Europe Cervical Cancer Market Set for Steady Growth Through 2033

How Screening Innovation, HPV Vaccination, and Public Health Policy Are Reshaping Cervical Cancer Prevention in Europe

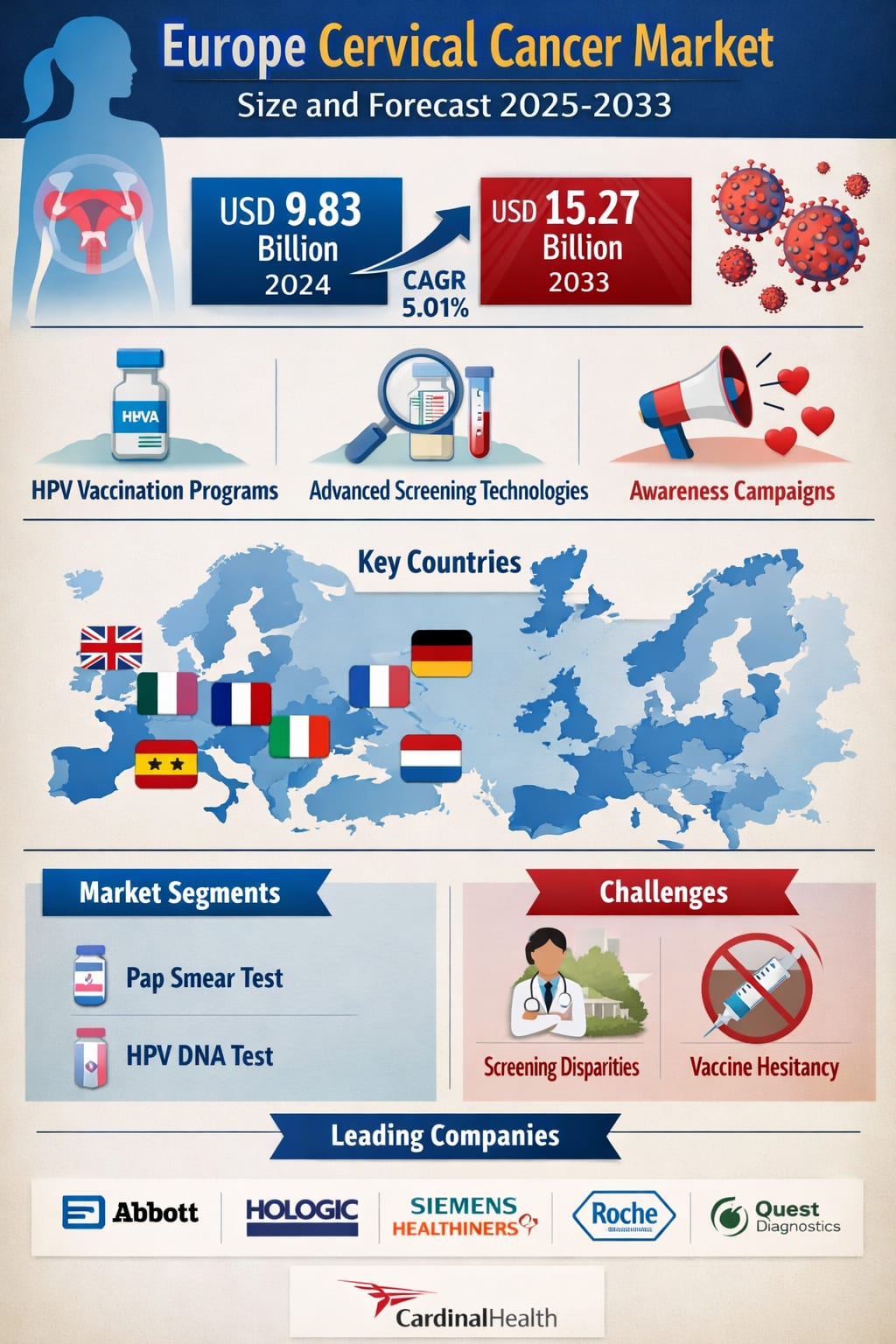

Europe Cervical Cancer Market: Size and Forecast 2025–2033

The Europe Cervical Cancer Market was valued at USD 9.83 billion in 2024 and is projected to reach USD 15.27 billion by 2033, expanding at a CAGR of 5.01% from 2025 to 2033. This steady growth reflects a powerful combination of technological advances in early detection, expanding HPV vaccination programs, rising public awareness, and strong government-backed screening policies across the region.

