How Hard Money Loan Lenders Evaluate Equity Instead of Appraisals

Mortgage Loans

In real estate investing, timing is everything. The faster you move, the more opportunities you unlock. Traditional financing can slow things down with credit checks, income verification, and detailed appraisals. Hard money loan lenders offer a better option. They look at one thing first; equity. If the equity is strong, the deal moves forward, sometimes within just a few days.

Traditional Lending vs. Hard Money Lending

Banks follow strict rules. They check your income, credit score, tax records, and current debt. Then, they order a full appraisal to confirm the property’s value. This entire process can take weeks. If anything doesn’t meet their criteria, the loan is denied.

Hard money lenders don’t work that way. They care less about your income and more about the deal itself. If the property has enough value to cover the multifamily bridge loan and there’s a solid plan in place; they’re ready to move forward. This approach makes funding faster and easier, especially for investors working under tight timelines.

Why Appraisals Aren’t Always Required

Appraisals are official reports created by licensed professionals. These reports tell banks how much a property is worth. The problem? Appraisals are slow and expensive. In competitive markets, waiting on an appraisal can mean losing the deal.

Hard money loan lenders often skip the appraisal for these reasons:

- Appraisals take too long. Deals can fall apart while waiting.

- They trust investor insight. Many borrowers know their market well.

- They focus on future value. They care about the after-repair value (ARV), not just the current condition.

- They use faster tools. Internal reviews, market data, and agent opinions speed up the process.

The result? Loans get approved faster, and investors can move quickly on good opportunities.

The Role of Equity in Hard Money Lending

Equity is the most important factor for a hard money lender. It’s the difference between the property’s value and what’s owed on it. The higher the equity, the lower the risk for the lender.

Let’s take an example. If a property is worth $350,000 and the borrower only owes $200,000, that’s $150,000 in equity. That equity acts as a safety net. If something goes wrong, the lender can recover the commercial bridge loan amount by selling the property.

What’s more, many lenders base equity on the after-repair value (ARV), not the current value. If the investor plans to fix and flip the property, the ARV will be much higher than the purchase price. That makes the deal even more attractive to the lender.

How Equity Is Evaluated Without a Formal Appraisal

Here are some of the most common ways Hard money loan lenders check a property’s value without ordering a traditional appraisal:

1. Broker Price Opinions (BPOs): Real estate brokers offer quick value estimates based on market trends.

2. Comparable Sales ("Comps"): The lender checks what similar properties in the area have recently sold for.

3. Purchase Price Review: If the investor bought the property below market value, that instantly adds equity.

4. After-Repair Value (ARV): The estimated value once repairs or upgrades are completed is used to project future equity.

5. In-House Reviews: Lenders may have internal staff review listings, photos, or sales data to assess value.

6. Google Earth or MLS Research: Online tools help verify property condition, lot size, location, and more.

7. Borrower’s Track Record: Experienced investors with a history of success are often trusted more with value estimates.

8. Visual Walkthroughs or Photos: Lenders may review property images or conduct on-site inspections to gauge condition and potential.

These methods help lenders make fast decisions without needing formal appraisals. They focus on the deal’s potential and real-time market data, not lengthy reports.

Benefits for the Borrower

Borrowers who work with equity-based hard money lenders in Woodland Hills enjoy several important advantages:

1. Faster Closings: Without appraisals and red tape, loans can close in as little as 5–7 days.

2. Fewer Credit Checks: Your personal credit score matters less if the equity is strong.

3. No Income Proof Needed: Self-employed or non-traditional borrowers can still qualify.

4. Flexibility with Unique Properties: Homes that banks won’t touch may still get funded based on equity.

5. Works for Distressed Properties: Ugly houses with potential are still great deals for equity-focused lenders.

6. Lower Upfront Costs: No need to pay for full appraisals or mountains of paperwork.

7. Custom Loan Terms: Equity gives room to negotiate interest rates, terms, or draw schedules.

8. Repeat Business Is Easier: Hard money loan lenders build relationships with borrowers who bring good equity again and again.

9. Less Stress for Investors: The focus is on the property, not your personal finances.

10. More Deals, More Often: With faster funding, you can move on to your next project quickly.

Final Thoughts

Hard money lending is designed for action-takers. It skips the slow parts of traditional banking and goes straight to what matters most; the value in the deal. By focusing on equity instead of formal appraisals, hard money loan lenders help investors move fast, stay competitive, and close on properties that others might miss.

Don’t let delays kill your deal. HML Investments delivers quick, reliable hard money solutions tailored for real estate investors.

About the Creator

William Sain

Want to share information regarding latest news

Keep reading

More stories from William Sain and writers in Trader and other communities.

What Makes Multi-Family Home Loans Different from Single-Family Financing?

When it comes to building wealth through real estate, one of the first decisions investors or homebuyers face is whether to invest in a single-family or multi-family property. While both paths offer unique advantages, they differ in more than just the number of units; they also vary significantly when it comes to financing. Understanding how Multi-Family home loans work compared to those for single-family homes can make all the difference in securing the right deal and planning your next move with clarity.

By William Sain6 months ago in Trader

Exploring the South Korea Cosmetics Market: Trends, Opportunities, and Insights

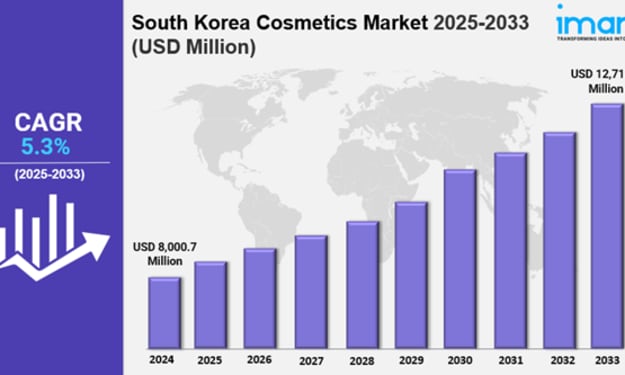

South Korea Cosmetics Market Overview South Korea cosmetics market size reached USD 8,000.7 Million in 2025. Looking forward, IMARC Group expects the market to reach USD 12,712.7 Million by 2034, exhibiting a growth rate (CAGR) of 5.3% during 2026-2034. The growing influence of social media platforms, along with the widespread adoption of extensive skincare routine by individuals, is primarily driving the market growth across the country.

By Kim Soo hyun6 days ago in Trader

Australia Computer Vision Market Poised for Strategic Growth: From Smart Surveillance to AI-Driven Enterprise Transformation

The Australia Computer Vision Market is rapidly evolving from a niche tech segment into a mainstream technology catalyst across multiple sectors. According to IMARC Group’s latest analysis, the market reached USD 434.0 million in 2025 and is poised to grow to USD 706.1 million by 2034, representing a CAGR of 5.56% during 2026–2034.

By Rashi Sharma6 days ago in Trader

Comments

There are no comments for this story

Be the first to respond and start the conversation.