Amortization Schedule: What It Is, Why It Matters, & How Lenders Can Calculate It Accurately

Amortization Schedule: What It Is, Why It Matters, & How Lenders Can Calculate It Accurately

If you’ve ever sat across from a borrower and been asked, "How much of my payment is actually reducing my loan balance?" you know how important clarity is. Borrowers want to understand where their money is going, and as a lender, it’s your job to provide that transparency.

An amortization schedule isn’t just a table of numbers—it’s a tool that builds trust by showing exactly how payments are split between principal and interest. But calculating it accurately requires precision and a solid understanding of the variables at play.

In this guide, I’ll walk you through what an amortization schedule is, why it matters, and how automation can help ensure it’s always correct.

What Is an Amortization Schedule?

Simply put, an amortization schedule is a table that details how your loan payments are allocated between principal and interest over the life of your loan. It shows you how much of each payment goes toward reducing the amount you borrowed (the principal) and how much goes toward interest.

Key Components of an Amortization Schedule

1. Payment Schedule: At its core, the schedule outlines the due dates and frequency of payments—typically monthly.

2. Interest and Principal Allocation: Each payment is divided into two parts:

- Interest: The cost of borrowing, calculated based on the remaining loan balance.

- Principal: The portion of the payment that directly reduces the loan balance.

Early in the loan term, a larger portion of the payment goes toward interest. Over time, as the principal decreases, the interest portion shrinks, and more of the payment goes toward the principal.

3. Remaining Loan Balance: With every payment, the outstanding loan balance decreases. This progressive reduction is a motivating factor for borrowers, providing them with a clear path to becoming debt-free.

Why Amortization Schedules Matter

While amortization schedules may seem like a minor detail, their impact on the lending experience is profound. Here’s why they’re essential:

1. For Borrowers

- Clarity on Payment Allocation: An amortization schedule breaks down each payment, so borrowers know exactly how much is going toward interest and how much is reducing the principal. This can help them in budgeting and managing finances.

- Better Financial Planning: With an amortization schedule, borrowers can see how their balance will reduce over time and understand the implications of early payoffs.

- Early Payoff Awareness: If you pay off your loan early, the schedule will show you how much interest you can save and what your remaining balance will be.

2. For Lenders

- Transparency in Loan Structuring: An accurate amortization schedule helps lenders set clear terms and conditions from the start, minimizing disputes and misunderstandings.

- Accurate Interest Revenue Calculations: It’s essential for lenders to track how much interest they’ll earn from each loan payment, and an amortization schedule makes this calculation easy.

- Minimizes Disputes: By providing detailed payment information, an amortization schedule helps avoid disputes between lenders and borrowers about payment allocations.

How to Calculate an Amortization Schedule

An amortization schedule might seem a bit complex, but it’s actually a straightforward process when broken down. Calculating it correctly can help you ensure that both you and your borrowers are on the same page, making payments predictable and transparent.

Here's how to go about it:

1. Start with the Loan Details

Before jumping into calculations, gather the essential loan information:

- Loan Amount (Principal): This is the total amount the borrower has borrowed.

- Interest Rate (APR): This is the annual interest rate expressed as a percentage. For example, if the interest rate is 6%, then the monthly interest rate would be 0.5% (6% / 12 months).

- Loan Term: This is the total duration over which the loan will be repaid. For instance, a 5-year loan would have 60 monthly payments (12 months × 5 years).

- Payment Frequency: Most loans are paid monthly, but bi-weekly or other schedules can also be used.

Remember, the more accurate this information is, the more reliable your amortization schedule will be.

2. Calculate the Monthly Payment

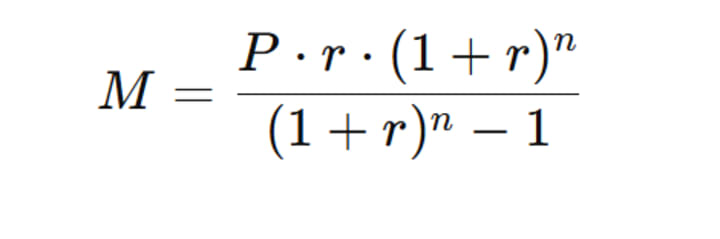

Once you have the loan details, the next step is to figure out how much the borrower needs to pay each month. The formula for calculating the fixed monthly payment for an amortizing loan is:

Where:

- M is the monthly payment.

- P is the loan amount (principal).

- r is the monthly interest rate (annual interest rate divided by 12).

- n is the total number of payments (loan term in months).

Example:

Let’s say the loan amount is $100,000, the annual interest rate is 6% (or 0.06), and the loan term is 5 years (or 60 months).

Monthly interest rate: 6% ÷ 12 = 0.5% (or 0.005 as a decimal).

Total number of payments: 60 months.

Using the formula:

M = 100,000 x 0.005 x (1+0.005)60

¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯

(1+0.005)60 - 1

M = 100,000 x 0.005 x 1.34885

¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯

0.34885

M = 674.425

¯¯¯¯¯¯¯¯¯¯¯¯¯¯¯

0.34885

M = 1933.28

So, the borrower will need to pay $1933.28 each month to fully repay the loan in 5 years.

