I Tried Viral Budget Hacks—What Worked

Cash envelopes, no-spend weekends, and the surprising truth about financial advice on social media

My bank account and I have long been a tumultuous couple. It isn't that I'm wasteful – I don't carry luxury handbags or take first class. It's more like a gradual, corrosive drip: the morning latte, the Amazon impulse buy, the subscription service I didn't even realize I had. Next thing I knew, payday would be regrettably out of reach.

Flicking through TikTok and Instagram, I was bombarded with 'life-changing' viral budget hacks promising financial independence with seemingly little effort. Envelope filling, no-spend challenges, 50/30/20 – the tips were infinite, frequently conflicting, and typically delivered with infuriatingly cheerful zeal.

Tired of my financial murkiness, I took a radical experiment: for one month, I would attempt all the most trendy viral budgeting tricks I could discover. All of them. At the same time (where feasible).

My aim wasn't simply to reduce expenses, but to determine which, if any, of these fashionable methods worked for a normal individual with odd willpower. Be my human guinea pig in personal finance fads.

The Contenders:

Cash Envelope System: Putting a certain cash amount into each budget category (groceries, eating out, entertainment) and placing that cash into labeled envelopes. When the envelope is depleted, no more spending in that category occurs. The Theory: Having physical cash makes it more real and hurts more.

50/30/20 Rule: Spending 50% of after-tax income on Needs (rent, electricity, groceries), 30% on Wants (eating out, hobbies, shopping), and 20% on Savings/Debt Repayment. The Theory: Offers a straightforward system of balanced budgeting.

No-Spend Challenge (Modified): Allowing certain days (I designated weekends) when no money is spent on non-necessities. The Theory: Stops impulse purchases and identifies spending triggers.

Automated Savings: Creating automatic deposits to a savings account on payday. The Theory: 'Pay yourself first' before you have an opportunity to spend it.

Budgeting Apps (Syncing): Utilizing an app (I used a well-known free one) to monitor all spending by syncing bank accounts and credit cards. The Theory: Offers real-time insight into spending patterns.

Meal Prepping: Preparing meals for the week ahead of time. The Theory: Eliminates costly takeout orders and food waste.

Subscription Audit: Checking all regular subscriptions and cancelling unused ones. The Theory: Stops forgotten money drains.

The Experiment Begins: Week 1 - Enthusiasm & Envelope Anxiety

Week one was driven by naivety. I faithfully crunched my 50/30/20 percentages, made a terrifying pile of cash at the bank, and Sharpied my envelopes. Budgeting app synced up, sharing terrifying facts about my coffee spend. I spent Sunday afternoon prep-ing vegetables, feeling self-righteous.

The envelopes for cash were instantly effective. Giving physical money for groceries was… different. More tangible. Watching the 'Dining Out' envelope shrink after one night out for pizza was a harsh visual reminder. But it was also cumbersome. Who walks around with clumps of cash anymore? Filling up at the pump was clumsy. Dividing a dinner bill among friends meant complicated envelope negotiations. And losing an envelope was always a fear.

The no-spend weekend was surprisingly painless the first time around – I stuck to free activities such as hiking and reading. Automatic savings swept money away before I even had time to miss it. Subscription audit brought instant results – adios, streaming service I haven't used in six months!

Week 2 - The Grind & Meal Prep Fatigue

The excitement had worn off. Meal prepping was just a pain. Sunday nights were spent preparing industrial amounts of chicken and rice, and by Thursday, I was thoroughly regretting my decision-making. The envelopes for cash were frustrating. I ended up going through 'Entertainment' cash mid-week, which resulted in a grumpy Friday night stay-at-home. The 50/30/20 worked too hard; a surprise car repair left my 'Needs' category entirely askew, and I had to 'borrow' from 'Wants' (which didn't feel right).

The budgeting app, however, was proving its worth. Seeing every transaction categorized provided undeniable clarity. It highlighted patterns I hadn’t noticed, like my tendency towards small, frequent online purchases.

Week 3 - Rebellion & Finding Flexibility

I ran up against something. I disliked the cash envelopes. I missed the simplicity of swiping my card. I gave in and got takeout after a long day at work, silently apologizing to my pathetic, prepared meal in the fridge. The second no-spend weekend had felt like torture. I had come to understand strict adherence wasn't jiving with my lifestyle.

