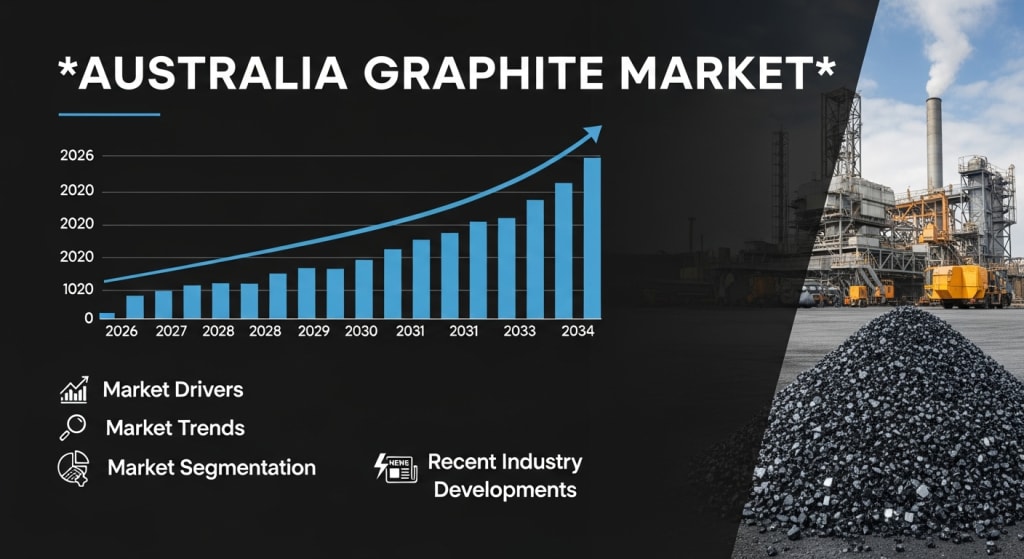

Australia Graphite Market: Powering the Clean‑Energy Transition and Industrial Demand

With rising demand for lithium‑ion battery materials and expanded industrial applications, the Australia graphite market is forecast to surge from USD 519.80 million in 2025 to USD 2,258.71 million by 2034, growing at a 17.73% CAGR.

The Australia graphite market is undergoing a dramatic transformation as global demand for critical battery materials accelerates alongside robust industrial consumption. According to the latest IMARC Group analysis, the market was valued at USD 519.80 million in 2025 and is projected to expand to USD 2,258.71 million by 2034, representing a substantial compound annual growth rate (CAGR) of 17.73% during 2026–2034.

Graphite — a form of crystalline carbon — is indispensable across a range of applications, from traditional refractory, foundry and metallurgical uses to high growth sectors such as lithium ion battery anodes for electric vehicles (EVs) and energy storage systems. Australia’s rich graphite resources, strategic positioning in global critical minerals supply chains, and supportive government policies are accelerating investment in mining, processing and downstream value addition.

Why the Market Is Growing So Rapidly

1. Electric Vehicle and Battery Storage Demand

One of the strongest growth drivers for the Australia graphite market is the rapidly increasing global uptake of electric vehicles (EVs) and battery energy storage systems. Graphite is the dominant anode material in lithium ion batteries, accounting for a major proportion of cell content. As the energy transition intensifies — with EV sales and grid scale storage deployments rising year on year — demand for high purity, battery grade graphite is rising sharply.

2. Australia’s Strategic Resource Advantage

Australia possesses some of the world’s most abundant and high quality graphite deposits, particularly natural flake graphite suitable for battery applications. Regions such as Western Australia lead production, benefiting from well developed mining infrastructure and streamlined permitting processes. These resource advantages have helped position Australia as a reliable, diversified supplier amid global supply chain reorientation away from traditional sources.

3. Expansion of Industrial Applications

Beyond batteries, graphite maintains strong demand in traditional industrial sectors. Its high thermal stability and conductivity make it essential in refractory products, foundries, casting, metallurgy, lubricants and other industrial uses. The metallurgy segment alone accounted for approximately 41% of market share in 2025, reflecting the material’s critical role in steelmaking and metal production.

4. Government Support and Policy Frameworks

Policy initiatives at both federal and state levels are reinforcing Australia’s competitive position in the global graphite landscape. Government frameworks aimed at critical minerals development — including funding support, tax incentives and regulatory streamlining — are encouraging investment across the exploration, mining, processing and value added production stages. These frameworks reduce investment risk and accelerate project timelines.

5. Supply Chain Diversification Imperatives

Global industrial players and battery manufacturers are increasingly seeking alternative graphite sources to reduce dependence on concentrated production regions, particularly China. Australia’s stable political environment and strategic partnerships with key markets provide a compelling value proposition for companies prioritising secure, ethical supply chains for critical minerals.

