Power Transformer Market Size and Forecast 2025–2033

Global grid expansion, renewable integration, and smart infrastructure push the transformer industry into a high-growth decade

Introduction

The power transformer market is entering a decisive growth phase as nations modernize electricity networks, integrate renewable energy, and respond to rising demand from urbanization and industrialization. According to Renub Research, the global power transformer market was valued at about USD 26.87 billion in 2024 and is projected to nearly double to approximately USD 52.16 billion by 2033, expanding at a robust CAGR of 7.65% from 2025 to 2033. This acceleration reflects more than cyclical infrastructure spending—it signals a structural shift in how power is generated, transmitted, and distributed across modern economies.

Power transformers sit at the heart of the electricity ecosystem. They enable long-distance transmission at high voltages, minimize losses, and ensure safe delivery to residential, commercial, and industrial users. As grids evolve to accommodate renewable generation, electric vehicles, data centers, and smart cities, transformer technology is being re-engineered for efficiency, reliability, and digital intelligence.

Power Transformer Market Overview

A power transformer is an electromechanical device that transfers electrical energy between circuits using electromagnetic induction, stepping voltage up or down to optimize transmission and distribution. Built with high-grade insulation, magnetic cores, and copper or aluminum windings, these systems are designed for continuous operation under heavy loads. Their role in substations, power plants, and industrial facilities makes them indispensable to grid stability, power quality, and system safety.

Globally, growth is propelled by three converging forces:

Rising electricity demand: Urbanization, electrification of transport, and expanding manufacturing are stretching legacy grids.

Renewable integration: Solar and wind generation introduce variability that requires advanced transformer designs to manage fluctuating loads and bidirectional power flows.

Grid modernization: Smart grids, digital monitoring, and energy-efficient transmission technologies are reshaping procurement standards.

Developing regions are investing in rural electrification and cross-border interconnections, while mature markets are replacing aging infrastructure with low-loss, environmentally safer equipment. Together, these trends sustain a strong, multi-year demand cycle.

Market Drivers

1) Infrastructure Development and Urban Expansion

Large-scale infrastructure programs—metros, industrial corridors, data centers, and housing—are increasing the density and complexity of power networks. Utilities require higher-capacity transformers to manage peak loads and maintain voltage stability across expanding urban footprints.

2) Renewable Energy and Grid Flexibility

Wind and solar capacity additions require transformers capable of handling intermittent generation and integrating energy storage. Ultra-high-voltage (UHV) projects, offshore wind connections, and hybrid substations are accelerating adoption of advanced power transformers with enhanced insulation, cooling, and digital control.

3) Smart Grids and Digitalization

Utilities are embedding sensors, condition monitoring, and predictive maintenance into transformer fleets. “Smart” transformers reduce downtime, optimize asset life, and improve operational efficiency—features increasingly mandated in new tenders.

4) Sustainability and Energy Efficiency

Regulatory pressure to reduce transmission losses and carbon footprints is driving demand for low-loss cores, biodegradable insulating fluids, and recyclable materials. Sustainability is no longer a differentiator; it is a baseline requirement.

Competitive Landscape: Leading Manufacturers

Bharat Heavy Electricals Limited (BHEL) – India

A cornerstone of India’s power infrastructure, BHEL designs, engineers, and executes projects across generation, transmission, and heavy industry. Its transformer portfolio spans EHV and specialty units, supported by extensive manufacturing, R&D, and after-sales services.

Daihen Corporation – Japan

Founded in 1919, Daihen delivers power transmission and distribution systems, automation, and welding solutions. Its focus on R&D, quality, and sustainable technologies positions it strongly across Asia-Pacific, Europe, and North America.

General Electric (GE) – USA

A diversified industrial leader, GE offers advanced grid solutions, including high-capacity transformers integrated with digital energy management. Its global manufacturing and service network supports utilities and large infrastructure projects worldwide.

Hitachi (and Hitachi Construction Machinery as a subsidiary example) – Japan

Within Hitachi’s broad industrial ecosystem, power systems and grid solutions benefit from deep engineering expertise and global operations spanning Asia, Europe, the Americas, and emerging markets.

Hyosung Heavy Industries Corporation – South Korea

Hyosung’s heavy industry arm supplies power grid systems globally, combining materials science, advanced manufacturing, and a strong export footprint across the US, Europe, the Middle East, and Asia.