3. Split the Monthly Payment Between Principal and Interest

Now that we know the monthly payment, we need to break it down into principal and interest.

At the start of the loan, the majority of each payment goes toward paying interest, with only a small portion reducing the principal. Over time, this ratio flips as the principal decreases.

To calculate the interest portion:

- Multiply the outstanding balance (starting with the full loan amount) by the monthly interest rate.

- Subtract the interest portion from the total monthly payment to get the principal portion.

Example:

- Starting loan balance: $100,000

- Interest rate: 0.5% per month

- Monthly payment: $1933.28

In the first month:

- Interest: $100,000 × 0.005 = $500

- Principal: $1933.28 - $500 = $1433.28

So, after the first payment, the loan balance will reduce by $1433.28.

4. Update the Loan Balance

After each payment, subtract the principal portion from the remaining loan balance. This is critical because it changes the amount on which interest is calculated in the next month.

Example:

- After the first payment, the new loan balance is:

$100,000 - $1433.28 = $98,566.72

In the second month, you’ll repeat the process:

- Interest: $98,566.72 × 0.005 = $492.83

- Principal: $1933.28 - $492.83 = $1440.45

Now, the loan balance will be:

$98,566.72 - $1440.45 = $97,126.27

Repeat this process for each payment until the loan is fully paid off.

5. Factor in Changes Like Prepayments or Variable Interest Rates

In real-world scenarios, things like early loan repayments or variable interest rates can complicate the process. If the borrower makes extra payments toward the principal, the loan balance decreases faster, which means the interest portion of future payments will be lower, and the principal portion will increase.

If the loan has a variable interest rate, the interest portion will fluctuate according to changes in the market rate. This requires recalculating the monthly payment and interest portions periodically.

6. Automate the Process

Calculating amortization schedules manually is effective but time-consuming. For businesses with large loan portfolios, automating this process is key to efficiency. Modern loan servicing software like Bryt Software can:

- Instantly calculate payments based on loan terms.

- Track changes to interest rates, payment schedules, and balances in real-time.

- Automatically generate detailed amortization schedules that are accessible to borrowers.

These tools not only improve accuracy but also allow lenders to manage larger volumes of loans with greater ease, freeing up time for more strategic activities.

Closing Thoughts

Amortization schedules might seem like a small detail in the lending process, but their impact is significant. They provide borrowers with clarity and control over their financial journey while giving lenders the tools to build trust and ensure accuracy.

By mastering the art of creating and maintaining amortization schedules—and embracing automation where possible—you can elevate the lending experience for everyone involved.

At the end of the day, it’s about more than just numbers. It’s about transparency, trust, and helping borrowers achieve their financial goals with confidence.

Author Bio: Bob Schulte

Bob Schulte, CEO of Bryt Software, drives the creation of cutting-edge, user-friendly loan management solutions. With over 30 years of SaaS industry experience and a strong record of success, Bob is a seasoned expert in software innovation, loan management, and customer-centric technology. Under his leadership, Bryt Software has become a leading name in the lending software industry, setting new standards for excellence and innovation.

LinkedIn: https://www.linkedin.com/in/bobschulte/

About the Creator

Bob Schulte

Bob Schulte, CEO of Bryt Software, is the visionary leader driving Bryt’s innovative loan management approach. With 30+ years in SaaS and 25 years in education, Bob brings a wealth of knowledge and expertise to the table.

Keep reading

More stories from Bob Schulte and writers in Trader and other communities.

10 Ways to Raise Investment Capital for Private Lending

Raising investment capital is a crucial step for private lenders looking to expand their lending capacity and increase profitability. Securing funds from the right sources allows lenders to take on more borrowers, structure competitive loan terms, and strengthen their financial position.

By Bob Schulte11 months ago in Trader

Philippines Data Center Storage Market: Cloud Expansion, Digital Growth & Infrastructure Scaling

Philippines Data Center Storage Market Overview The Philippines data center storage market is expanding rapidly as digital transformation accelerates and businesses, government agencies and service providers increasingly require robust storage infrastructure to manage burgeoning data volumes. Data center storage refers to high-capacity systems that retain, manage and secure digital information generated by cloud services, enterprise operations, mobile traffic and streaming applications. The Philippines data center storage market size reached USD 548.0 Million in 2025. Looking forward, IMARC Group expects the market to reach USD 1,357.1 Million by 2034, exhibiting a growth rate (CAGR) of 10.60% during 2026-2034. This growth reflects the nation’s accelerating digital adoption, enterprise cloud migration strategies, increasing internet penetration and expansion of digital services across sectors.

By Manisha Dixit6 days ago in Trader

Not Just For Clean Up: A History Of The MCU's Department of Damage Control

Initially an organisation that seemed to exist to help the heroes of the Marvel Cinematic Universe, from Phase Four onwards, the Department of Damage Control has shifted into a more antagonistic role. Most recently seen in the Wonder Man series, the current incarnation of Damage Control seems to target superpowered individuals, regardless of whether that person poses an active or intentional threat.

By Kristy Anderson4 days ago in Geeks

Comments

There are no comments for this story

Be the first to respond and start the conversation.