Trump Pushes a 1-Year, 10% Cap on Credit Card Interest Rates — Banks Balk

The proposal sparks debate over consumer protection, banking profits, and economic impact

Introduction

Former U.S. President Donald Trump has reignited controversy in the financial sector by proposing a 1-year, 10% cap on credit card interest rates. According to Trump, the move aims to protect American consumers from what he calls “usurious” rates that burden millions of households. While many consumers welcomed the proposal, major banks and financial institutions have expressed strong opposition, arguing that such a cap could disrupt credit markets and hurt the economy.

The debate highlights a recurring tension in U.S. finance: balancing consumer protection with the viability of lending institutions, and raises questions about how political proposals intersect with complex financial systems.

The Proposal in Detail

Trump’s plan proposes limiting credit card interest rates to 10% annually for one year, with the intent to relieve borrowers facing rising debt and high interest rates. He frames it as a temporary measure to provide immediate financial relief while broader economic policies stabilize.

Supporters argue that this cap could:

Reduce interest burdens for millions of Americans

Prevent debt spirals and financial hardship

Encourage responsible lending practices

However, critics question whether a short-term cap can effectively address systemic issues in consumer credit, or whether it may create unintended consequences.

Banking Industry Pushback

Major banks have publicly criticized the proposal, warning that such a rate cap could:

Shrink profits and reduce incentives to offer credit

Lead to stricter lending standards, making it harder for consumers to obtain credit

Disrupt existing credit contracts and legal frameworks

Some banks argue that risk-based pricing is necessary to compensate lenders for potential defaults. Limiting interest rates indiscriminately may result in lenders either tightening credit availability or charging higher fees elsewhere to offset losses.

Economic Implications

Economists have weighed in on the potential consequences of Trump’s proposal:

Potential Benefits

Reduced financial strain on households carrying high credit card balances

Short-term stimulus effect as consumers have more disposable income

Increased public attention on consumer debt and predatory lending practices

Potential Risks

Reduced lending could slow consumer spending, a key driver of economic growth

Banks may shift costs to other financial products, such as loans, checking accounts, or late fees

Legal challenges may arise if retroactive enforcement is attempted

The debate underscores the delicate balance between consumer protection and economic stability, especially when regulatory interventions are abrupt or temporary.

Consumer Perspectives

For American consumers, particularly those carrying high-interest credit card debt, the proposal has been largely welcomed. According to recent surveys, the average credit card APR exceeds 20%, placing a heavy burden on many households.

One consumer advocate stated, “Millions of Americans are trapped in high-interest cycles that make it impossible to pay down debt. A temporary 10% cap could provide much-needed relief, especially as inflation and living costs continue to rise.”

However, some caution that without careful design, the proposal could limit access to credit for lower-income households if banks respond by tightening lending criteria.

Political Context

Trump’s proposal comes amid heightened attention on consumer debt and inflation in the United States. Politically, the initiative aligns with a broader populist message aimed at portraying Trump as a champion of everyday Americans against powerful financial institutions.

While Trump does not currently hold office, proposals like this can influence public debate, shape party platforms, and pressure lawmakers to address consumer credit issues more aggressively.

Historical Precedent

The U.S. has a mixed history of interest rate caps:

State-level usury laws historically limited interest rates, but federal regulations often overrode them for national banks

Credit card deregulation in the 1980s allowed interest rates to rise, fueling modern credit card practices

Trump’s proposal echoes previous calls for usury reform, but the unique 1-year, 10% limit is unusual in modern financial markets and could trigger legal and operational challenges if attempted.

Potential Alternatives

Critics of the cap suggest alternative approaches to protect consumers without creating market disruption:

Enhanced transparency requirements for credit card terms

Incentives for low-interest credit products

Support for debt consolidation and financial education programs

These approaches aim to reduce consumer debt burdens without directly interfering in lending profitability, providing a more sustainable, long-term solution.

Conclusion

Trump’s push for a 1-year, 10% cap on credit card interest rates has sparked heated debate between consumer advocates and financial institutions. On one hand, the proposal highlights the urgent need to address high-interest debt that affects millions of Americans. On the other hand, banks argue that such a measure could disrupt credit availability, reduce profits, and unintentionally harm consumers who rely on access to credit.

The controversy reflects a broader tension in U.S. finance: how to protect consumers without destabilizing financial systems. While Trump frames the cap as immediate relief for households, economists and banking executives warn that practical implementation is far from simple. Whether viewed as bold populism or impractical policymaking, the proposal has succeeded in bringing consumer debt and credit card practices back into the national spotlight, highlighting the ongoing debate over fairness, regulation, and economic stability in modern America.

About the Creator

Asad Ali

I'm Asad Ali, a passionate blogger with 3 years of experience creating engaging and informative content across various niches. I specialize in crafting SEO-friendly articles that drive traffic and deliver value to readers.

Switzerland Used Car Market Size & Forecast 2025–2033

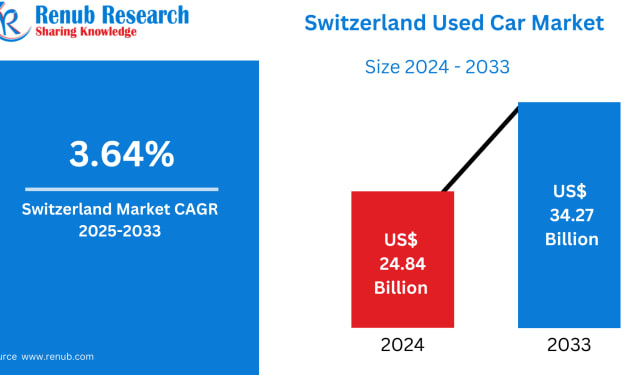

Switzerland Used Car Market Overview The Switzerland Used Car Market is undergoing steady and resilient expansion, reflecting changing consumer priorities, economic pragmatism, and evolving mobility trends. According to Renub Research, the market is expected to grow from US$ 24.84 billion in 2024 to US$ 34.27 billion by 2033, registering a Compound Annual Growth Rate (CAGR) of 3.64% between 2025 and 2033.

By Marthan Sir5 days ago in The Swamp

Fair Exchange, No Robberies

Dark Memoirs - Index There are at least two kinds of people in the world: those who write this half-arsed kind of intro to a story that looks to separate the rare and the norm, and those who realise it's an overused framing device and don't.

By Paul Stewart6 days ago in Chapters

Comments

There are no comments for this story

Be the first to respond and start the conversation.