Cervical cancer remains one of the most preventable forms of cancer when detected early. Europe has made substantial progress in reducing mortality through routine screening programs, improved diagnostic technologies, and vaccination strategies targeting human papillomavirus (HPV), the primary cause of cervical cancer. As healthcare systems continue to modernize and prioritize preventive care, the demand for Pap smear tests, HPV DNA testing, and advanced diagnostic tools is expected to remain strong throughout the forecast period.

In addition, growing healthcare expenditure, better access to diagnostic facilities, and increased focus on women’s health are reinforcing the long-term outlook of the European cervical cancer market. Countries such as the United Kingdom, Germany, France, Italy, Spain, and the Netherlands are at the forefront of this transformation, supported by structured national screening programs and public health initiatives.

Europe Cervical Cancer Market Outlook

Cervical cancer develops in the cells of the cervix and is most commonly linked to persistent infection with high-risk HPV strains. Despite being a serious disease, it is also one of the most preventable and treatable cancers when identified early through regular screening and vaccination.

Over the past decade, Europe has witnessed a significant shift toward prevention-focused healthcare models. Awareness campaigns, government-led screening programs, and improved access to healthcare services have contributed to higher participation in routine testing. Screening methods such as Pap smears, HPV DNA tests, and colposcopy play a crucial role in detecting precancerous lesions before they progress into invasive cancer.

At the same time, HPV vaccination programs—especially among adolescents—are reshaping the long-term epidemiology of cervical cancer. Countries like the UK, Germany, France, Italy, and the Netherlands have integrated HPV vaccines into national immunization schedules, significantly reducing the future risk burden.

With continued investment in digital pathology, AI-assisted diagnostics, and molecular testing, the European cervical cancer market is expected to grow steadily, supported by both public and private healthcare sectors.

Key Drivers of Growth in the Europe Cervical Cancer Market

Rising Awareness and Government Policies

European governments have played a decisive role in promoting cervical cancer prevention through organized screening programs, HPV vaccination initiatives, and public health campaigns. Many countries offer free or subsidized screening services, encouraging early diagnosis and timely treatment.

Organizations such as the European Cervical Cancer Association (ECCA) emphasize education, prevention, and routine screening, which has significantly improved participation rates across several regions. The European Union has also issued evidence-based guidelines recommending integrated HPV vaccination and cervical cancer screening strategies.

A major public health target is to ensure that at least 70% of European women are screened every five years with high-precision HPV tests by 2030, particularly in the 35 and 45 age groups. Innovations such as self-sampling kits are further expected to increase participation, especially among populations that traditionally have lower screening uptake.

Technological Developments in Screening and Diagnosis

Technology is transforming the cervical cancer screening landscape in Europe. Advances such as liquid-based cytology, HPV DNA testing, molecular diagnostics, and AI-driven image analysis are improving both accuracy and efficiency.

Automated screening systems reduce human error, minimize false negatives, and allow for earlier intervention. The integration of digital pathology and telemedicine has also expanded access to screening services in rural and underserved areas.

In early 2025, for example, a digital health initiative supported by industry and innovation partners introduced online risk assessment tools aimed at increasing awareness during Cervical Cancer Awareness campaigns. Such developments highlight how digital health solutions are becoming an integral part of prevention strategies across Europe.

Expansion of HPV Vaccination Programs

HPV vaccination remains one of the most powerful tools in the fight against cervical cancer. Several European countries, including the UK, France, Germany, Italy, and the Netherlands, have incorporated HPV vaccines into their national immunization programs, targeting young girls and, in many cases, boys as well.

The European Union has reinforced this commitment through initiatives aligned with the Europe Beating Cancer Plan and the WHO Global Strategy to eliminate HPV-related diseases. The EU Joint Action on HPV Vaccination aims to harmonize efforts across member states, improve vaccine coverage, and address disparities in access.

