India Frozen Paratha Market Size and Forecast 2025

From Convenience to Cuisine: How Frozen Parathas Are Reshaping India’s Ready-to-Eat Food Landscape

India Frozen Paratha Market Overview

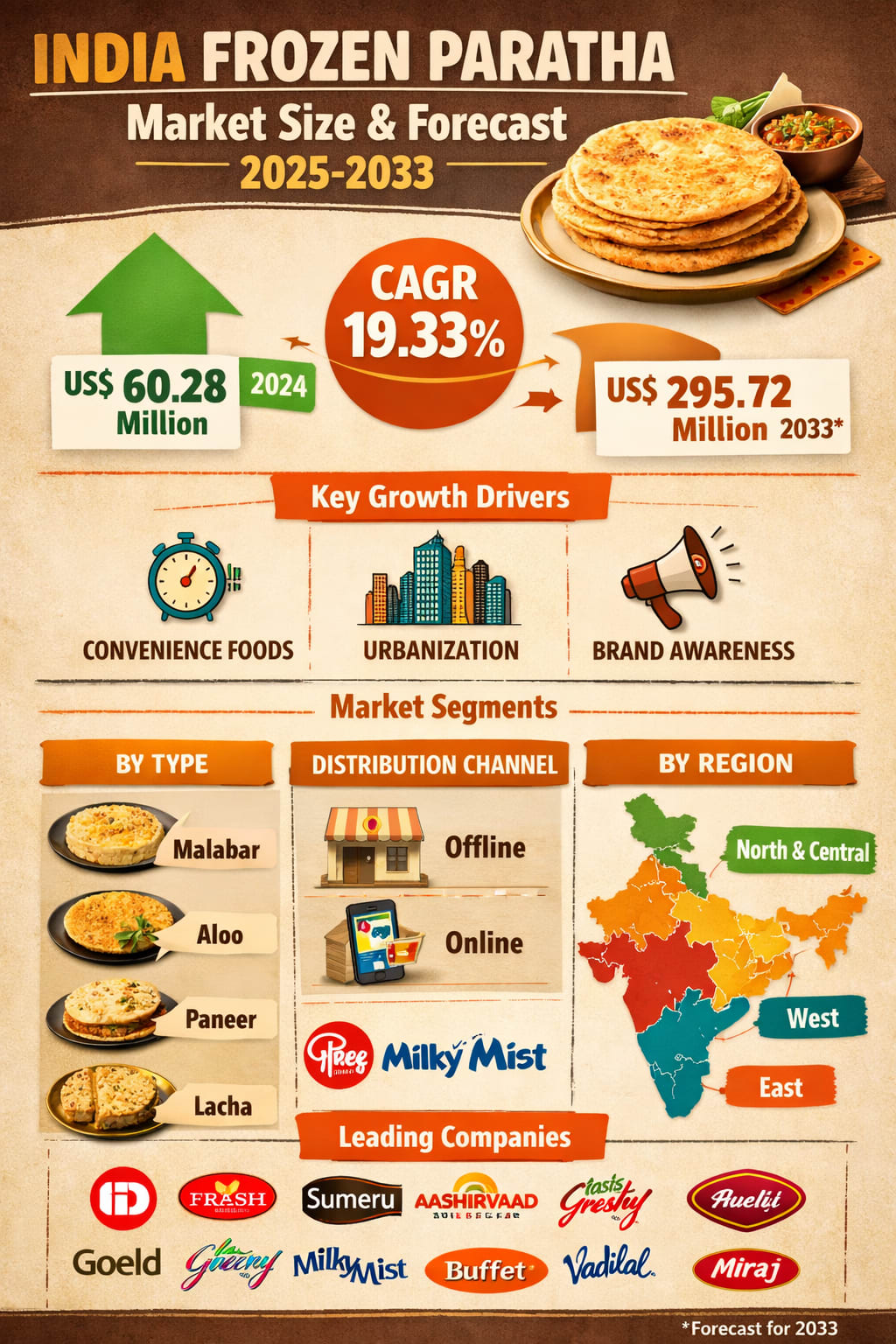

The India Frozen Paratha Market is witnessing a remarkable transformation, driven by changing lifestyles, rising urbanization, and the growing demand for convenient yet authentic food options. According to Renub Research, the market is expected to reach US$ 295.72 million by 2033, up from US$ 60.28 million in 2024, growing at an impressive CAGR of 19.33% from 2025 to 2033.

