

A.O. Smith

Rinnai Corporation

Whirlpool Corporation

Bajaj Electricals Ltd

Haier Inc.

Havells India Ltd

Lennox International Inc.

Kenmore

Thermex Corporation

These companies compete on energy efficiency, product reliability, technological innovation, after-sales service, and pricing. Japanese firms, in particular, are heavily investing in R&D for hydrogen-compatible systems, advanced heat pumps, and ultra-efficient tankless designs, aiming to strengthen both domestic leadership and global export potential.

Recent developments across the industry highlight a strong focus on decarbonization, smart connectivity, and long-term cost savings for consumers, reinforcing the sector’s innovation-driven growth model.

Outlook: A Market Shaped by Clean Energy and Smart Living

Looking ahead, the Japan water heater market is set to benefit from three powerful and converging trends:

National decarbonization policies,

Technological innovation in heating systems, and

Changing consumer expectations around efficiency and sustainability.

With Renub Research forecasting the market to grow from US$ 1.42 billion in 2024 to US$ 2.2 billion by 2033 at a CAGR of 5.01%, the industry’s direction is clear. Water heaters in Japan are evolving from basic appliances into strategic components of energy-efficient, low-carbon, and digitally connected homes and buildings.

Hydrogen-based systems, in particular, could redefine the future of residential water heating, while heat pumps, solar integration, and smart controls will continue to drive near-term growth.

Final Thoughts

Japan’s water heater market stands at the intersection of policy, technology, and sustainability. What was once a mature and relatively stable appliance segment is now becoming a dynamic platform for clean energy innovation and smart living solutions.

As manufacturers continue to invest in next-generation technologies and the government strengthens its push toward carbon neutrality, water heaters will play a more strategic role in Japan’s energy ecosystem. For consumers, this means lower energy bills, smarter homes, and a smaller environmental footprint. For the industry, it means a decade of steady growth, global opportunity, and technological leadership.

About the Creator

Visa Stock Analysis: Why Visa Remains a Strong Play in the Global Payments Industry

Introduction Visa stock has consistently been one of the most reliable growth investments in the financial technology sector. As a global leader in digital payments, Visa Inc. processes billions of transactions annually, connecting consumers, businesses, and financial institutions across the globe. With the ongoing shift from cash to digital payments, Visa’s business model positions it to benefit from structural growth trends in global commerce. For investors, Visa stock represents a combination of stability, recurring revenue, and long-term growth potential.

By Hammad Nawaz4 days ago in Trader

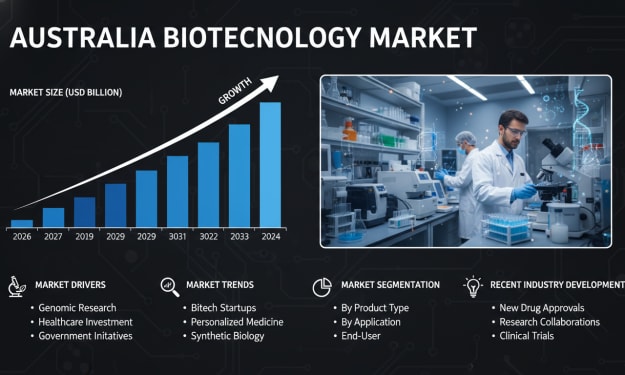

Australia Biotechnology Market — Growth, Forecast & Strategic Outlook 2026–2034

The Australia biotechnology market has reached a significant scale as biotechnological solutions become integral to healthcare, agriculture, environmental sustainability, and industrial processing. According to IMARC Group, the market was valued at USD 13.4 billion in 2025 and is forecast to reach USD 24.8 billion by 2034, growing at a compound annual growth rate (CAGR) of 7.02% during 2026–2034.

By Amélie Belle8 days ago in Trader

Comments

There are no comments for this story

Be the first to respond and start the conversation.