What the Opportunities Are

1. Battery Grade Graphite Production and Purification

With global battery demand rising, opportunities abound for companies developing downstream processing facilities capable of producing ultra high purity graphite suitable for lithium ion battery anodes. Vertical integration from mining to purification and spheronization will significantly increase value capture within Australia.

2. Strategic Partnerships and Offtake Agreements

Partnerships between Australian graphite producers and international battery, automotive and energy storage firms provide long term offtake security and investment funding. These strategic alliances enhance market stability and facilitate access to export markets.

3. Expansion of Refractory and Metallurgical Markets

Despite rapid battery driven growth, traditional applications such as refractories, casting, foundries and metallurgy will continue to drive stable demand. Innovation in refractories and high temperature graphite products represents a durable revenue stream.

4. Regional Development and Export Infrastructure

Western Australia and other resource rich regions offer targeted growth opportunities, leveraging established mining infrastructure, port connectivity and export logistics to accelerate shipments to Asia, Europe and North America.

5. Sustainable Processing Technologies

Developing environmentally responsible purification and processing methods — including alternatives to hydrofluoric acid — can reduce emissions and appeal to customers with strict environmental, social and governance (ESG) requirements.

6. Workforce Upskilling and Technical Services

Investments in specialised workforce development and technical training can help overcome skills constraints and enhance operational excellence in mining and processing operations.

7. Downstream Value Addition and Local Manufacturing

Policies and investments that support downstream manufacturing — such as graphite anode fabrication facilities — strengthen Australia’s critical minerals value chain and create high value jobs.

March 2025: Government Support Milestone: The Federal Industry and Science Minister granted major project status to a critical minerals hub on the Eyre Peninsula in South Australia, focusing on large scale graphite development and associated manufacturing infrastructure. This designation recognises the sector’s strategic importance and facilitates streamlined approvals and investment incentives.

July 2025: Resource Advancement: Renascor Resources completed bulk sample production of high grade graphite concentrate at its Siviour deposit, achieving an average carbon grade of 96.8% with a 96.5% recovery rate — a key step toward battery ready material production that enhances the company’s downstream processing prospects.

August 2025: Infrastructure Investment: The Queensland Government fast tracked approval for a USD 1.2 billion graphite mining and processing project in Croydon, backed by international firms. Expected to create more than 230 jobs and strengthen domestic value chains for battery materials, this initiative signals Australia’s growing role in critical mineral supply diversification.

Why Should You Know About the Australia Graphite Market?

The Australia graphite market is at the nexus of industrial demand and the global energy transition. Its projected growth from USD 519.80 million in 2025 to USD 2,258.71 million by 2034, at a 17.73% CAGR, underscores graphite’s escalating role as a foundational raw material for lithium ion batteries and other high tech applications.

For investors, this market offers exposure to one of the clean energy economy’s fastest growing segments, with opportunities spanning mining, processing and downstream manufacturing. For industrial players, graphite’s broad applicability across metallurgical and high performance material markets ensures diversified demand. And for policymakers, fostering domestic production, sustainable processing and export oriented infrastructure positions Australia as a strategic hub in global critical mineral supply chains for decades to come.

About the Creator

Amélie Belle

Hi, I’m Amélie Belle—27, New York writer, lover of quiet moments and honest words. I share poetry and reflections on love, healing, and life’s small miracles. If my writing makes you feel seen, I’m exactly where I’m meant to be.

Keep reading

More stories from Amélie Belle and writers in Trader and other communities.

Australia Powder Coating Equipment Market: Riding the Wave of Industrial Modernisation and Sustainability

The Australia powder coating equipment market is gaining meaningful traction as manufacturers and fabricators increasingly adopt advanced surface finishing technologies that deliver durability, corrosion protection and lower environmental impact compared to traditional liquid systems. According to the latest IMARC Group research, the market was valued at USD 95.7 million in 2025 and is expected to reach USD 168.66 million by 2034, representing a strong compound annual growth rate (CAGR) of 6.50% between 2026 and 2034.

By Amélie Belle2 days ago in Trader

BP Stock Price Prediction: Future Outlook, Forecast, and Investment View

BP plc remains one of the most closely followed energy stocks in global markets. As oil prices fluctuate and the energy sector continues to evolve, investors are increasingly searching for a realistic bp stock price prediction to understand where the company’s shares may head in the coming years. This article provides a comprehensive outlook on BP’s stock price based on business fundamentals, market trends, and long-term strategy.

By Hammad Nawaz7 days ago in Trader

Comments

There are no comments for this story

Be the first to respond and start the conversation.