Product Launches and Innovation

Hyundai Electric & Energy Systems (Jan 2022): Exported ultra-high-voltage power transformers to Oman’s state utility in a deal valued at USD 8.5 million. The supply of 400-kV/500-MVA units underscores the growing scale of transmission projects in the Middle East.

Schneider Electric (Oct 2024): Launched MasterPacT MTZ Active, a next-generation circuit breaker designed to enhance safety, efficiency, and sustainability—reflecting the broader push toward digital, resilient electrical infrastructure.

These developments highlight a market moving toward higher capacities, smarter controls, and lifecycle efficiency.

Company SWOT Snapshots

CG Power & Industrial Solutions Ltd.

Strengths: Diversified product portfolio, advanced manufacturing, and strong global presence. CG Power’s expertise across EHV, distribution, and specialty transformers, coupled with turnkey project capabilities, positions it as a comprehensive solutions provider. Its export reach across 80+ countries strengthens competitiveness.

Fuji Electric Co., Ltd.

Strengths: Technological innovation, high-quality engineering, and leadership in advanced power systems. Fuji’s eco-friendly, compact transformer designs integrate smart monitoring and low-loss technologies, aligning closely with smart grid and renewable trends.

Recent Developments

Kirloskar Electric Co. Ltd. (Mar 2022): Introduced high-efficiency low-voltage electric motors manufactured with high-grade copper and certified testing—reflecting the industry’s broader emphasis on efficiency and compliance.

Siemens Energy AG (Sep 2025): Laid the cornerstone for a new Technology Campus in Erlangen, Germany, focused on power electronics under the “Made for Germany” initiative. The project strengthens Europe’s innovation base in energy systems.

Sustainability as Strategy

ABB Ltd.

ABB embeds sustainability into transformer design through low-loss cores, biodegradable insulating fluids, and digital monitoring for energy efficiency and extended asset life. The company targets carbon-neutral operations by 2030 and champions circular-economy principles via recyclability and resource optimization.

TBEA Co., Ltd.

TBEA advances green manufacturing and high-efficiency transformer technology, supplying equipment for solar, wind, and UHV transmission. Its operational focus includes energy-efficient facilities, pollution control, and digital “smart transformer” solutions for real-time monitoring and grid optimization.

Sustainability is reshaping procurement criteria. Utilities increasingly favor vendors that combine performance with environmental stewardship.

Market Segmentation

While detailed numerical splits vary by region, the power transformer market is commonly segmented by:

By Rating: High-voltage, medium-voltage, and low-voltage; with UHV projects gaining prominence.

By Cooling Type: Oil-immersed and dry-type transformers, the latter favored in urban and environmentally sensitive installations.

By Application: Transmission, distribution, and power generation (including renewables).

By End-User: Utilities, industrial facilities, infrastructure projects, and commercial complexes.

By Geography: Asia-Pacific leads growth, followed by North America, Europe, the Middle East & Africa, and Latin America.

Historical Trends and Forecast Analysis

Historically, transformer demand tracked capital expenditure cycles in utilities and heavy industry. The post-pandemic recovery, coupled with government-backed green investments, has structurally elevated the market. From a base of USD 26.87 billion in 2024, the market is projected to reach USD 52.16 billion by 2033, reflecting sustained investments in grid resilience, renewable integration, and digital infrastructure.

Key forecast themes include:

Replacement of aging assets in developed markets to reduce losses and improve reliability.

Greenfield projects in emerging economies to expand access and capacity.

Digital retrofits to enable predictive maintenance and grid intelligence.

Market Share and Company Deep-Dive Framework

For major players—BHEL, Daihen, GE, Hitachi, Hyosung, Hyundai Electric, Kirloskar Electric, Mitsubishi Electric, Schneider Electric, Siemens Energy, ABB, TBEA, CG Power, Fuji Electric, Toshiba Energy Systems & Solutions, WEG, SGB-SMIT, Alstom Grid, JSHP Transformer, China XD Group—analysis typically spans:

Company Overview: History, mission, and business model

Operations & Workforce: Manufacturing footprint and service networks

Leadership: Executive teams and governance

Strategy: M&A, partnerships, investments

Sustainability: Renewable adoption, energy-efficient infrastructure, water and waste management, circular-economy initiatives

Products: Portfolio, quality standards, pipeline, benchmarking

Financials: Revenue performance and market share

SWOT: Strengths, weaknesses, opportunities, and threats

This structured approach highlights how scale, innovation, and sustainability differentiate leaders in a consolidating market.