Frozen parathas, made from wheat flour and traditional spices, are pre-cooked and designed to be quickly reheated in a pan or microwave. Available in a wide variety of flavors such as plain, aloo (potato), paneer, methi, and Malabar-style parathas, these products offer consumers a perfect blend of convenience and authentic taste. After freezing, the parathas retain their texture and flavor, making them an easy substitute for freshly prepared meals or snacks.

India’s fast-growing economy is also playing a crucial role in shaping this market. The World Bank has consistently highlighted India as one of the world’s fastest-growing major economies, with ambitions of becoming a high-income nation by 2047, the centenary of its independence. This economic momentum, combined with rising disposable incomes, hectic urban lifestyles, and expanding modern retail infrastructure, is creating fertile ground for the growth of the frozen paratha segment.

What was once considered a niche product for a small urban audience is now steadily entering mainstream households. Improved cold chain logistics, better awareness about frozen food quality, and the rapid rise of online grocery platforms are further accelerating adoption across different regions of the country.

Market Size and Forecast: A High-Growth Story

The growth trajectory of the India Frozen Paratha Market reflects broader changes in Indian food consumption patterns. From US$ 60.28 million in 2024 to a projected US$ 295.72 million by 2033, the market’s expansion underscores how quickly convenience foods are becoming part of everyday life.

A 19.33% CAGR over the forecast period is not just impressive—it signals a structural shift in how Indian consumers approach meals. Instead of viewing frozen foods as inferior substitutes, a growing segment of consumers now sees them as smart, time-saving solutions that do not compromise much on taste or quality.

Several factors are working together to support this growth: increasing urbanization, the rise of nuclear families, higher participation of women in the workforce, longer working hours, and the spread of modern retail and e-commerce platforms. Together, these trends are reshaping the food consumption landscape and creating sustained demand for products like frozen parathas.

Key Growth Drivers

Rising Demand for Convenience Foods

One of the strongest drivers behind the frozen paratha market in India is the surging demand for convenience foods. As urbanization continues and daily schedules become more packed, consumers are actively seeking quick, hassle-free meal solutions. Traditional cooking methods, especially for items like parathas, can be time-consuming and require preparation, rolling, and cooking. Frozen parathas eliminate most of this effort—consumers only need to heat them.

This convenience is particularly appealing to small families, students, and working professionals who want home-style meals without investing significant time in the kitchen. The growth of dual-income households and rising disposable incomes have further boosted spending on convenience foods. For many consumers, frozen parathas strike the right balance between speed, taste, and familiarity.

Increasing Urbanization

Urbanization is another major force shaping the frozen paratha market. As more people migrate to cities in search of better jobs and opportunities, lifestyles are becoming increasingly fast-paced. Urban consumers often have less time for traditional cooking, which increases the appeal of ready-to-cook and ready-to-heat food options.

Frozen parathas fit perfectly into this lifestyle shift. They offer the comfort of familiar Indian food with minimal preparation time. Moreover, their availability in supermarkets, hypermarkets, and online grocery platforms has made them more accessible than ever before. Cities are also home to a large population of students, young professionals, and nuclear families—groups that are especially inclined toward convenient food solutions.

Increased Brand Awareness and Product Innovation

Brand awareness has played a critical role in expanding the frozen paratha market. Through advertising, social media marketing, in-store promotions, and word-of-mouth, consumers are becoming more familiar with frozen food products and more confident about their quality and safety.

A notable example is Aashirvaad, which entered the frozen food segment in January 2023 with the launch of five varieties of frozen naans and parathas, including paneer, aloo, Malabar, and tandoori options. Such moves by well-known brands not only increase competition but also build consumer trust in the category as a whole.

Companies are also focusing on highlighting freshness, authentic taste, and improved nutritional profiles, which helps overcome traditional skepticism toward frozen foods. As a result, the market is expanding beyond metro cities into smaller urban and semi-urban areas.

Key Challenges

Cold Chain and Storage Issues

Despite strong growth prospects, the frozen paratha market in India faces significant challenges related to cold chain and storage infrastructure. Maintaining the required temperature throughout transportation, storage, and retail display is critical for preserving product quality and safety. In many rural and semi-urban areas, cold chain facilities are still inadequate.

Any breakdown in this system can lead to spoilage, reduced shelf life, and compromised taste and texture, which in turn affects consumer trust. For companies, investing in reliable cold chain logistics remains both a necessity and a cost-intensive challenge.

Competition from Local Alternatives

Another major hurdle is competition from local, freshly prepared alternatives. In many parts of India, consumers still prefer buying hot, fresh parathas from neighborhood shops or preparing them at home. These options are often perceived as fresher, cheaper, and more culturally authentic.

Convincing such consumers to switch to frozen products requires strong branding, consistent quality, and clear communication of the convenience and hygiene benefits. While urban consumers are gradually making this shift, local competition continues to limit market penetration in many regions.