As vaccination coverage expands and newer, more effective vaccines become available, the long-term incidence of cervical cancer is expected to decline—while the screening and diagnostics market continues to grow in parallel.

Challenges Facing the Europe Cervical Cancer Market

Disparities in Screening Access and Participation

Despite strong healthcare systems, screening participation rates vary widely across Europe. Socioeconomic differences, cultural barriers, lack of awareness, and geographic isolation continue to limit access in some regions.

Rural and underserved communities often face shortages of advanced diagnostic facilities, leading to delayed diagnosis and treatment. Bridging these gaps will require targeted outreach programs, mobile screening units, digital health solutions, and policy-level interventions to ensure equitable access.

Concerns Over HPV Vaccine Hesitancy

While HPV vaccines are scientifically proven to be safe and effective, vaccine hesitancy remains a concern in certain populations. Misinformation, fear of side effects, and cultural misconceptions contribute to lower vaccination rates in some regions.

Public health authorities are actively addressing these issues through education campaigns, physician-led counseling, and transparent communication. However, building trust and improving vaccine acceptance will require sustained, long-term efforts.

Europe Pap Smear Cervical Cancer Market

Pap smear testing continues to be a cornerstone of cervical cancer screening across Europe. This method detects abnormal cervical cells before they become cancerous, enabling early treatment and significantly improving survival rates.

Many European countries operate national Pap smear screening programs, which have played a key role in reducing cervical cancer incidence over the past decades. Technological advancements such as liquid-based cytology, automation, and AI-assisted slide analysis have further improved test accuracy and turnaround times.

Even as HPV DNA testing gains prominence, Pap smears remain an essential part of co-testing strategies and follow-up diagnostics, ensuring their continued relevance in the European market.

Europe HPV DNA Cervical Cancer Market

HPV DNA testing is increasingly recognized as a more sensitive and reliable screening tool compared to traditional cytology alone. It allows for the direct detection of high-risk HPV strains responsible for the majority of cervical cancer cases.

Several European healthcare systems now recommend HPV DNA testing as the primary screening method or in combination with Pap smears. The growing adoption of molecular diagnostics, HPV genotyping, and high-throughput testing platforms is driving strong growth in this segment.

As laboratories and healthcare providers continue to invest in advanced diagnostic infrastructure, HPV DNA testing is expected to play an even larger role in Europe’s cervical cancer prevention strategy.

Country-Level Market Insights

Spain Cervical Cancer Market

Spain has made significant progress through nationwide screening programs and widespread HPV vaccination campaigns. The introduction of population-based HPV screening has improved early detection rates, while increased government funding supports ongoing innovation in diagnostics and treatment.

A national directive requires all autonomous communities to adopt HPV-based screening programs, with near-universal coverage targeted by the end of the decade. This structured approach positions Spain as a strong contributor to the European cervical cancer market.

Italy Cervical Cancer Market

Italy operates organized cervical cancer screening programs, offering free Pap smears and HPV DNA tests to eligible women. High HPV vaccination coverage has already contributed to a decline in cervical cancer incidence.

Italy’s strong emphasis on preventive care, research, and personalized medicine continues to support market growth. The country also benefits from a well-developed healthcare infrastructure that facilitates early diagnosis and timely treatment.

Germany Cervical Cancer Market

Germany has an advanced and highly structured screening system that integrates HPV DNA testing with routine Pap smear programs. Universal healthcare coverage ensures broad access to screening and vaccination services.

The country is also a leader in precision medicine and AI-driven diagnostics, which is accelerating innovation in early detection and treatment. Regulatory approvals for novel therapies and diagnostics further strengthen Germany’s position in the European cervical cancer market.

France Cervical Cancer Market

France has intensified its cervical cancer prevention efforts through nationwide screening initiatives and HPV vaccination programs. Routine Pap smear and HPV testing are widely accessible, improving early detection rates.

Strong government support for research and development, public awareness campaigns, and tailored treatment strategies continues to drive market expansion. France also plays an active role in international initiatives aimed at reducing the global burden of cervical cancer.