This compelled a shift. I abandoned the actual cash envelopes but retained the concept. With the budgeting tool, I established virtual envelopes or spending limits for each category. It gave me the same consciousness without the hassle. I adapted the 50/30/20 rule to a rough guideline with room for variation between months. I adapted the no-spend challenge – rather than cold turkey zero spending, I allocated a very low weekend budget, with room for an occasional coffee or small indulgence, which seemed more realistic.

Week 4 - Integration & Sustainable Habits

The last week was less of a series of hacks and more of an integrated system. Automatic savings went on without a hitch. The budgeting app remained my go-to for tracking and awareness. Meal prep occurred, but less vigorously – perhaps just lunches, or prepping dinners that utilized similar ingredients. The subscription audit's savings were evident on my bank statement.

The Verdict: What Worked, What Didn't, and What Stuck

Cash Envelopes: Didn't Work (for me). Too kludgy for contemporary life. The concept of assigning and monitoring spending by category, though, is good. Virtual envelopes/tracking in an app did the same job without the hassle.

50/30/20 Rule: Functioned (as a Guideline). Excellent place to begin learning about allocation, but require flexibility. Life does not always cooperate with percentages. Apply as a goal, but don't berate yourself over month-to-month variations.

No-Spend Challenge: Functioned (Modified). Punitively strict no-spend days were unpalatable, but low-spend days worked well as a deterrent to impulse shopping and promotion of free activities. Educate yourself.

Automated Savings: WORKED! The one best, no-effort hack. Set and forget. This is not negotiable for saving.

Budgeting Apps: WORKED! Needed for visibility and accountability. Connecting accounts offers immediate data that's difficult to overlook. Pick one that you find easy to use and review it on a regular basis.

Meal Prepping: Worked (in Moderation). Prepping every single meal led to burnout, but planning dinners and prepping lunches saved significant money and reduced food waste. Find a level that’s sustainable for you.

Subscription Audit: WORKED! Easy win. Do this quarterly. You’ll likely find forgotten subscriptions draining your account.

The Takeaway:

There is no one magic fix for budgeting. Viral tips tend to overcomplicate complicated behavior around money. The best method appears to be a tailored blend of approaches centering on awareness (monitoring apps, allocation into categories) and automation (automated saving). Stodginess is an enemy; adaptability and longevity are essential.

Did I gain fiscal enlightenment within thirty days? No. Did I save more than I normally would? Absolutely. Most importantly, I had a valuable lesson on my own personal spending habits and learned which tools truly do keep me in check. The test stripped away the mystique of budgeting tricks, showing that the best financial plan isn't always the latest one, but the one you can realistically stick to.

Now, if you'll forgive me, I have to review my budgeting app – I think I can splurge on that latte today.

About the Creator

Get Rich

I am Enthusiastic To Share Engaging Stories. I love the poets and fiction community but I also write stories in other communities.

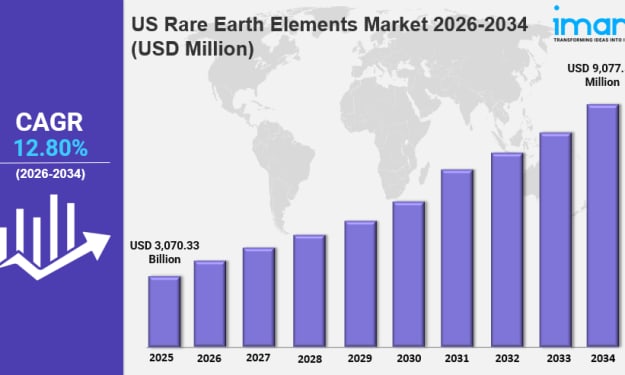

US Rare Earth Elements Market Size, Share, Industry Trends & Growth Factors Forecast 2034

Understanding the Evolution of the US Rare Earth Elements Market Rare earth elements play a quiet but essential role in modern life. From smartphones and electric vehicles to wind turbines and advanced electronics, these materials support technologies that define today’s economy. In the United States, growing industrial demand and supply chain awareness are reshaping how rare earth resources are sourced, processed, and utilized.

By Kim Soo hyun3 days ago in Trader

Review of 'Man on the Run'

My wife and I saw Man on the Run, a nearly 2-hour documentary on Amazon Prime, about Wings, Paul McCartney's group that flew around the world from shortly after The Beatles broke up in early 1970 to shortly after John Lennon was murdered at the end of 1980, making a Beatles reunion forever impossible.

By Paul Levinson5 days ago in Beat

Comments (2)

I've been there with my finances. Tried some budgeting tricks but they were a hassle. You're brave to test so many at once. Can't wait to hear how it turns out.

this topic is really mindblowing