Regional Insights

North & Central Region

The North and Central regions of India—including states like Punjab, Haryana, Delhi, Uttar Pradesh, and Madhya Pradesh—represent an important market for frozen parathas. Parathas are already a staple in these regions, which creates a natural demand base for frozen variants.

Urbanization and changing lifestyles are driving adoption, especially in major cities. Consumers are increasingly choosing ready-to-cook parathas for convenience without sacrificing familiar flavors. The growth of modern retail outlets and improvements in cold chain infrastructure are further supporting market expansion in this region.

Southern Region

In Southern India, cities such as Bangalore, Hyderabad, and Chennai are witnessing steady growth in frozen paratha consumption. While traditional foods like idli and dosa continue to dominate, frozen parathas—especially Malabar parathas—are gaining popularity among urban consumers who value convenience.

Rising disposable incomes, exposure to diverse cuisines, and the spread of organized retail formats are key factors driving growth here. For many time-pressed households, frozen parathas are becoming a practical addition to their meal options.

Western Region

Western India, including Maharashtra, Gujarat, and Rajasthan, is seeing significant growth in the frozen paratha market. Urban centers like Mumbai and Pune, with their busy lifestyles and high concentration of working professionals, are major demand hubs.

Plain, aloo, and paneer parathas are particularly popular in this region. Expanding retail networks and improving cold chain logistics are making these products more widely available, encouraging more consumers to adopt them for quick, authentic meals.

Eastern Region

The Eastern region—covering West Bengal, Odisha, Bihar, Jharkhand, and the Northeast—is gradually emerging as a growth market for frozen parathas. While regional cuisines still dominate, urbanization and changing lifestyles are increasing demand for convenience foods.

Cities like Kolkata, Bhubaneswar, and Patna are witnessing growing adoption, especially among nuclear families and working professionals. As cold chain infrastructure improves and product availability increases, frozen parathas are becoming a more common choice for quick, home-style meals.

Market Segmentation

By Type

Malabar Paratha

Lacha Paratha

Paneer Paratha

Aloo Paratha

Others

By Distribution Channel

Offline

Online

By Region

North & Central Region

Southern Region

Western Region

Eastern Region

Company Analysis

The competitive landscape of the India Frozen Paratha Market includes a mix of established food brands and specialized frozen food players. Key companies covered include:

ID Fresh

Haldiram

Sumeru

Goeld

Aashirvaad

Tasty Fresh

Buffet

Asal Foods (Milky Mist Dairy)

Godrej

WahUstad

Keventer

Miraj Group

Vadilal

Brillar

Kawaan

Swaad

Each company is analyzed across five key dimensions:

Overview

Recent Development & Strategies

Monthly All-India Sales (June 2022 – May 2023)

Major City Sales (June 2022 – May 2023)

Yearly Volume Analysis by Distribution Channel (June 2022 – May 2023)

Competition is intensifying as more brands enter the segment, innovate with new flavors, and invest in marketing and distribution to capture a larger share of this fast-growing market.

Final Thoughts

The India Frozen Paratha Market is no longer a niche segment—it is fast becoming a mainstream category within the country’s broader frozen and convenience food industry. With the market projected to grow from US$ 60.28 million in 2024 to US$ 295.72 million by 2033, the opportunities for brands, retailers, and investors are substantial.

Driven by urbanization, rising incomes, changing lifestyles, and improving retail and cold chain infrastructure, frozen parathas are well-positioned to become a regular feature in Indian kitchens. While challenges such as cold chain limitations and competition from fresh alternatives remain, continuous innovation, strong branding, and expanding distribution networks are likely to overcome these hurdles over time.

About the Creator

Tom Shane

Tom Shane is a content writer specializing in SEO-driven blogs, product descriptions, and thought leadership. He crafts engaging, research-backed content that connects with audiences and drives results.

The Institutionalization of Crypto Assets, From Speculation to Financial Infrastructure

Crypto assets were long regarded as highly volatile speculative instruments driven primarily by retail investors. In their early stages, the market lacked clear regulation and institutional-grade infrastructure, allowing prices to swing wildly based on narrative and sentiment rather than fundamentals. In recent years, however, the crypto market has passed a clear inflection point. Digital assets are no longer a theoretical experiment about the future of finance. They are being restructured into a recognized asset class with defined rules, liquidity mechanisms, and long-term investment relevance. At the center of this transformation stands the growing participation of institutional investors.

By crypto genie3 days ago in Trader

Comments

There are no comments for this story

Be the first to respond and start the conversation.