United Kingdom Cervical Cancer Market

The United Kingdom has one of the most robust cervical cancer screening and vaccination systems in Europe. The National Health Service (NHS) provides free HPV-based screening and vaccination, resulting in high participation rates and significant reductions in disease incidence.

Public awareness campaigns and continuous upgrades in screening technology keep the UK at the forefront of cervical cancer prevention. The country’s structured approach serves as a model for other European healthcare systems.

Netherlands Cervical Cancer Market

The Netherlands has transitioned from cytology-based screening to primary HPV DNA testing, significantly improving detection rates. A universal HPV vaccination program further strengthens the country’s preventive healthcare framework.

Ongoing investments in digital pathology, AI-based diagnostics, and precision medicine are fueling innovation in screening and treatment, making the Netherlands a key contributor to Europe’s cervical cancer market growth.

Europe Cervical Cancer Market Segmentation

By Application:

Pap Smear Test

HPV DNA Test

By Test Population:

Pap Smear Test Population

HPV DNA Test Population

By Country:

United Kingdom

France

Germany

Italy

Spain

Sweden

Switzerland

Norway

Netherlands

Competitive Landscape and Company Analysis

The European cervical cancer market features several major players focusing on diagnostics, laboratory solutions, and healthcare supply chains. Companies are evaluated across five key dimensions: overview, key personnel, recent developments, product portfolio, and revenue performance.

Key Companies Include:

Abbott Laboratories

Hologic Corporation

Becton, Dickinson and Company

Siemens AG

Roche Diagnostics

Quest Diagnostics

Cardinal Health

These companies are actively investing in molecular diagnostics, automation, AI-driven screening tools, and integrated laboratory solutions, shaping the future of cervical cancer detection and management in Europe.

Final Thoughts

The Europe Cervical Cancer Market is on a clear path of sustainable growth, driven by strong public health policies, rapid technological innovation, and expanding HPV vaccination coverage. With the market expected to grow from USD 9.83 billion in 2024 to USD 15.27 billion by 2033, the region is steadily moving toward a future where cervical cancer becomes increasingly preventable, detectable, and treatable.

While challenges such as screening disparities and vaccine hesitancy remain, continued investment in education, digital health, and advanced diagnostics is expected to bridge these gaps. As Europe strengthens its commitment to early detection and prevention, the cervical cancer market will not only grow in value—but also play a crucial role in saving lives and improving women’s health outcomes across the continent.

About the Creator

Keep reading

More stories from shibansh kumar and writers in Trader and other communities.

Global Pork Meat Market Trends & Summary

Introduction: A Market on a Steady Growth Path The global pork meat market continues to hold a vital position in the international food and agriculture economy, supported by rising protein demand, expanding middle-class populations, and continuous improvements in production and processing technologies. According to Renub Research, the Pork Meat Market is expected to reach US$ 365.36 billion by 2033, growing from US$ 259.61 billion in 2024, registering a compound annual growth rate (CAGR) of 3.87% from 2025 to 2033.

By shibansh kumar2 days ago in Trader

United States Online Food Delivery Market Size, Trends & Growth Forecast 2034

How the United States Online Food Delivery Market Is Changing the Way People Eat The rise of online food delivery has transformed how Americans access meals. What began as a convenience service for busy evenings has grown into a deeply integrated part of everyday life. Across cities and suburbs alike, digital ordering platforms now influence restaurant operations, consumer habits, and even urban culture.

By Jackson Watson3 days ago in Trader

Australia Graphite Market: Powering the Clean‑Energy Transition and Industrial Demand

The Australia graphite market is undergoing a dramatic transformation as global demand for critical battery materials accelerates alongside robust industrial consumption. According to the latest IMARC Group analysis, the market was valued at USD 519.80 million in 2025 and is projected to expand to USD 2,258.71 million by 2034, representing a substantial compound annual growth rate (CAGR) of 17.73% during 2026–2034.

By Amélie Belle5 days ago in Trader

Comments

There are no comments for this story

Be the first to respond and start the conversation.