Regional Outlook

Asia-Pacific: The fastest-growing region, driven by China, India, and Southeast Asia’s electrification, renewable build-outs, and mega-infrastructure.

North America: Grid hardening, data center expansion, and renewable integration sustain steady demand.

Europe: Energy transition policies, offshore wind, and cross-border interconnections drive high-specification transformer projects.

Middle East & Africa: Transmission upgrades and new generation capacity, particularly in GCC countries and electrification initiatives in Africa.

Latin America: Renewable investments and modernization of legacy networks support medium-term growth.

Challenges and Risks

Supply Chain Volatility: Copper, steel, and specialized insulation materials remain exposed to price swings.

Project Delays: Permitting, financing, and geopolitical uncertainties can defer large transmission projects.

Technological Complexity: Integrating digital systems and meeting evolving environmental standards increases design and compliance costs.

Nevertheless, long-term fundamentals—electrification, decarbonization, and digitalization—continue to outweigh near-term risks.

Strategic Implications for Stakeholders

Utilities: Prioritize life-cycle efficiency, digital monitoring, and sustainability in procurement.

Manufacturers: Invest in R&D for low-loss materials, smart diagnostics, and modular designs to shorten deployment times.

Investors: Favor firms with diversified geographies, strong order backlogs, and leadership in green technologies.

Policy Makers: Align grid modernization funding with renewable targets and resilience objectives to accelerate infrastructure upgrades.

Final Thoughts

The global power transformer market is transitioning from a traditionally cyclical industry into a strategic pillar of the energy transition. With market value projected to rise from USD 26.87 billion in 2024 to USD 52.16 billion by 2033 at a 7.65% CAGR, growth is anchored in real, long-term demand: expanding grids, renewable integration, smart infrastructure, and sustainability mandates.

Manufacturers that combine scale with innovation—delivering efficient, digitally enabled, and environmentally responsible transformers—will shape the next decade of power infrastructure. For utilities, investors, and policymakers, the message is clear: transformers are no longer just components of the grid; they are enablers of a resilient, low-carbon, and electrified future.

About the Creator

jaiklin Fanandish

Jaiklin Fanandish, a passionate storyteller with 10 years of experience, crafts engaging narratives that blend creativity, emotion, and imagination to inspire and connect with readers worldwide.

Keep reading

More stories from jaiklin Fanandish and writers in The Swamp and other communities.

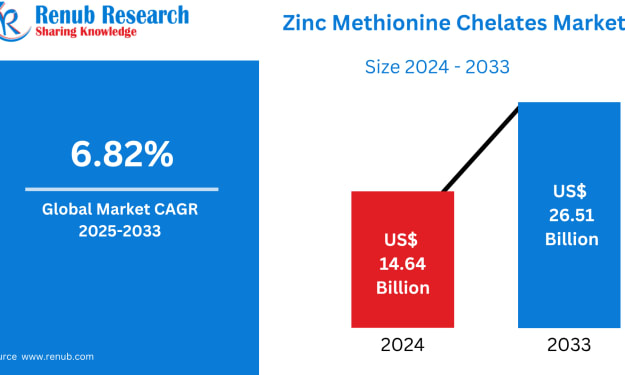

Zinc Methionine Chelates Market Size and Forecast 2025–2033

Introduction As global agriculture enters a new era of efficiency, sustainability, and precision nutrition, the role of advanced feed additives is becoming more critical than ever. Among these, Zinc Methionine Chelates are gaining notable attention for their superior bioavailability, environmental benefits, and impact on animal productivity. Once considered a niche solution, chelated trace minerals are now reshaping livestock nutrition strategies across developed and emerging economies alike.

By jaiklin Fanandish6 days ago in The Swamp

Iran Warns Attack on Khamenei Would Be Declaration of War

In a sharp escalation of rhetoric, Iran has warned that any attack on its Supreme Leader, Ayatollah Ali Khamenei, would be treated as a declaration of war against the entire nation. The warning came on January 18, 2026, from Iranian President Masoud Pezeshkian, highlighting Tehran’s sensitivity to foreign threats amid domestic unrest and tense relations with the United States.

By Aarif Lashariabout 14 hours ago in The Swamp

Comments

There are no comments for this story

Be the first to respond and start the conversation.